Welcome to CENFACS’ Online Diary!

04 June 2025

Post No. 407

The Week’s Contents

• Creative Economic Development Month and Jmesci (June Month of Environmental and Sustainable Initiatives) Project 2025

• Matching Organisation-Investor via Telehealth Facility – Activity 2 (04 to 10/06/2025): Matching Organisation-Investor via Market Analysis, Feature Prioritization and Design

• Activity/Task 6 of the Restoration (R) Year/Project: Work with the Needy to Improve Creations and Innovation Linked to Restoration

… And much more!

Key Messages

• Creative Economic Development Month and Jmesci (June Month of Environmental and Sustainable Initiatives) Project 2025

The key theme for June 2025 is Creations and Innovations to Reduce Poverty and Enhance Sustainable Development. Within this main theme, there are 3 sub-themes which are

σ creative and innovative challenges (that is, the challenges that the creative and innovative abilities of some of the CENFACS Community members can face)

σ critical and strategic resources or minerals (that is, the use of critical and strategic natural resources or minerals for energy transition and poverty reduction)

σ loss or depreciation of assets value (that is, the loss or depreciation of households’ assets value).

Inside these sub-themes, there are codes.

These three sub-themes make up the plan for June 2025 as highlighted below.

a) Challenges hindering the ability to create and innovate (CHACI)

CHACI echoes the theme of World Creativity and Innovation Day 2025 (1) held last 21 April; theme which was ‘Step out and Innovate‘. We are continuing to raise awareness of the role of creativity and innovation in all aspects of poverty reduction and sustainable development.

To continue the theme of the World Creativity and Innovation Day 2025, we are going to work on strategy to address challenges that some of the CENFACS Community members may face in terms of their abilities to create and innovate solutions to come out poverty and improve the quality of their lives.

b) Creations and Innovations relating to the use of critical or strategic natural resources or minerals for energy transition and poverty reduction

Forming from nothing ideas or introducing changes to move forward together will be the main activity during the month of June 2025. These creative ideas and innovative ways of working will enable to find the means to meet the level of ambition we have for the kind of sustainable development and future we want, which we hope will help achieve a more equitable and inclusive society.

Using our experience, skills, knowledge and talents to find techniques, technologies and new methods to deal with the use of critical or strategic natural resources or minerals for energy transition (like aluminium, cobalt, copper, lithium, platinum, etc.) and poverty reduction will not be enough unless we create and innovate to prevent or at least to mitigate future crises. It means there could be another need to bring into existence ideas and introduce changes and new methods to address future crises if they happen when they happen.

In practical terms, we shall work on creations and innovations that make critical or strategic minerals to reduce poverty by creating jobs for those in need, generating income for the poor, focussing on artisanal and small-scale mining of these minerals to create opportunities for local people and communities.

c) Creations and Innovations to deal with the loss (depreciation or devaluation) of households’ assets value

Loss of asset value of poor households is the decline in the worth of their possessions. This decline, which can happen through depreciation and devaluation, could push them further into poverty, particularly but not limited to asset-based poverty, or prevent them from escaping from this type of poverty.

This is why it is better to create and innovate to tackle households’ loss of asset value by implementing a robust asset management plan. Such plan will consider strategies like depreciation, impairment testing and asset disposal.

Creations and innovations to tackle the causes of asset value loss (e.g., distress sales, health shocks, lack of savings, low-income and high costs, inefficiency or inadequacy, etc.) will be conducted to help reduce asset-based poverty.

So, we have 3 sub-themes of creations and innovations to offer in the context of the Creative Economic Development Month (CEDM).

During this CEDM, we are forming responses from nothing and bringing them into existence to deal with the above-mentioned sub-themes. Equally, we are going to introduce new ideas or methods as well as make changes to what has been tried and tested to deliver these kinds of sub-themes.

In this process of forming proposals and introducing new methods, we are going to work with the community – via the project Jmesci (June Month of Environmental and Sustainable Initiatives project) featuring this month – to try to create and innovate so that we are all able to better meet the challenges and cross the hurdles brought by crises or shocks (such as the cost-of-living crisis, trade tariff crisis, international aid cuts, natural disaster, humanitarian catastrophe, etc.).

June 2025 is a feature-rich month during which we shall streamline users’ content creation and innovation processes. In this process of creating and innovating, we shall consider some of the creative and innovative ideas, proposals, metrics, experiences and tools that have been so far put forward to help poor people and households reduce poverty and hardships.

Our work will revolve around the kinds of creation and innovation the CENFACS Community (and alike our Africa-based Sister Organisations) needs in order to find ways of moving forward to protect the gains or legacies of our building-forward-better-together work while building upon progress to achieve a more equitable and inclusive society.

Under the Main Development section of this post, we have provided further information about this first key message.

• Matching Organisation-Investor via Telehealth Facility – Activity 2 (04 to 10/06/2025): Matching Organisation-Investor via Market Analysis, Feature Prioritization and Design

The second activity or episode of our 5-week Matching Organisation-Investor via Telehealth Facility is about Matching Organisation-Investor via Market Analysis, Feature Prioritization and Design.

Both Africa-based Sister Charitable Organisation (ASCO) and not-for-profit (n-f-p) impact investor have decided to move forward with the matching talks as they scored points each of them during Activity 1. They agreed to move to Activity 2 while finalising the little bits remaining from Activity 1 of the matching negotiations.

To summarise what is going to happen at this Activity 2, we have organised our notes around the following headings:

σ Activity 2 Matching Concepts

σ Africa-based Sister Charitable Organisation’s Market Analysis (MA), and Feature Prioritization and Design (FPD)

σ Not-for-profit Impact Investor’s View on MA and FPD

σ The Match or Fit Test.

Let us look at each of these headings.

• • Activity 2 Matching Concepts

There are three concepts making this Activity 2. The first concept is market analysis and is part of ASCO’s telehealth business plan. The second and third concepts are feature prioritization and feature design, which are one of the steps in ASCO’s telehealth software development.

Let us explain these concepts.

• • • Market analysis

The website ‘wallstreetmojo.com’ (2) explains that

“Market analysis is a comprehensive study of a specific market within an industry, including an examination of its various components, such as market size, key success factor, distribution channels, target audience, profitability, and growth rate, and market trend”.

From the point of view of the same ‘wallstreetmojo.com’, market analysis should not be confused with market research (that is, a focus on a specific market segment and its customers) and industry analysis (that is, the examination of the whole industry).

From the definition of market analysis, ASCO needs to evaluate and understand the telehealth market conditions, trends, and competition to make informed business decisions.

• • • Features prioritization and design

To explain features prioritisation and design, let us first start with the word ‘feature’.

According to ‘6b.digital’ (3),

“A feature is essentially anything that does something within a piece of software… Features are capabilities or functionalities. They allow users to perform actions for a desired result”.

Features can be prioritised and designed. ASCO would be required to prioritise and design the features of its telehealth software development.

• • • • Feature prioritization

The definition of feature prioritization selected here comes from ‘optimizely.com’ (4) which argues that

“Feature prioritization determines the importance or order in which different features or functionalities should be implemented, improved, or represented to users within a product or service. The process involves assessing the potential impact and value of each feature and making decisions based on various criteria”.

From this perspective, feature prioritisation will determine the order in which features are developed and released, balancing customer value, business goals, and technical feasibility.

In terms of the Telehealth Facility, ASCO has to consider feature prioritisation influencers such as beneficiary/customer needs, telehealth goals, testing and data analysis, feasibility, market trends and competition and alignment with log-term telehealth strategy and vision.

• • • • Feature design

In marketing, design encompasses the planning and creation of the user interface, user experience, and overall look and feel of the product. From this understanding of design, it is possible to explain feature design.

Feature design can be approached in many ways. One of the ways of approaching is given on the website ‘sciencedirect.com’ (5) where it is mentioned that

“Feature-based design is a design approach in computer science that involves using predefined features and operations to define sketched features, where the geometry is created by sweeping a planar cross-section or lofting between tow or more planar cross-sections with declarative constraints”.

ASCO would be expected to have the design of the telehealth feature-based.

Knowing the meaning of the above-mentioned concepts, the two sides of the matching talks will use them to negotiate. Let us see what each party will bring to the negotiating table.

• • Africa-based Sister Charitable Organisation’s Market Analysis (MA), and Feature Prioritization and Design (FPD)

ASCO will negotiate and argue about its plan for market analysis and features prioritisation and design.

Concerning market analysis, ASCO needs to demonstrate that it did understand TF beneficiaries, track competition, test the service to be delivered and predict the future of TF.

ASCO can use the opportunity of the matching negotiations to provide market analysis metrics to show how deep it has analysed the market. It can provide the following market analysis metrics or tools:

~ market size and growth rate (measures the potential revenue or customer/beneficiary base)

~ market share (helps assess the percentage of total sales or market revenue for ASCO’s brand)

~ customer/beneficiary acquisition cost (indicates the cost of acquiring new customers or beneficiaries)

~ customer/beneficiary lifetime value (estimates the total revenue a customer/beneficiary will generate)

~ conversion rate (measures the percentage of website visitors and leads)

~ return on investment (the number of people to be lifted out of health poverty rather than the financial profitability of the investment made)

~ brand awareness (indicates the level of recognition or familiarity with ASCO’s brand)

~ customer/beneficiary satisfaction and loyalty (measures the perceptions of customers/beneficiaries)

~ competition analysis (analyses the strengths and weaknesses of TF competitors)

etc.

By providing these metrics, ASCO will prove that its has carried out a thorough data-driven work.

Regarding features prioritisation and design, ASCO has to define and explain the following:

~ the core features of its software as a product or service

~ user interface (that is, the visual layout and elements of its product)

~ user experience (that is, the overall user journey and interactions with the product)

~ usability (that is, how easy it is for users to use and navigate the product)

~ the workflow integration and data security.

Failure to define and explain the core features of its software can create disagreement with the not-for-profit impact investor.

• • Not-for-profit Impact Investor’s View on MA and FPD

The definitions and explanations provided by ASCO about MA and FPD must align with n-f-p impact investor’s view on them.

Concerning the MA, the n-f-p impact investor wants to know which methods and tools (e.g., surveys, focus groups, field trials, personal interviews, observations, social media, etc.) ASCO will use to conduct its market analysis and decision-making process.

Regarding the FPD, the n-f-p impact investor will be keen to know ASCO’s technology plan, particularly the order in which features will be developed and released. He/she will want to be told if ASCO will run a pilot telehealth service and if it will thoroughly explain user interface and user experience about the software product. Additionally, he/she would like some details on how ASCO will reduce wasted effort or resources on low impact feature.

In short, the n-f-p impact investor would like some guarantee that the online and phone-based healthcare service or bespoke remote healthcare programme, including the FPD, will be helpful for both health professionals and users. He/she is keen to know if there are some links between ASCO’s three plans: healthcare services plan, business plan and technology development plan. Briefly, he/she wants to understand ASCO’s telehealth business model through ASCO’s market analysis and MA and FPD.

There should be an agreement between ASCO’s MA and FPD on the one hand, and the n-f-p impact investor’s view on them on the other hand. If there is no agreement or alignment of the two positions, the matching talks may not go to the next stage of this matching process or to progress. If there is a disagreement, then the talks/negotiations could be subject to match or fit test.

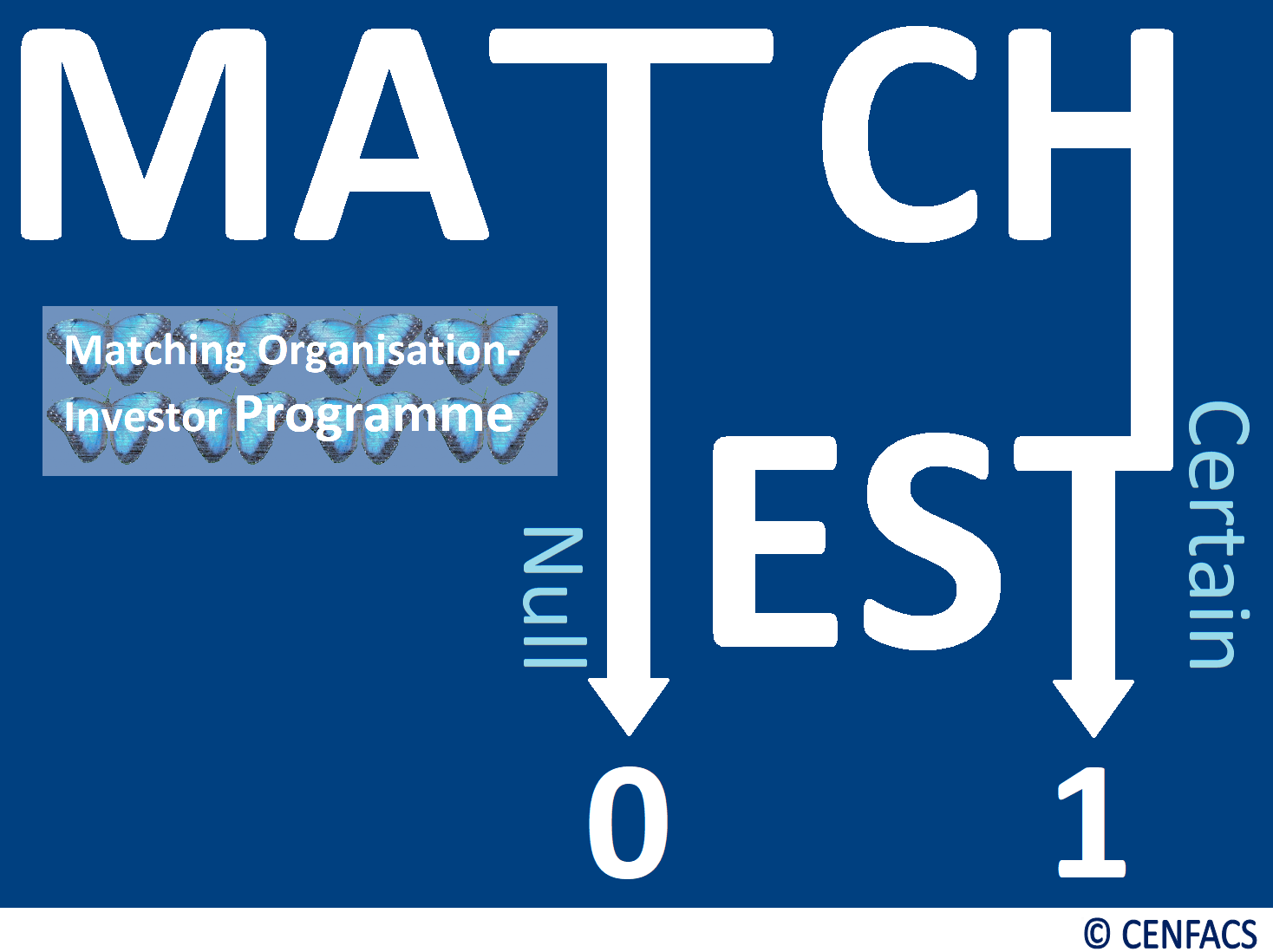

• • The Match or Fit Test

As part of the match or fit test, n-f-p Impact Investor’s view on ASCO’s MA and FPD must be matched with the information coming out of ASCO’s MA and FPD documents.

The match can be perfect or close in order to reach an agreement. If there is a huge or glaring difference between the two (i.e., between what the investor wants and what ASCO is saying about its MA and FPD, between what the investor would like the MA and FPD phase to indicate and what ASCO’s MA and FPD are really saying), the probability or chance of having an agreement at this second round of negotiations could be null or uncertain.

However, if this happens there is still a chance as CENFACS can advise ASCO and guide n-f-p investor on their approaches to Telehealth Facility.

• • • Impact Advice to ASCO and Guidance to n-f-p Impact Investor

CENFACS can impact advise ASCOs to improve the presentation of the MA and FPD they are bringing forward. CENFACS can as well guide n-f-p impact investors to work out their expectations in terms of the MA and FPD to a format that can be agreeable by potential ASCOs. CENFACS’ impact advice for ASCOs and guidance on impact investing for n-f-p impact investor, which are impartial, will help each of them (i.e., investee and investor) to make informed decisions and to reduce or avoid the likelihood of any significant losses or misunderstandings or mismatches.

However, to reduce or avoid this likelihood both parties need to follow the rule of the matching game.

• • • The Rule of the Matching Game

The rule of the game is the more impact investors are attracted by ASCO’s MA and FPD the better for ASCOs. Likewise, the more ASCOs can successfully respond to impact investors’ level of enquiries and queries about the MA and FPD the better for investors. In this respect, the matching game needs to be a win-win one to benefit both players (i.e., investee and investor).

The above is the second stage or activity of the Matching Organisation-Investor via Telehealth Facility.

Those potential organisations seeking investment to set up a telehealth facility in Africa and n-f-p impact investors looking for organisations that are interested in their giving, they can contact CENFACS to arrange the match or fit test for them. They can have their fit test carried out by CENFACS’ Hub for Testing Hypotheses.

• • • CENFACS’ Hub for Testing Hypotheses

The Hub can help to use analysis tools to test assumptions and determine how likely something is within a given standard of accuracy. The Hub can assist to

√ clean, merge and prepare micro-data sources for testing, modelling and analysis

√ conduct data management and administration

√ carry out regression analysis, estimate and test hypotheses

√ interpret and analyse patterns or trends in data or results.

For any queries and/or enquiries about this second stage/activity of Matching Organisation-Investor via Telehealth Facility, please do not hesitate to contact CENFACS.

• Activity/Task 6 of the Restoration (R) Year/Project: Work with the Needy to Improve Creations and Innovation Linked to Restoration

The sixth activity/task of the “R” Project is about Working with the Needy to Improve Creations and Innovation Linked to Restoration.

Like any field or area of life, restoration needs improvements. These improvements can be done through creations and innovations by working together, in particular but not exclusively, with the people in need.

• • What Does Imply Working with Them?

Working with these people to improve creations and innovations linked to restoration can imply taking a number of initiatives such as collaborating with them, communicating with them, and developing a clear understanding of the goals and challenges surrounding creations and innovations about restoration.

This could involve fostering a culture of innovation, including restoration stakeholders from diverse backgrounds, and leveraging various tools and techniques to facilitate brainstorming, ideation, and prototyping.

• • What Else Does Working with Them Require?

It also requires taking the following actions:

~ identifying needs and opportunities by finding out areas in need of restoration and assessing the potential for positive change

~ developing and implementing restoration plans

~ fostering collaboration and communication with different stakeholders (e.g., local authorities, landowners, conservation groups and corporations)

~ monitoring and evaluation by regularly checking restoration efforts using established indicators and metrics to address the effectiveness of the task of Working with the Needy to Improve Creations and Innovation Linked to Restoration.

The above is what Activity/Task 6 of the Restoration (R) Year/Project is about. Those who would like to undertake it, they can go ahead.

For those who need any help before embarking on this activity/task, they can speak to CENFACS.

For any other queries and enquiries about the ‘R‘ project and this year’s dedication, please contact CENFACS as well.

Extra Messages

• Goal of the Month: Reduction of Poverty Stigma for Poor People to Pursue Creative Goals

• Climate-conscious Impact Investing Strategies for Households – In Focus from 04/06/2025: Climate-aligned Portfolios

• Triple Value Initiatives (TVIs)/All Year-round Projects (AYRPs) and the World Environment Day 2025

• Goal of the Month: Reduction of Poverty Stigma for Poor People to Pursue Creative Goals

In order to meet this goal, it is better to explain poverty stigma and our working plan about it as well the implications deriving from this goal.

• • Poverty Stigma and Our Planned Work about It

Poverty stigma refers to the negative beliefs, stereotypes, and discriminatory attitudes directed towards individuals and communities living in poverty. There are two types of poverty stigma: received stigma and perceived stigma. Received stigma is personal experiences of unfair treatment or judgement from others. Perceived stigma is beliefs about how people living on low incomes are treated unfairly by institutions and public services.

It is known that poverty stigma can lead to feelings of shame and hopelessness, making it harder for individuals to pursue their goals, particularly but not limited to creative ambitions and goals.

During this month of Creative Economic Development within CENFACS, it makes sense to help reduce this type of poverty. During this June 2025, we shall raise awareness about the effects of poverty stigma and promote positive narratives about people in poverty to pursue creative endeavours. We shall as well advocate for spaces for creativity, funding, learning and development to be provided to the victims of poverty stigma to realise their creative potentials and projects.

The above is our goal of the month.

• • Implications for Selecting the Goal for the Month

After selecting the goal for the month, we focus our efforts and mind set on the selected goal by making sure that in our real life we apply it. We also expect our supporters to go for the goal of the month by working on the same goal and by supporting those who may be suffering from the type of poverty linked to the goal for the month we are talking about during the given month (e.g., May 2025).

For further details on the goal of the month, its selection procedure including its support and how one can go for it, please contact CENFACS.

• Climate-conscious Impact Investing Strategies for Households – In Focus from 04/06/2025: Climate-aligned Portfolios

To tackle this impact investing strategy, it is better to define it, highlight portfolio alignment metrics and explain how households can align their portfolios.

• • What Is Climate-aligned Portfolio?

Climate alignment of portfolios is about reducing exposure of household portfolios and capturing opportunities by aligning household portfolios with the Paris Agreement; Agreement aiming to limit global temperature rise to well below 2 degrees Celsius, preferably to 1.5 degrees Celsius. This is because climate change creates new risks and opportunities for investors.

Because of the new risks, it is right for climate-conscious household impact investors to go beyond them by considering the environmental and social impacts of their investments. It is equally normal for them to seize new opportunities arising from green investments. There are benefits in doing so as climate-aligned portfolios can potentially offer better long-term returns and reduced risk with companies with strong environmental credentials.

However, to align their portfolios, they may need some guidance or direction to take in terms of metrics or tools.

• • Portfolio Alignment Metrics

This alignment can happen by using alignment metrics, which are mainly three:

1) binary targets (measuring the percentage of portfolio with net-zero or Paris Agreement aligned targets)

2) emissions-based metrics (indicating emissions intensity or absolute emissions)

3) temperature-based metrics (assessing the implied temperature rise from portfolio investments).

According to Lane Clark and Peacock (6),

“Portfolio alignment metrics measure how aligned a portfolio is with a transition to a world targeting a particular climate outcomes, such as limiting temperature rises to well below 2°C, preferably to 1.5°C, as per the Paris Agreement”.

Households can align their portfolios by referring to these metrics.

• • How Can Household Investors Align Their Portfolios?

In their investment strategy, they can do it by

~ halving extreme weather risks that can affect their assets

~ supporting a net-zero strategy when investing

~ minimizing exposure to industries impacted by a green economy shift, such as gas and oil

~ moving their investments from carbon-intensive companies to green alternative ones

etc.

By pursuing the above-mentioned strategies, climate-conscious household impact investors would integrate climate resilience into their investment decision-making processes. Likewise, their asset managers can also assist them in this matter. Those households that are struggling to do it and do not have asset managers for assistance can work with CENFACS.

For any queries and/or enquiries about Climate-aligned Portfolios as well as Climate-conscious Impact Investing Strategies for Households (including how to access these strategies), please do not hesitate to contact CENFACS.

• Triple Value Initiatives (TVIs)/All Year-round Projects (AYRPs) and the World Environment Day 2025

Tomorrow, the World Environment Day (WED) 2025 will be focussing on ending plastic pollution. From ‘worldenvironmentday.global’ (7),

“Plastic pollution exacerbates the deadly impacts of the triple crisis: the crisis of climate change, the crisis of nature, land, and biodiversity loss, and the crisis of pollution and waste”.

As part of this worldwide event day, those of our members who are working on any of the TVIs/AYRPs can reflect the theme of the WED 2025 in the application of their initiatives/projects. They can integrate the theme of ‘Ending Plastic Pollution‘ into them.

Those who have included or will include the features of this campaign in the TVIs/AYRPs can let us know their experience of this inclusion.

Telling and sharing your TVI/AYRP story of the inclusion experience will help

√ contribute to ending plastic pollution

√ reduce the triple crisis (that is, the crisis of climate change, the crisis of nature, land, and biodiversity loss, and the crisis of pollution and waste)

√ improve the environmental aspect within TVI/AYRP

√ know what has worked and not worked so far before TVI’s/AYRP’s deadline of 23/12/2025.

To tell and share your TVI/AYRP story of environmental inclusion and particularly of the inclusion of the theme of WED 2025 , please contact CENFACS.

Message in French (Message en français)

• Activité/Tâche 6 de la Restauration (R) Année/Projet : Travailler avec les Personnes dans le Besoin pour Améliorer les Créations et les Innovation liées à la Restauration

La sixième activité/tâche du projet “R” concerne le travail avec les personnes dans le besoin pour améliorer les créations et les innovations liées à la restauration.

Comme dans tout domaine de la vie, la restauration nécessite des améliorations. Ces améliorations peuvent être réalisées grâce à des créations et des innovations en travaillant ensemble, en particulier mais pas exclusivement, avec les personnes dans le besoin.

• • Que signifie travailler avec ces personnes ?

Travailler avec ces personnes pour améliorer les créations et les innovations liées à la restauration peut impliquer de prendre un certain nombre d’initiatives telles que collaborer avec elles, communiquer avec elles et développer une compréhension claire des objectifs et des défis entourant les créations et les innovations sur la restauration.

Cela pourrait impliquer de promouvoir une culture de l’innovation, y compris les parties prenantes de la restauration provenant de divers horizons, et d’exploiter divers outils et techniques pour faciliter le brainstorming, l’idéation et le prototypage.

• • Que nécessite d’autre le travail avec elles ?

Il nécessite également la prise des mesures suivantes :

~ identifier les besoins et les opportunités en trouvant des zones nécessitant une restauration et en évaluant le potentiel de changement positif

~ développer et mettre en œuvre des plans de restauration

~ favoriser la collaboration et la communication avec différents acteurs (p. ex., les autorités locales, les propriétaires terriens, les groupes de conservation et les entreprises)

~ surveiller et évaluer en vérifiant régulièrement les efforts de restauration à l’aide d’indicateurs et de métriques établis pour évaluer l’efficacité de la tâche visant à travailler avec les nécessiteux/ses pour améliorer les créations et l’innovation liées à la restauration.

Ce qui précède concerne l’Activité/Tâche 6 du projet/année de Restauration (R).

Ceux ou celles qui souhaitent entreprendre cela peuvent y aller. Pour ceux ou celles qui ont besoin d’aide avant de commencer cette activité/tâche, ils/elles peuvent s’adresser à CENFACS.

Pour toute autre question concernant le projet ‘R‘ et la dédication de cette année, veuillez contacter CENFACS également.

Main Development

• Creative Economic Development Month and Jmesci (June Month of Environmental and Sustainable Initiatives) Project 2025

The following points make up the Main Development section of this post:

∝ Basic understanding of the creative economic development

∝ What 2025 June Month of Environmental and Sustainable Creative Initiatives (Jmesci) project will be about

∝ Theme and Sub-themes of Creative Economic Development Month 2025

∝ The kinds of creative economic development projects we will be dealing with

∝ The method of delivering the Creative Economic Development Month

∝ The calendar and contents of the Creative Economic Development Month

∝ Execution of CEDM 2025 Sub-themes: First Codes (from Week Beginning Monday 02/06/2025)

∝Creative Economic Development Projects

∝ Featuring other environmental activities or events outside but closer to CENFACS’ work.

Let us look at these points one by one.

• • Basic Understanding of the Creative Economic Development (CEDM)

To grasp the creative economic development is better to start with the understanding of the creative economy.

• • • Basic understanding of the creative economy

There are many definitions of creative economy. In this communication, we have selected two of them.

The first definition comes from the United Nations Conference on Trade and Development (UNCTAD). UNCTAD (8) argues that a creative economy

“Essentially… is the knowledge-based economic activities upon which the ‘creative industries’ are based”.

The UNCTAD goes on by claiming that

“The creative industries – which include advertising, architecture, arts and crafts, design, fashion, film, video, photography, music, performing arts, publishing, research and development, software, computer games, electronic publishing, and TV/radio – are the lifeblood of the creative economy”.

The second definition, which is from ‘rasmussen.edu’ (9), is

“The creative economy is the income-earning potential of creative activities and ideas”.

Clearly, this second definition focusses on the income generation aspect of creative industries and activities.

However, CENFACS looks at the creative economy from the perspective of development or sustainable development.

• • • Creative economy from the perspective of development and sustainable development

From the development point of view, creative economic development focuses on leveraging creativity and cultural assets to drive economic growth and development process, fostering job creation, attracting investment, and enhancing the overall quality of life in a particular area. It involves creating an environment that supports innovative industries like the arts, film, music, fashion, and design, while also recognising that creativity can enhance various sectors beyond these traditional creative industries.

From the perspective of sustainable development, one needs to include the definition of sustainable development as given by World Commission on Environment and Development (10), definition which is:

“Development that meets the needs of the present without compromising the ability of future generations to meet their own needs”

So, the knowledge-based economic activities – upon which the creative industries are supported – need to be sustainable; that is capable of being continued over the long term without adverse effects. Since, we are pursuing CENFACS’ Programme of ‘Building Forward Better Together to a Greener, Cleaner, Safer, Inclusive and Climate-Resilient Future’; these activities need to be inclusive, clean, green (or net zero), climate-resilient and safe.

• • What June Month of Environmental and Sustainable Initiatives 2025 Is about

Individual and collective creations in the ways of improving lives through the conception of fresh ideas and the implementation of practical ideas to escape from poverty and hardships as well as foster a better environment and sustainability, are CENFACS’ area of interest. We create all over the year and life; however June is the month for us to remember and acknowledge our environmental and sustainable makings.

June is the month of Creative Economic Development at CENFACS with creation and innovation on the main menu: creation for researching and developing fresh ideas to reduce poverty, particularly extreme poverty; innovation for making these ideas or dreams come true, transformable into practical environmental and sustainable initiatives and actions.

Put it simply, Jmesci (June Month of Environmental and Sustainable Creative Initiatives) is just about finding out ways of engineering creations relating to the environment and sustainability in order to further reduce poverty and improve the quality of life. In practical terms, it is the project that features or carries the Creative Economic Development Month (CEDM).

This year’s Jmesci will be about 3 Types of Creations and Innovations:

a) Creations and Innovations overcoming challenges that hinder the ability of poor people to create and innovate

b) Creations and Innovations applying to the use of critical or strategic natural resources or minerals for energy transition and poverty reduction

c) Creations and Innovations dealing with the loss (depreciation or devaluation) of households’ assets value.

• • Theme and Sub-themes of CEDM 2025

The key theme of CEDM 2025 is Creations and Innovations to Reduce Poverty and Enhance Sustainable Development. Within this main theme, we have 3 sub-themes of creations and innovations to offer, which are:

1) challenges hindering the ability of poor people to create and innovate

2) critical and strategic resources or minerals

3) loss (depreciation or devaluation) of assets value.

Let us briefly highlight each of the sub-themes.

• • • Challenges hindering the ability of poor people to create and innovate

Generally speaking, poor people face many challenges that hinder their ability to create and innovate. To mention the few of them, we can include the lack of

~ resources for poor people to invest in creative pursuits

~ budget for discretionary spending on creativity activities

~ knowledge and skills needed for some creative fields

~ infrastructure to foster creativity

~ opportunity to develop their artistic talents

etc.

These challenges need to be addressed.

In the context of CEDM 2025, we are going to work on ways of (or strategies for) addressing these challenges. There are four strategies for overcoming these challenges on which we will be working this month:

a) Investing in education and skills development of poor people

b) Promoting social inclusion and combatting stigma

c) Providing access to resources and opportunities

d) Addressing underlying causes of poverty.

Working on the above-mentioned strategies means find creations and innovations that can help overcome poor people’s barriers to develop their ability to create and innovate.

• • • • Creations and innovations to address the challenges hindering the ability of poor people to create and innovate

Details of these specific creations and innovations have not been given in these CEDM 2025 notes. They will be released in the next notes this month. In meantime, readers can refer to the above-mentioned four strategies for overcoming these challenges.

Those who would be interested in them and their codes, they should not hesitate to contact CENFACS.

• • • Creations and Innovations relating to the use of critical or strategic natural resources or minerals for energy transition and poverty reduction

Perhaps the best way of approaching these creations and innovations is to explain critical and strategic natural resources or minerals, as well as their importance for energy transition and their contribution to poverty reduction. Before explaining them, let us note that the adjectives ‘critical’ and ‘strategic’ are interchangeably used when it is about minerals or natural resources. Their definitions depend on countries that have and listen them.

• • • • What are critical minerals?

The website ‘unu.edu’ (11) states that

“The definition of whether a mineral is considered critical or not is somewhat flexible, since the classification depends on not only the context and the stakeholder’s point of view, but is also subject to change over time because the current techno-socio-economic paradigm largely defines criticality level of minerals”.

The same website ‘unu.edu’ explains that

“Critical minerals are a subset of minerals considered crucial for the manufacturing and technological needs of companies, industries, nations, or even the world”.

Similarly, the website ‘3gimbals.com’ (12) argues that

“A mineral qualifies as critical if its supply is vulnerable to disruption and if it is a key input for technologies ranging from weapons systems and satellites to electric vehicle batteries and semi-conductors”.

Examples of these critical minerals include gallium, battery minerals (such as lithium, cobalt, nickel, and graphite essential for vehicles, energy storage, and many military technologies).

Some these critical minerals can be used for energy transition and/or poverty reduction.

• • • • What are strategic natural resources?

According to ‘studysmarter.co.uk’ (13),

“Strategic natural resources refer to minerals that are vital for a country’s economy and defence capabilities. These resources often have limited availability and are crucial for producing advanced technologies, military equipment, and renewable energy systems. Their scarcity and uneven global distribution make them pivotal in global trade and security policies”.

Examples of strategic minerals include rare earth elements (like neodymium and dysprosium), lithium (critical for battery production is increasingly important in the transition to renewable energy and electric vehicles), cobalt (used in rechargeable batteries), nickel (important for stainless steel production and battery technology), etc.

• • • • Importance of critical and strategic natural resources for energy transition

The above-given examples about lithium, cobalt and nickel already show how some of these critical and strategic natural resources are vital for energy transition. These mineral commodities are not only important for the economy and security for countries and regions of the world that possess; they are also crucial for our journey to energy transition (or the shift from relying on fossil fuels to using clean, renewable energy sources like wind, solar, and hydropower) and for reducing poverty (if the dividends or incomes earned from minerals extraction are equitably shared with local communities or those living in poverty).

• • • • Contribution of critical and strategic natural resources to poverty reduction

Both critical and strategic natural resources can contribute to poverty reduction in countries (like those of Africa) that possess them. They can help create jobs, stimulate economic growth, and increase community well-being in resource rich countries and regions.

For instance, by creating opportunities for employment and economic growth, and investing in social infrastructure, both critical and strategic minerals can play a role in reducing poverty.

However, because of various challenges (like uneven distribution of supply chains in terms of energy transition, barriers to accessing low-carbon technologies and the environmental impacts of the mining operations), there is a need to create and innovate regarding the use of critical and/or strategic natural resources or minerals for energy transition and poverty reduction.

• • • • Creations and Innovations relating to the use of critical or strategic natural resources or minerals

Creations and innovations using critical or strategic minerals, like those in energy transition technologies, can be a powerful tool for poverty reduction. What are these creations and innovations.

• • • • • Creations relating to the use of critical or strategic natural resources or minerals

They are those that deal with global competition, supply chain vulnerabilities, adversarial control over critical materials, mining investments, supply contracts, geopolitical agreements, disruption risks, etc.

However, as part of the CEDM 2025 notes, we shall focus on the following four areas of creations:

σ supply chain vulnerabilities

σ adversarial control over critical materials

σ mining investments

σ geopolitical agreements.

• • • • • Innovations relating to the use of critical or strategic natural resources or minerals

There are countless of innovations applying to the use of critical or strategic natural resources. However, for the convenience of CEDM 2025 notes, we will be working on four areas about these innovations, which are how to

σ ensure reliable access to critical natural resources

σ uphold technological edge in poverty reduction

σ preserve strategic autonomy

σ fortify poverty reduction base.

• • • Creations and Innovations dealing with the loss (depreciation or devaluation) of households’ assets value

Before highlighting these creations and innovations, let us first explain loss of assets value. This loss of assets value can happen in many ways, particularly through depreciation and devaluation (or currency depreciation).

• • • • What is depreciation of assets value?

Loss or depreciation of assets can be explained in many ways. On the website of ‘assetvalueguide.com’ (14), it is stated that

“Depreciation is the loss of value of an asset or class of assets, as they age”.

Another explanation comes ‘fastercapital.com’ (15) which argues that

“Depreciation is the systematic allocation of an asset’s cost over its useful life. It recognizes that assets lose value over time due to factors such as wear and tear, obsolescence, or technological advancements”.

There are basically three methods of working out depreciation which are: straight-line, declining balance, and units of production.

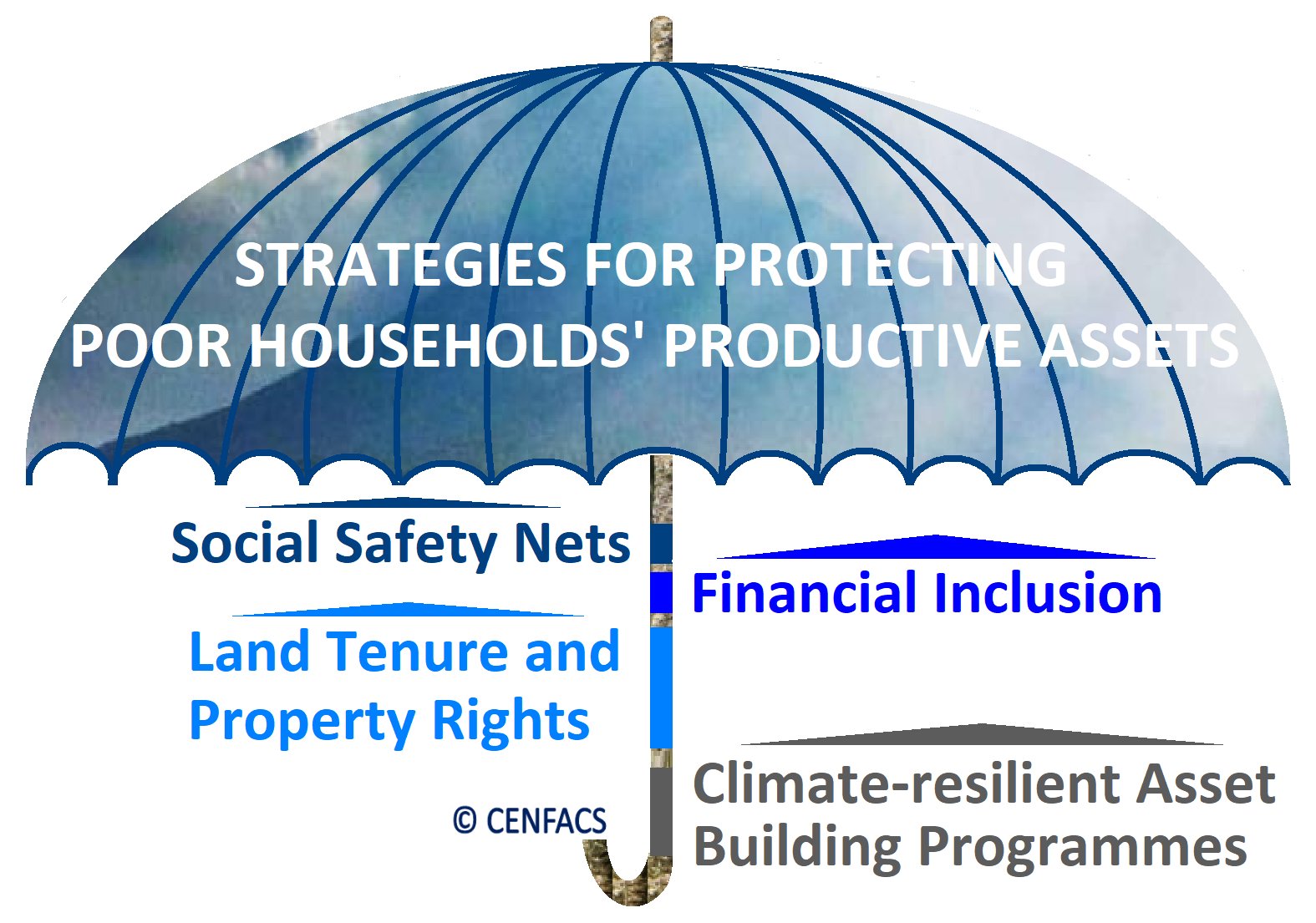

Because the value of assets can depreciate over time, households need some creations and innovations to either restore assets value or replace them.

• • • • What is devaluation?

Oxford Dictionary of Economics written by John Black et al. (16) explains that

“For a country with a pegged exchange rate regime, devaluation is an officially announced lowering in the value of the domestic currency relative to foreign currencies, usually as a means of correcting balance of payment deficit, at least temporarily” (p. 139)

Devaluation or currency depreciation can affect household assets value.

As a result, there could be necessity to create and innovate to deal with the loss of household assets value.

• • • • Creations and Innovations dealing with the loss (depreciation or devaluation) of households’ assets value

• • • • • Creations dealing with the loss (depreciation or devaluation) of households’ assets value

To mitigate households’ loss of assets value, we shall deal with the creations linked to the following:

σ financial modelling and simulations

σ alternative investment strategies

σ financial fictional scenarios

σ systemic issues.

• • • • • Innovations dealing with the loss (depreciation or devaluation) of households’ assets value

To reduce the economic impacts of market fluctuations, inflation and other financial factors on household loss of assets value, we shall consider the following innovative approaches:

σ diversification of investment portfolios

σ affordable insurance options

σ financial literacy programmes

σ user-friendly digital platforms and tools.

The above-mentioned creations and innovations will make up CEDM 2025. They will be part of projects of CEDM 2025.

• • Kinds of Creative Economic Development Projects Dealt with

The types of creative economic development projects that will be considered will be those helping people in need to reduce or end poverty while enhancing sustainable development. In other words, for any creations and innovations to meet the objectives of the creation and innovation month, they need to address poverty while contributing to the principles of sustainable development; that is development that is inclusive, clean, green (or net zero), climate-resilient and safe.

From the idea or conception to the implementation of these projects, their contents need to have the values of poverty reduction and sustainability (particularly the inclusive, clean, green or net zero, climate-resilient and safe aspects of sustainability). As we continue to unveil these projects throughout this month, these values will become clear, apparent and self-explanatory. This will as well determine the manner in which the Creative Economic Development Month will be approached and delivered throughout the month.

• • The Method of Delivering the Creative Economic Development Month

The Creative Economic Development Month will be delivered through the composition of notes and a number of activities (such as workshop, focus group or discussion, exhibition, advocacy or campaign and appeal).

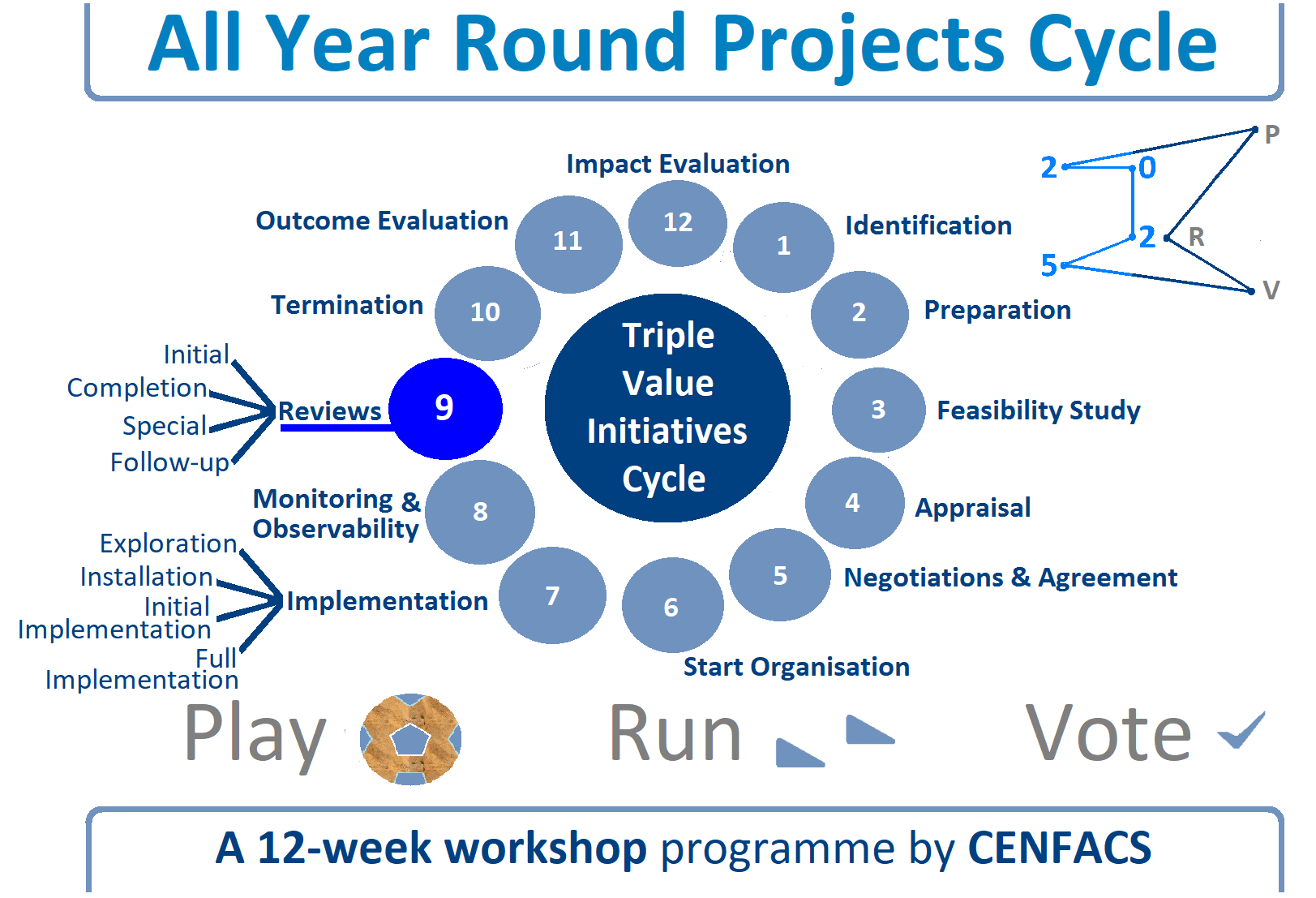

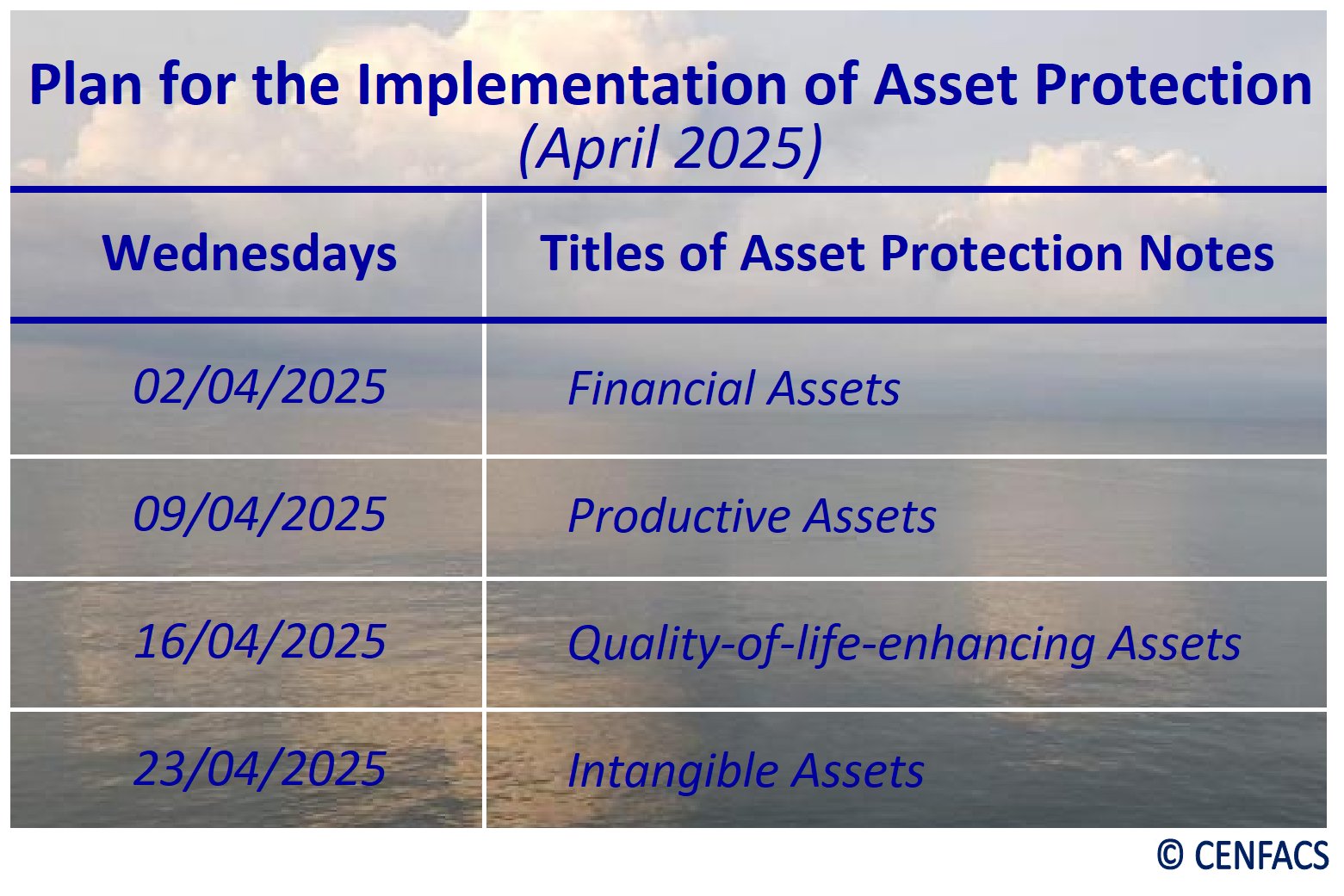

• • The Calendar and Contents of the Creative Economic Development Month

To deliver on what we have argued so far, we have organised the Creative Economic Development Month (CEDM) as indicated in the figure below.

On the above figure, C means creation while I signifies innovation. As shown in the same figure, Sub-theme 1 does not make any difference between creations and innovations.

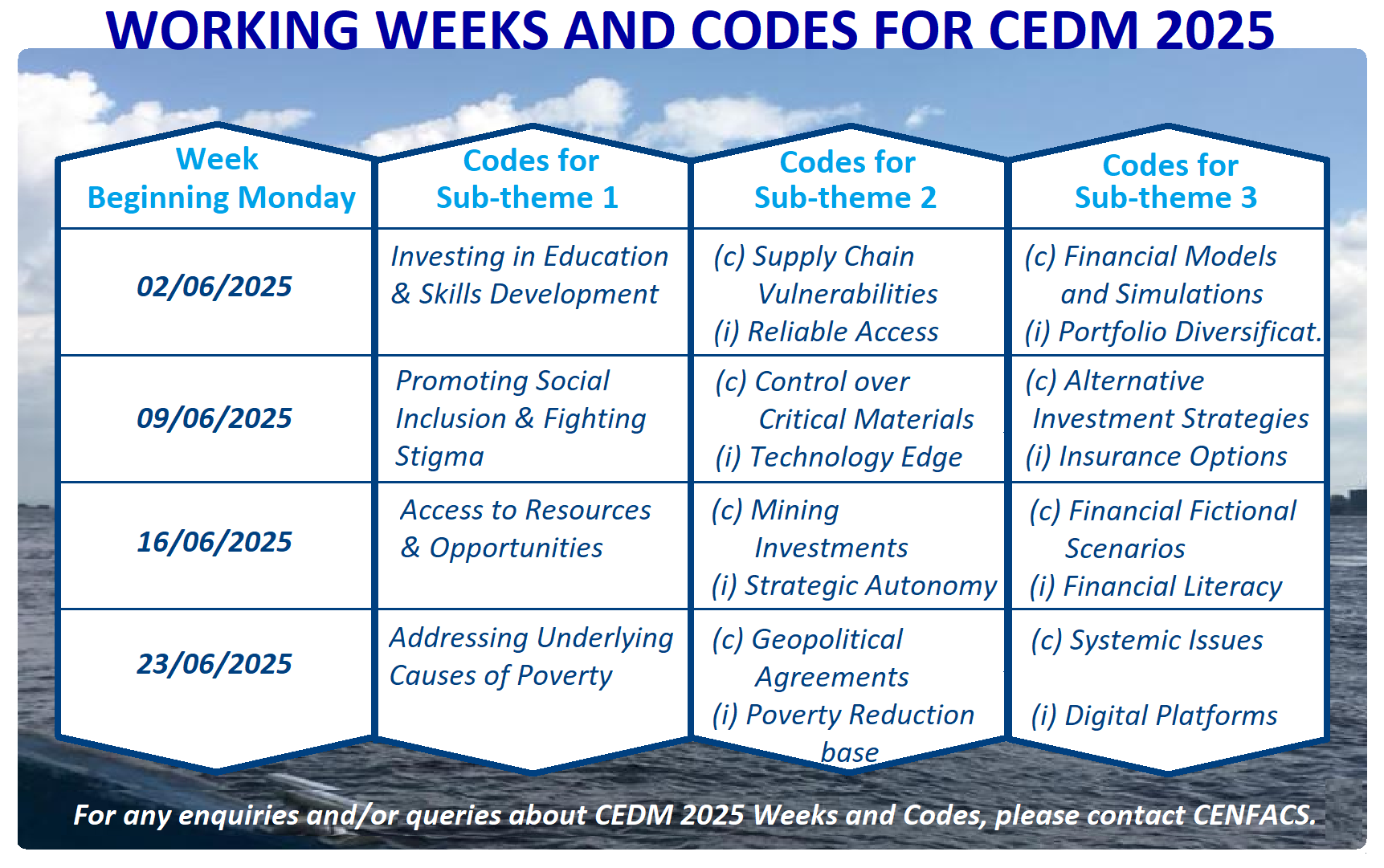

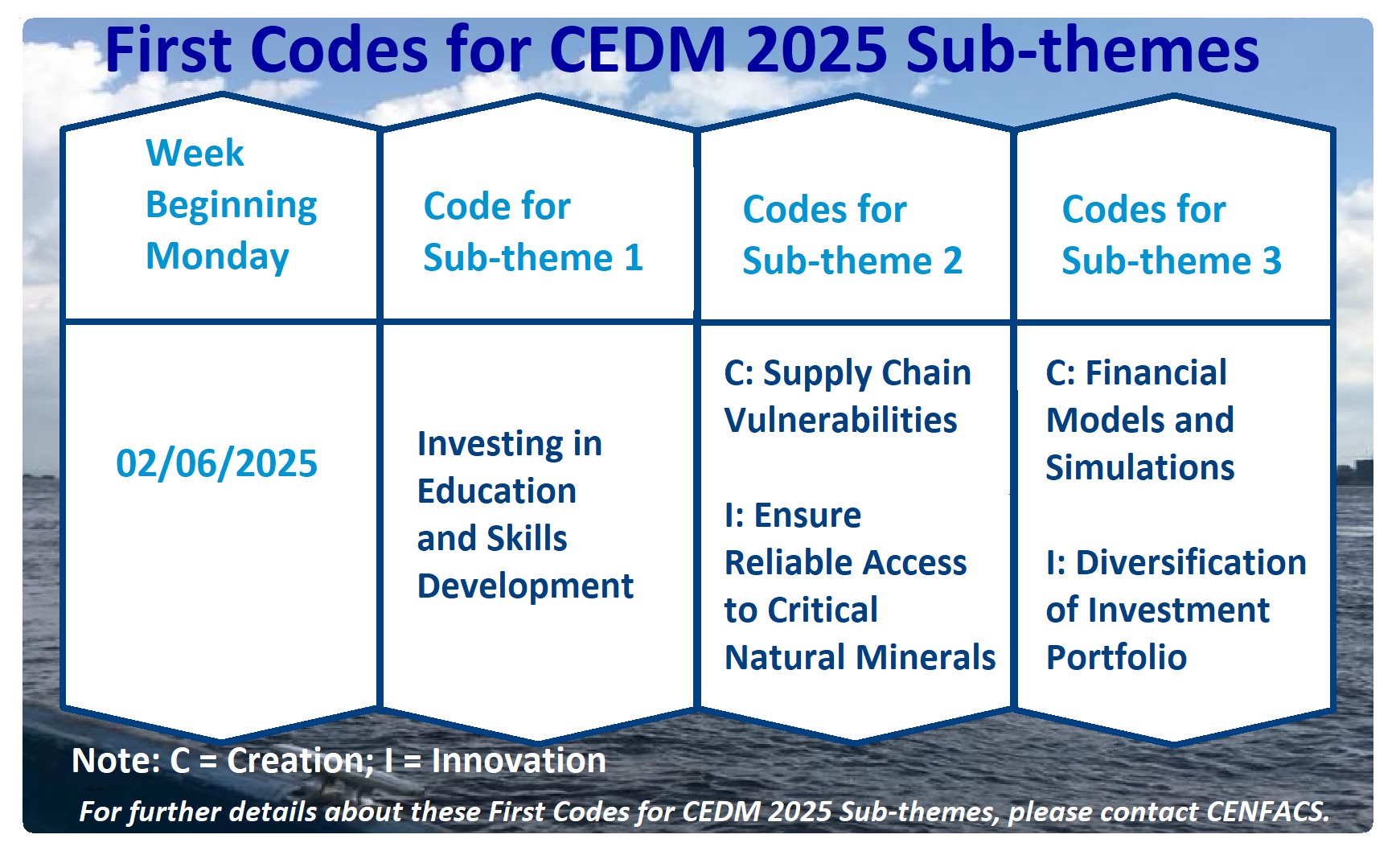

• • Execution of CEDM 2025 Sub-themes: First Codes (from Week Beginning Monday 02/06/2025)

Our CEDM Working Weeks and Plan starts with the first codes for each sub-theme, which are

~ Investing in education and skills development of poor people for sub-theme 1 (ST1)

~ Supply chain vulnerabilities for Creations in sub-theme 2 (ST2.1)

~ Reliable access to critical natural resources for Innovations in sub-theme 2 (ST2.2)

~ Financial modelling and simulations for Creations in sub-theme 3 (ST3.1)

~ Investment portfolio diversification for Innovations in sub-theme 3 (ST3.2).

Those who would like to engage with the CEDM 2025 can choose amongst the above-mentioned codes and contact CENFACS.

For example, if one wants to know more about how Investing in Education and Skills Development of Poor People can help them overcome challenges hindering the their ability to create and innovate, they can contact CENFACS to discuss it or participate in one of the activities to be organised about it.

Likewise, using critical or strategic minerals, like those in energy transition technologies, can be a powerful tool for poverty reduction. Those who may be interested in learning creations relating to Supply Chain Vulnerabilities and innovations for Reliable Access to Critical Natural Resources that can help energy transition and reduce poverty can work with CENFACS on these matters.

Equally, to mitigate households’ loss of assets value it could require households to create New Financial Models and Simulations, and to innovate by Diversifying Their Investment Portfolio Diversification.

The above is the first execution of our CEDM 2025 Working Weeks and Plan. For those who may be interested in any of the first codes of each sub-theme of this plan, they can contact CENFACS. For those would like to learn more about CEDM 2025, they can also communicate with CENFACS.

• • Creative Economic Development Projects

There are areas of creative economic industries upon which we (together with those in need) draw inspiration to develop projects to help reduce poverty and enhance sustainable development. These areas include: advertising, arts and crafts, design, video, research and development.

To be more specific, let us look at one example, one activity and one competition relating to creative economic development projects.

• • • Example of Creative Economic Development Project: Art and Design for Poverty Reduction and Sustainable Development

CENFACS’ creative economic development projects (like Art and Design for Poverty Reduction and Sustainable Development) can help users to handle squeezed household life-sustaining spending.

For example, we normally run Art and Design for Poverty Reduction and Sustainable Development as a creative economic development or creative economy project. Through this project, participants can unlock their creative aspirations to build and develop poverty reduction content-creating objects or materials. This exercise will provide them with poverty reduction building experiences via objects/materials.

• • • Creative Economic Development Activity of the Month: Construct and Post e-cards or e-objects

One of the activities related to this project for this year will be to construct and post e-cards or e-objects expressing the theme of “Ending Plastic Pollution”. The construction will echo the World Environmental Day’s (op. cit.) celebratory theme of tomorrow 05/06/2025.

One can as well construct and post the similar cards as expressions or ways of dealing with drought to resonate the World Day to Combat Desertification and Drought (17) on 17/06/2025. The theme of 2025 Desertification and Drought Day is “Restore the Land. Unlock the Opportunities”.

So, those who wish and want can design and post an e-card or e-object to feature the theme of “Ending Plastic Pollution” relating to World Environment Day, and/or the theme of “Restore the Land. Unlock the Opportunities” linked to the World Day to Combat Desertification and Drought.

To support and or enquire about Art and Design for Poverty Relief and Sustainable Development, please contact CENFACS.

• • • Creative Economic Development Competition of the Month: The Creative Mind of Poverty Reduction and Sustainable Development

The Creative Mind of Poverty Reduction and Sustainable Development is a one-month’s project of challenge created and run by CENFACS that will enable creators and innovators of the month to showcase their creations and innovations in and for the community; creations and innovations relating to poverty reduction and sustainable development.

As a creator or innovator of poverty reduction and/or sustainable development you can tell and/or share with CENFACS your creation and/or innovation project or experience of creative and/or innovative poverty reduction and/or sustainable development. Your creation and/or innovation project or experience will be part of this month’s challenge to find the Creative Mind of Poverty Reduction and Sustainable Development.

To tell and/or share your creation and/or innovation project or experience, please contact CENFACS this month.

• • Featuring other environmental activities or events outside but closer to CENFACS’ work

Our month of creation (of thinking up new things) and innovation (of converting our thoughts into tangible outcomes) revolves around global, national, and local environmental and sustainable issues and events of the month as well.

Examples of June world environmental events and days of the month include the following events (we have already mentioned some of them):

∝ London Climate Action Week (18) which will take place 21 to 29 June 2025

∝ The United Nations World Environment Day which is being held today 05/06/2025 under the theme of ‘Ending Plastic Pollution’

∝ The World Day to Combat Desertification and Drought 2024 to be held on 17/06/2025 under the theme of ‘Restore the Land. Unlock the Opportunities’.

The above notes are for CENFACS’ Creative Economic Development Month.

To support and or engage with CENFACS’ Creative Economic Development Month and or the project Jmesci 2025, please contact CENFACS.

_________

• References

(1) https://worldcreativityday.com/en#:~text=… (accessed in June 2025)

(2) https://www.wallstreetmojo.com/market-analysis/ (accessed in June 2025)

(3) https://6b.digital/insights/what-is-a-feature-in-software-development (accessed in June 2025)

(4) https://www.optimizely.com/optimization-glossary/ (accessed in June 2025)

(5) https://www.sciencedirect.com/topics/computer-science/feature-based-design#:~text(accessed in June 2025)

(6) https://www.lcp.com/media/cvypelgw/portfolio-alignment-metrics-june-2022.pdf#:~text= (accessed in June 2025)

(7) https://www.worldenvironmentday.global/about/theme-host#::~text (accessed in June 2025)

(8) https://unctad.org/en/Pages/DITC/CreativeEconomy/Creative-Economy-Programme.aspx (accessed in May 2023)

(9) https://www.rasmussen.edu/degrees/design/blog/what-is-the-creative-economy/ (accessed in June 2023)

(10) Brundtland et al. (1987), Our Common Future, World Commission on Environment and Development (The Brundtland Report), Oxford University Press, London

(11) https://unu.edu/merit/news/what-are-critical-minerals-and-why-are-they-so-important#:~:text (accessed in June 2025)

(12) https://3gimbals.com/insights/strategic-natural-resources-and-u-s-national-security-in-a-resource-hungry-world/ (accessed in June 2025)

(13) https://www.studysmarter.co.uk/explanations/environmental-science/geology/strategic-minerals/ (accessed in June 2025)

(14) https://www.assetvalueguide.com/chapter/6-depreciation/ (accessed in June 2025)

(15) https://fastercapital.com/content/Depreciation-How-to-Account-for-the-Loss-of-Value-of-an-Asset-over-Time.html#Understanding-Depreciation (accessed in June 2025)

(16) Black, J., Hashimzade, N. & Myles, G. (2017), Oxford Dictionary of Economics, Fifth Ed., Oxford University Press, UK

(17) https://www.unccd.int/events/desertification-drought-day/2025 (accessed in June 2025)

(18) https://www.londonclimateactionweek.org (accessed in June 2025)

_________

• Help CENFACS Keep the Poverty Relief Work Going This Year

We do our work on a very small budget and on a voluntary basis. Making a donation will show us you value our work and support CENFACS’ work, which is currently offered as a free service.

One could also consider a recurring donation to CENFACS in the future.

Additionally, we would like to inform you that planned gifting is always an option for giving at CENFACS. Likewise, CENFACS accepts matching gifts from companies running a gift-matching programme.

Donate to support CENFACS!

FOR ONLY £1, YOU CAN SUPPORT CENFACS AND CENFACS’ NOBLE AND BEAUTIFUL CAUSES OF POVERTY REDUCTION.

JUST GO TO: Support Causes – (cenfacs.org.uk)

Thank you for visiting CENFACS website and reading this post.

Thank you as well to those who made or make comments about our weekly posts.

We look forward to receiving your regular visits and continuing support until the end of 2025 and beyond.

With many thanks.