Welcome to CENFACS’ Online Diary!

08 May 2024

Post No. 351

The Week’s Contents

• Financial Resilience Programme for Households (FRP4Hs) – In Focus for Wednesday 08/05/2024: Outcome and Impact of FRP4Hs on Households

• All in Development Stories (AiDS) Serial 2: Stories of Creating Metrics and Looking at Changing Patterns (Starting from Wednesday 08/05/2024)

• Goal of the Month: Make Poverty Reduction Happen through Stories

… And much more!

Key Messages

• Financial Resilience Programme for Households (FRP4Hs) – In Focus for Wednesday 08/05/2024: Outcome and Impact of FRP4Hs on Households

The last theme of our work on financial asset holdings of households or economic resources that households possess to help them stay resilient against shocks focusses on the Outcome and Impact of Financial Resilience Programme for Households (FRP4Hs) on Households.

Indeed, one thing is to set up and deliver a programme, another thing is to check that this programme results in short-term positive changes and effects on its intended beneficiaries (here households) as well as in broader and long-term changes on the same beneficiaries. In programme planning jargon and parlance, the two operations or steps are called outcome and impact.

In practical terms, if you are a household and has been followed the FRP4Hs, you may want to know what this programme is going to achieve for you in short, medium and long term.

In short term, it is possible to get some results from the implementation of the programme at household level. In the long term, it may take sometimes to know if what happens to a particular household is the result of the FRP4Hs or not. Also, regardless of the length of the term, one needs to have household data and use metrics or indicators in order to argue about outcome and impact. However, before these outcome and impact happen we can work with households to inform them what could be the outcome and/or impact of a programme such as FRP4Hs if they apply it.

In this last theme, we are thus looking at the possible outcome and impact that may result from the application of the FRP4Hs. Bearing in mind that each household is different and specific. They have their own financial problems, strengths, weaknesses, capacities and capabilities to be or not to be resilient from income or expense shocks when these shocks occur. What FRP4Hs is trying to do is to increase their financial strengths while reducing their financial weaknesses or vulnerabilities.

To find out more about the possible outcome and impact of the FRP4Hs, please read under the Main Development section of this post.

• All in Development Stories (AiDS) Serial 2: Stories of Creating Metrics and Looking at Changing Patterns (Starting from Wednesday 08/05/2024)

Our two-story series continues with Serial 2, which covers Stories of Creating Metrics and Stories of Looking at Changing Patterns. Let us highlight each of these stories.

• • Stories of Creating Metrics

To understand these stories, one may need to know the meaning of metrics.

• • • Brief explanation of metrics

To explain metrics, we are going to refer to what ‘chisellabs.com’ (1) argues about them, which is

“Metrics are quantifiable measurements used to assess performance, track progress, and measure the success of various processes, initiatives, or entities. They provide objective and tangible data that allow organisations to make informed decisions, identify improvement areas, and monitor strategies’ effectiveness”.

Additionally, ‘digitalocean.com’ (2) explains why metrics are useful in these terms:

“Metrics are useful because they provide insight into the behaviour and health of your systems, especially when analysed in aggregate”.

For ‘digitalocean.com’, metrics related to system can include host-based metrics, application metrics, network and connectivity metrics, server pool metrics, external dependency metrics, etc.

Metrics can help to monitor our poverty reduction system. In this respect, ‘batimes.com’ (3) argues that

“Metrics can be a powerful tool for informing and guiding decision making at all levels of an organisation… In order for metrics to deliver value rather than distraction, they must be clearly defined, completely understood and broadly communicated, as well as focused on the areas that are most important to the success of an organisation”.

Knowing what metrics are, it is possible to extract the Stories of Creating Metrics.

• • • Stories of Creating Metrics

Stories of Creating Metrics are the narratives of creating new metrics to reset systems – our poverty reduction system.

They are those of

√ factorizing into the development of metrics or quantitative methods the culture and needs of the people in need

√ educating people before adopting metrics

√ aligning metrics with the vision, mission and goals of any poverty reduction system.

If you are part of a media organisation and drawing from, for example, what ‘mediashift.org’ (4) explains, telling the stories of creating metrics would be about sharing your experiencing stories on the following:

~ how to identify the metrics that matter for your organisation

~ how to make metrics useful – where useful equals actionable

~ how to report smarter, not harder.

If you are a member of CENFACS Community and have these types of story, please do not hesitate to tell and share your stories with CENFACS. If you are not our member, you can still submit your story.

To donate, tell and share your storying gift of Stories of Creating Metrics, please contact CENFACS.

• • Stories of Looking at Changing Patterns

To deal with these stories, let us clarify the concept of patterns of change.

• • • Clarification of the concept of patterns of change

This clarification has been provided by Raulo et al. (5), who argue that

“Patterns of change describe how success and composition of every entity, from species to societies, vary across. The notions of change, such as birth, death, growth, evolution and longevity, extend across reality including biological, cultural and societal phenomena”.

Another explanation of the concept of patterns of change comes from ‘britannica.com’ (6). For ‘britannica.com’, patterns of change are studied by social scientists or theoreticians who recognise three traditional ideas of social change – decline, cyclic change, and progress. Still from the view of ‘britannica.com’, short-term tends to be cyclic while long-term change tends to follow one direction.

By looking at the patterns of change in our system of poverty reduction, we can ask ourselves if the patterns of change are cyclic or one-directional. However, if our task is to look at patterns of change over the long term , then we can follow the model or theory of long-term cyclic changes, which is birth, growth, flourishing, decline, and death of a system.

From the above definitions and observations, we can develop our Stories of Looking at Changing Patterns.

• • • Stories of Looking at Changing Patterns

Stories of Looking at Changing Patterns are the plots of looking at patterns of change rather than static snapshots.

They are the stories of

√ recognizing models or patterns (for example, if our system of poverty reduction is patterned, then one needs to recognise it)

√ acknowledging that situations repeat themselves over and over again

√ vicious circle in some systems of poverty reduction

√ failing to change the way in which a system works

√ going around in circles to deal with a system

√ resolving the problems linked to the way a system is patterned or operating

√ seeing patterns of change problems as an opportunity rather than a misfortune

√ listening your feelings and intuition to recognise patterns

√ overcoming difficulties in understanding patterns

etc.

Briefly speaking, Stories of Looking at Changing Patterns can tell us if a system is in decline, cyclic change, and progress.

If you are a member of our community – the CENFACS Community – and have these types of story, please do not hesitate to tell and share your stories with CENFACS. If you are not our member, you can still submit your story.

To donate, tell and share your storying gift of Stories of Looking at Changing Patterns, please contact CENFACS.

• Goal of the Month: Make Poverty Reduction Happen through Stories

Our poverty reduction goal for May 2024 is Making Poverty Reduction Happen through Stories. It is about telling and sharing stories that can pitch or lead to poverty reduction and sustainable development for the poor and those CENFACS Community members who may need inspiring and motivational stories to navigate their ways out the problems they have. In other words, by listening, viewing and learning from inspiring stories they can develop their own strengths to gradually find their own pace and tune towards the reduction of poverty and the enhancement of sustainable development.

To put this into perspective, Pullanikkatil and Shackleton (7) give the example of Poverty Reduction through Non-Timber Forest Products. Referring to the work of Pullanikkatil and Shackleton, Sarah Feder (8) explains that

“Stories can amplify the voices of people who are not often heard, and make their experiences relatable to people in wildly different contexts”.

Likewise, Angela Wood and John Barnes (9) are in favour of

“Amplifying poor people’s voices by combining alternative media such as community radio, oral testimonies and community theatre with the involvement of the media”.

It is possible to deduct from these two quotations that stories can have the following attributes:

σ to amplify poor people’s voices

σ to provide a voice for the voiceless people

σ to create opportunity for these people to narrate from their own perspective

σ to learn lessons to be used in poverty reduction policies, practices and strategies

σ to create and sustain poverty reduction and sustainable development.

Those who can help to make poverty reduction happen through stories, they can be supportive of this goal. We expect our supporters and audiences to support this goal as well.

For further details on this goal including its support, please contact CENFACS.

Extra Messages

• All-year Round Projects Cycle (Triple Value Initiatives Cycle) – Step/Workshop 12: Impact Evaluating Your Play, Run and Vote Projects

• Nature Projects and Nature-based Solutions to Poverty – From Week Beginning Monday 13/05/2024: A Survey on Green Bonds (Activity 2)

• ReLive Issue No. 16, Spring 2024: Will You Help The Conflict-related Acute Food Insecure in Africa to Rebuild and Renew Their Lives?

• All-year Round Projects Cycle (Triple Value Initiatives Cycle) – Step/Workshop 12: Impact Evaluating Your Play, Run and Vote Projects

In Step/Workshop 11 of your Play, Run and Vote Projects, you conducted an outcome evaluation by measuring your behaviour, participation to and achievement following the delivery of these projects. Now, you can proceed with an impact evaluation. An impact evaluation will help to evaluate the effect of your Play, Run and Vote Projects on you and the environment surrounding you. But, what is an impact evaluation?

• • Basic Understanding of an Impact Evaluation

The definition we have chosen to understand an impact evaluation comes from ‘betterevaluation.org’ (10). According to ‘betterevaluation.org’,

“An impact evaluation provides information about the impacts produced by an intervention. The intervention might be a small project, a large programme, a collection of activities, or a policy”.

The same ‘betterevaluation.org’ states that

“A impact evaluation can be undertaken to improve or reorient an intervention (i.e., for formative purposes) or to inform decisions about whether to continue, discontinue, replicate or scale up an intervention (i.e., for summative purposes)”.

In other words, an impact evaluation tries to measure the difference between outcomes with an intervention and without it in a way that can attribute the difference to the intervention, and only the intervention. For instance, an impact evaluation of your Run Project will assess changes in your wellbeing that can be attributable to your Run Project. The figure below is an impact evaluation exercise showing how your all-year-round project can impact on you.

To carry out an impact evaluation, one needs to answer/know the why, when, what and who to engage in the evaluation process. Also, one can base its impact evaluation on a particular way of thinking or a theory.

• • Theories to Be Used in Your Impact Evaluation

To simplify the matter, an all-year-round project beneficiary will use a theory of change that will guide them to causal attribution or to answer cause-and-effect questions; meaning that changes in outcome are directly attributable to an intervention (here your Play, Run and Vote Projects). Therefore, you need to better plan and manage your impact evaluation.

• • Example of Planning and Managing the Impact Evaluation of Your All-year Round Projects

To better plan and manage the impact evaluation of Your All-year Round Projects, you can proceed with the following:

σ Describe what needs to be evaluated

σ Identify and mobilise resources for your evaluation

σ Decide who will conduct the evaluation and engage it

σ Set up an evaluation methodology/approach/technique

σ Manage your evaluation work

σ Implement your evaluation work

σ Evaluate the result/impact of Your All-year Round Projects on you and/or others

σ Share your evaluation results/report.

The above is one of the possible ways of impact evaluating your All-year Round Projects. For those who would like to dive deeper into Impact Evaluation of their Play or Run or Vote project, they should not hesitate to contact CENFACS.

• • Concluding Note about This 12-week Workshop Programme

To conclude this 12-week workshop programme, we would like to thank those who have been engaged with it.

We would like to ask to those who can to measure the impact and effectiveness in working with them/you on how to plan, execute and evaluate your All-year Round Projects.

For example, they/you can state that on overall they/you have positive or negative impacts from this programme. They/you can send your statement to CENFACS‘ usual contact details as given on this website.

Those who need help for any aspect of the plan of their All-year Round Projects, they should not hesitate to contact CENFACS.

Good luck with their/your All-year Round Projects!

• Nature Projects and Nature-based Solutions to Poverty –

From Week Beginning Monday 13/05/2024: A Survey on Green Bonds (Activity 2)

To introduce Activity 2 of the fourth series of Nature Projects and Nature-based Solutions to Poverty, let us summarily define green bonds.

• • What Are Green Bonds?

To understand green bonds, it is better to know bonds. According to the World Bank (11),

“A bond is a form of debt security. A debt security is a legal contract for money owed that can be bought and sold between parties”.

What are green bonds?

Our understanding of green bonds comes from ‘weforum.org’ (12), which explains that

“Green bonds work like regular bonds with one key difference: the money raised from investors is used exclusively to finance projects that have a positive environmental impact such as renewable energy and green buildings”.

The above-mentioned definitions will be used in our survey.

• • Aim of Activity 2

This is an exercise in which we intend to look at in detail debt securities with a view that the money raised from investors is solely used to fund projects with positive impact on the environment.

For example, it is known that the issuance of bonds together with the development of green, social and sustainable bond market are important in Africa in the fight against climate change and in the upkeep of nature. They represent investment opportunities to protect the nature and generate resources for poverty reduction and sustainable development in Africa. In particular, green bonds can finance a portfolio of environmentally friendly investments and fund climate change initiatives.

• • What the Survey Is about

The survey is about the market pricing of green bonds. It is as well dealing with the economic and environmental effects of green bond financing on poverty reduction and sustainable development. The survey focuses on the challenges and opportunities for developing and sustaining green bonds in Africa.

• • Participating to the Survey on Green Bonds

As part of the survey, we are running a questionnaire which will contain some questions to be answered by those willing to respond. You can contribute your answer and respond to the survey.

Participation to this survey is voluntary.

For those who would like to engage with Activity 2, they should not hesitate to contact CENFACS.

For those who would like to find out more about Nature Projects and Nature-based Solutions to Poverty, they can also communicate with CENFACS.

• ReLive Issue No. 16, Spring 2024: Will You Help The Conflict-related Acute Food Insecure in Africa to Rebuild and Renew Their Lives?

This Spring, we are running 14 Gifts in a world of 20 Reliefs or Helpful Differences. What does this mean?

It means donors or funders have 14 Gifts of Renewing Lives to choose from and 20 Reliefs to select from to make helpful differences to the food insecure.

In total, our Spring Relief campaign is providing to potential supporters 14 GIFTS of rebuilding lives in the three African Countries (i.e., Central African Republic, Chad and the Democratic Republic of Congo) in 20 RELIEFS to make this happen.

For this renewal to happen, support is needed towards LRPs.

To support, go to http://cenfacs.org.uk/supporting-us/

Message in French (Message en français)

• Activité/Tâche 5 de l’année/du projet Transitions (t) : Raconter des histoires inspirantes de transitions pour sortir de la pauvreté

La cinquième activité/tâche du projet «t» consiste à partager avec ceux/celles qui en ont besoin des histoires inspirantes sur la transition vers la sortie de la pauvreté. Selon les circonstances de la vie, les gens peuvent entrer dans la pauvreté et en sortir. Cette transition peut être courte ou longue. Ce qui nous intéresse, ce sont les transitions pour sortir de la pauvreté et leur inspiration en termes d’histoire.

• • Transition pour sortir de la pauvreté

De nombreux facteurs peuvent déterminer la sortie de la pauvreté. Ann Huff Stevens (13) en donne quelques-unes dans le cas des États-Unis d’Amérique. D’après elle,

«Les changements dans les revenus et la structure familiale sont associés à la sortie de la pauvreté».

Elle soutient également qu’elle dépend d’une pauvreté circonstancielle à court terme ou d’une pauvreté à long terme associée à des limitations permanentes des revenus, de l’emploi et de la structure familiale.

S’inspirant de l’argument d’Ann Huff Stevens, l’activité/tâche 5 de l’année/du projet Transitions (t) consiste à fournir des histoires de transitions hors de la pauvreté.

• • Fournir des histoires inspirantes de transitions pour sortir de la pauvreté

Il s’agit de donner des témoignages édifiants sur vous ou sur des personnes que vous connaissez qui sont sorties de la pauvreté. L’histoire doit mentionner depuis combien de temps elles sont sorties de la pauvreté et combien de temps dure la transition.

Par exemple, on peut raconter des histoires sur les changements dans la structure des ménages ou sur les changements sur le marché du travail et sur la façon dont ils ont aidé à sortir de la pauvreté. Des histoires comme celles-ci peuvent en inspirer d’autres.

Ce qui précède est l’objet de l’activité/tâche 5. Pour ceux/celles qui ont besoin d’aide avant de se lancer dans cette activité/tâche, ils/elles peuvent s’adresser au CENFACS.

Pour toute autre question ou demande de renseignements sur le projet «t» et la dédicace de cette année, veuillez également contacter le CENFACS.

Main Development

• Financial Resilience Programme for Households (FRP4Hs) – In Focus for Wednesday 08/05/2024: Outcome and Impact of FRP4Hs on Households

The following items cover the Outcome and Impact of FRP4Hs on Households:

σ What Are Outcome and Impact?

σ What Are Outcome and Impact in the Context of FRP4Hs on Households?

σ Types of Changes and Effects that FRP4Hs Can Bring to Households

σ How to Measure Changes and Effects from FRP4Hs for Households: Key Indicators of Financial Resilience

σ Working with Households on Effects and Changes from the Application of FRP4Hs

σ Final Words about FRP4Hs for Households

Let us develop each of the above-mentioned points.

• • What Are Outcome and Impact?

Outcome and impact are part of the steps in any programme or project planning and implementation. Because of that, it will be wrong for us to speak about financial resilience for households without explaining what could be the result on them. So, what is outcome and what is impact?

According to Sally Cupitt with Jean Ellis (14),

“Outcomes are all the changes and effects that happen as a result of your work. Impact is the broad, long term effects of your work” (p. 3)

As one can notice, there is a difference between the two. This difference is stressed by ‘impactio.com’.

Highlighting the difference between ‘Impact’ and ‘Outcome’ in Research Findings, ‘impactio.com’ (15) explains that

“The outcomes are directly correlated to the findings. Outcomes drive a short-term or immediate change in the reader as a result of the information that came from the research itself… An impact, on the other hand, is a more significant, wider change. Impacts are the result of the outcome being put into place in society or the academic world”.

The above-mentioned definitions can be applied to households.

• • What Are Outcome and Impact in the Context of FRP4Hs on Households?

Outcomes are the short- and medium-term effects that households would like to see as a result of the application of FRP4Hs. Impacts are long-term effects to be produced by the FRP4Hs.

For households following the FRP4Hs, outcomes can be they become more confident and aware in the way they approach financial resilience. There could be as well that they improve their financial communication and skills as they feel motivate and aspire on the way they can tackle potential income or expense shocks.

For households following the FRP4Hs, impacts can be health impact, consumption impact, well-being impact, impact on children for those that have kids, housing impact, etc. There could also be a shift in the way they think and behave regarding financial matters, as well as in the way the design their household financial policies and rules.

• • Types of Changes and Effects that FRP4Hs Can Bring to Households

Financial resilience outcome and impact for households can be expressed in many ways as highlighted below.

Expressed as short- and medium-term effects, it is when households can

√ improve their skills to manage budgets and their savings

√ widen their access to affordable credit

√ understand financial risks and contexts

√ make good financial decision

√ learn the range of liquidities and how to access them to offset any potential financial risks, particularly for liquidity-constrained households

√ improve their sense of financial wellness or subjective financial well-being

√ mitigate the impacts of income or expense shocks

√ buffer themselves against these shocks

etc.

Expressed as long-term effects, it is when households can

√ become less financially vulnerable and distressed to the problems of getting to the end of month and/or the inability to face unexpected expenses

√ be without or with less unsecured debt (e.g., consumer credit)

√ be less impulsive with good financial and spending behaviour

√ reduce the effects of unexpected negative income or expense shocks, especially for low-income ones which may experience these shocks at disproportionally high rates

etc.

• • How to Measure Changes and Effects from FRP4Hs for Households: Key Indicators of Financial Resilience

Many of the measures to be used here fall under the scope of financial resilience. We are limiting ourselves to key indicators. Amongst them are Financial Resilience Index, Households’ Savings to Income, Households’ Debt to Income. Let us consider Financial resilience Index and the other measures.

• • • Key Indicators of Financial Resilience

• • • • Financial Resilience Index

This index can be perceived in many ways. From the perspective of Chartered Institute of Public Finance and Accountancy (16),

“Financial Resilience Index shows a council’s position on a range of measures associated with financial risk highlighting where additional scrutiny may be required”.

Although the Chartered Institute of Public Finance and Accountancy speaks about council, the spheres of implementation of its view on financial resilience can be extended to include households. So, Financial Resilience Index for Households shows a household’s position on a range of measures associated with financial risk highlighting where additional scrutiny may be required.

• • • • Other Measures of Financial Resilience

Amongst the other indicators that can use to improve the ability to recover from financial shocks are:

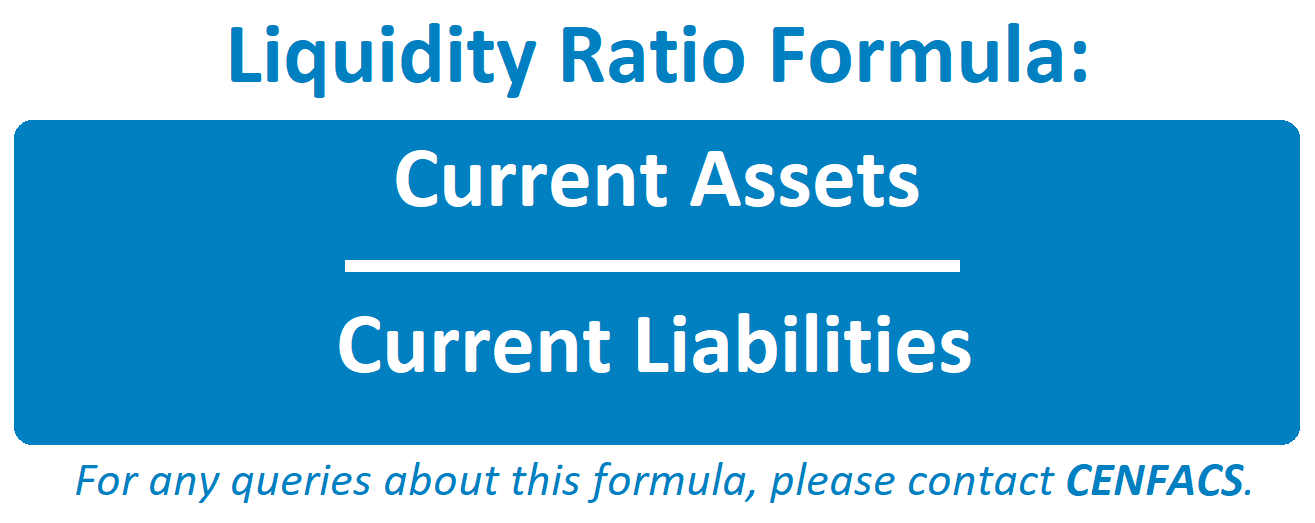

a) The value of savings and liquid financial assets that could be drawn on in times of need

By using financial ratios, this value can be expressed as follows:

Savings / Income or Liquid financial assets / Income

b) Subjective assessments of the ability to cope with financial shocks

c) Measures of financial literacy, numeracy, communications and technology (e.g., financial awareness, use of e-finance, ability to make financial decision, etc.)

d) Measures of financial capability (e.g., soundly managing money, surviving financial shock waves)

e) Measures of capturing financial anxiety, distress or from difficulty, which can be written in the form of financial ratios like

Financial Assets / Debt or Credit / Income

f) Over-indebtedness measures

Etc.

Many of these measures can be found in the work of Abigail McKnight and Mark Rucci (17).

What is important is not to list these measures. What is meaningful is for households to understand the key indicators of financial resilience and help them stay resilient if they follow the underlying advice contained in these indicators.

• • Working with Households on Effects and Changes from the Application of FRP4Hs

Working with households on the effects and changes resulting from financial resilience programmes is about helping them to avoid costly financial mistakes. It is also about reassuring them that there is always support for those households that would like to learn to shield themselves from income or expense shocks.

For example, if liquidity-constrained households are not sure how financial resilience programmes can help them, we can conduct financial resilience needs assessment to determine whether or not this type of programmes can be beneficial to them as well as the areas of their finances that need support in the form of advice and guidance.

The above is the fourth and last theme of our FRP4Hs.

Those households that would like to access the FRP4Hs so that this programme can positively affect and change their life to stay resilient, they can work with CENFACS.

For any queries and/or enquiries about the theme of Outcome and Impact of FRP4Hs on Households, please do not hesitate to contact CENFACS.

• • Final Words about FRP4Hs for Households

Financial Resilience Programme for Households is about improving the financial ability and capability to recover from income or expense shocks as explained by Salignac et al (18), or enhancing the ability in coping with financial shock or recovering from financial difficulties as argued by McKnight and Rucci (op.cit.).

It is further about working together with liquidity-constrained households through an arsenal of financial tools or weaponry they need so that they can stay resilient or embrace financial resiliency. In doing so, it increases their financial strengths while reducing their financial weaknesses or vulnerabilities.

It is finally about reducing, avoiding and ending asset-based poverty amongst them and their future generations.

For further details about Financial Resilience Programme for Households, please contact CENFACS.

_________

• References

(1) https://chisellabs.com/glossary/what-are-metrics/ (accessed in May 2024 )

(2) https://www.digitalocean.com/community/tutorials/an-introduction-to-metrics-monitoring-and-alerting (accessed in May 2024)

(3) https://www.batimes.com/articles/creating-implementing-and-managing-effective-metrics/ (accessed in May 2024)

(4) https://mediashift.org/2017/11/telling-stories-metrics-inside-news-organisation/(accessed in May 2024)

(5) Raulo A, Rojas A, Kröger B, Laaksonen A, Orta CL, Numio S, Peltoniemi M, Lahti L, Ζliobaitè I. 2023 What are patterns of rise and decline? R. Soc. Open Sci. 10:230052. https://doi.org/10.1098/rsos.230052 (accessed in May 2024)

(6) https://www.britannica.com/topic/social-change/Patterns-of-social-change (accessed in May 2024)

(7) Pullanikkatil, D. and Shackleton, CM. (2019), Poverty Reduction Through Non-Timber Forest Products: Personal Stories, Sustainable Development Goals Stories, Springer at https://doi.org/10.1007/978-3-319-75580-9 (Accessed in May 2023)

(8) Feder, S., (2020), The Power of Stories: Poverty Reduction Through NTFPs at https://medforest.net/2020/02/26/that-power-of-stories-poverty-reduction=through-ntfps/ (Accessed in May 2023)

(9) Wood, A. and Barnes, J., (2007), Making Poverty the Story: Time to Involve the Media in Poverty at https://gsdrc.org/document-library/making-poverty-the-story-time-to-involve-the-media-in-poverty-reduction/# (Accessed in May 2023)

(10) https://www.betterevaluation.org/methods-approaches/themes/impact-evaluation (Accessed in May 2023)

(11) https://documents1.worldbank.org/curated/en/400251468187810398/pdf/99662-REVISED-WB-Green-Bond-Box393208B-PUBLIC.pdf (accessed in May 2024)

(12) https://www.weforum.org/agenda/2023/11/what-are-green-bonds-climate-change/ (accessed in May 2024)

(13) https://poverty.ucdavis.edu/sites/main/files/file-attachments/policy_brief_stevens_poverty_transitions_1.pdf (accessed in April 2024)

(14) Cupitt, S. & Ellis, J. (2003), Your project and its outcomes, Charities Evaluation Services, Community Fund 2003

(15) https://www.impactio.com/blog/defining-the-difference-between-impact-and-outcome (accessed in May 2024)

(16) https://www.cipfa.org/services/financial-resilience-index-2022 (accessed in May 2024)

(17) McKnight, A. & Rucci, M. (2020). The Financial resilience of households: 22 country study with new estimates, breakdowns by household characteristics and a review of policy options. CASE/219, Centre for Analysis of Social Exclusion, London School of Economics and Political Science, May http://sticerd.lse.ac.uk/case (accessed in May 2024)

(18)Salignac, F.; Marjolin, A.; Reeve, R.: Muir, K. (2019). Conceptualising and measuring financial resilience: A multidimensional framework. Social Indicators Research 2019, 145, 17-38 (accessed in May 2024)

_________

• Help CENFACS Keep the Poverty Relief Work Going this Year

We do our work on a very small budget and on a voluntary basis. Making a donation will show us you value our work and support CENFACS’ work, which is currently offered as a free service.

One could also consider a recurring donation to CENFACS in the future.

Additionally, we would like to inform you that planned gifting is always an option for giving at CENFACS. Likewise, CENFACS accepts matching gifts from companies running a gift-matching programme.

Donate to support CENFACS!

FOR ONLY £1, YOU CAN SUPPORT CENFACS AND CENFACS’ NOBLE AND BEAUTIFUL CAUSES OF POVERTY REDUCTION.

JUST GO TO: Support Causes – (cenfacs.org.uk)

Thank you for visiting CENFACS website and reading this post.

Thank you as well to those who made or make comments about our weekly posts.

We look forward to receiving your regular visits and continuing support throughout 2024 and beyond.

With many thanks.