Welcome to CENFACS’ Online Diary!

05 April 2023

Post No. 294

The Week’s Contents

• Protection in the Context of Falling Real Household Disposable Income

• Taking Climate Protection and Stake for African Children at the Implementation (TCPSACI) with Installation Sub-phase (Phase 3.2) and the High Seas Treaty

• Activity/Task 4 of the ‘i‘ Project: Influence Protection

…And much more!

Key Messages

• Protection in the Context of Falling Real Household Disposable Income

This month, our protection work will focus on ways of finding and or enhancing the means, tools and policies to protect incomes and income poor households. Many of income poor households have problem to meet their living expenses. They live at or below the extreme poverty line of $2.15 person per day (based on 2017 purchasing power parities) and or do not simply have earned income to be independent. Adding to their lack of or very limited level of income, there has been a succession of crises (like climate crisis, the coronavirus disaster and the cost-of-living crisis) with cumulative adverse effects. These crises together with their negative effects have made their income situation even worse in living memory. It has been catastrophic for those who do have not solvable income to survive or those living at/below the extreme poverty line or those who always have income problem. The majority of them have their purchasing power falling while the prices and bills for life-sustaining services and goods keep on climbing.

In this painful context of soaring prices and bills, there is a pressing and urgent need to protect falling real household disposable income. Protecting falling real household disposable income is about taking actions to stop incomes falling. This could mean either the income poor households do it by themselves (via self-protection) or someone else do it for them or even they partly do it and others partly do it for them. These are the possible options for them.

The income protection options that we will be working on during this Month of Protection within CENFACS are the most commonly known about income protection for the poor households. However, we shall not stop at these conventional options. Throughout the month of April 2023, we are going to try to go beyond these generic or classic recipes of income protection to explore new and innovative ways of approaching income protection for the poor; ways that reflect the kinds of context or circumstances we have today and will be having tomorrow. Today, we are in the context of skyrocketing prices and bills at a rate and pace that no income poor household can match or follow. Tomorrow, there could be different types of challenges or crises with damaging effects on poor household income.

Both the generic or classical solutions to falling incomes and new approaches are highlighted in our April 2023 action plan to work with the income poor households to protect their falling purchasing power. To find more about this action plan and what is likely to be the Month of Protection within CENFACS, please read under the Main Development section of this post.

• Taking Climate Protection and Stake for African Children at the Implementation (TCPSACI) with Installation Sub-phase (Phase 3.2) and the High Seas Treaty

Last month, we started the planning process of the 2023 Climate Talks Follow-up. We informed you that the slogan for this 2023 follow-up would be: Dubai Raise Children’s Ambitions and Hopes.

Consisted of the 2023 Climate Talks Follow-up is our plan to engage with the 28th session of the Conference of the Parties (COP28) to the United Nations Framework Convention on Climate Change (1), which will be convened in Dubai (United Arab Emirates) from 30 November to 12 December 2023. This engagement or follow up will contribute to TCPSACI.

We hope that the coming Dubai climate gathering will raise climate ambitions and hopes for children. Let us also expect that the voices of youth and future generations will resonate during COP28 as they were included in COP27, and youth-led solutions to climate change will find accommodation in COP28.

Besides the planning process of the 2023 Climate Talks Follow-up, we are reflecting on the High Seas Treaty.

• • What is the High Seas Treaty?

Last month, the United Nations (2) reached an historic agreement on protecting marine biodiversity in international waters. This agreement on Marine Biodiversity of Areas Beyond National Jurisdiction (also known as BBNJ or the High Seas Treaty for others) is about ensuring the protection and sustainable use of marine biodiversity of areas of beyond national jurisdiction. It is the ocean-related goals and targets linked to the 2030 Agenda for Sustainable Development. We are working on the contents of this agreement or treaty.

• • TCPSACI and the High Seas Treaty

We are working on how the stoppage of the destructive trends facing ocean health can enhance climate protection and stake for children and generations to come. In other words, we are looking at how a healthier, resilient and productive ocean can benefit the current and future generations since the ocean provides water, food, oxygen and climate regulation.

For those who are interested in this piece of work or are doing similar work and would like to talk to us about it, they are welcome to contact CENFACS.

For those who have any queries about the 2023 Climate Talks Follow-up and the Phase 3.2, they are free to get in touch with CENFACS.

To find out more about CENFACS’ Compendia of CENFACS’ Climate Advocacy, please also communicate with CENFACS.

• Activity/Task 4 of the ‘i‘ Project: Influence Protection

This month’s activity or task for the ‘i‘ project is to positively influence protection of the poor, the victims of war and natural disasters as well as the victims of other risks, shocks and crises.

• • What is positively influencing protection about?

It is about maximising the power that persons or factors have to affect target audiences (e.g., those looking for shelter, refuge, cover, safety, care, food, health, etc.) shielding from danger (like homelessness, hunger, insecurity, violence, natural calamity, health disaster, etc.). This can be in local community matter and/or overseas humanitarian aid situation where the protection of the vulnerable, unprotected and events-stricken people and communities is highly regarded and demanded.

• • What one can do to create and or enhance protection of the poor

To create and or enhance protection of the poor, one needs to understand the contextual situation of those who need protection, identify the problems they are facing, find out who have the power to achieve change and explore the way of achieving change.

In this task, it is better to use evidence-based materials to positively influence those who have the power to protect the poor. One can also use a simple and persuasive story and engage those who hold the key to the lack of or less protection of the poor, those who are in the position to do something about poverty. One can use their experience to the real world policy influencing techniques or methods, conduct evidence-informed policy change, and utilise their alliances and networks so that those in need of protection can have it and navigate their way out of poverty linked to the lack of or less protection.

For those members of our community who would like to positively influence protection with us, and who would like to talk to us beforehand; they should not hesitate to contact us.

To contact CENFACS, please use the details provided on the contact-us page of this site.

Extra Messages

• Shop at CENFACS’ Zero Waste e-Store during Easter Giving Season

• All-year Round Projects Cycle (Triple Value Initiatives Cycle) – Step/Workshop 7: Implementing your Play, Run and Vote Projects

• CENFACS’ be.Africa Forum Discusses Protection for Women and Children in Africa

• Shop at CENFACS’ Zero Waste e-Store during Easter Giving Season

CENFACS e-Store is opened for your Easter goods donations and goods purchases.

At this time, many people have been affected by the cost of living crisis mostly driven by the hikes in prices of basic life-sustaining needs (e.g., energy, food, transport, housing, council tax, phone, etc.).

The impacted of the cost of living crisis needs help and support as prices and bills have astronomically gone up while real incomes are less for many of those living in poverty.

Every season or every month is an opportunity to do something against poverty and hardships. This April too is a good and great month of the year to do it.

You can donate or recycle your unwanted and unneeded goods to CENFACS’ Charity e-Store, the zero waste shop built to help relieve poverty and hardships.

You can as well buy second hand goods and bargain priced new items and much more.

CENFACS’ Charity e-Store needs your support for SHOPPING and GOODS DONATIONS.

You can do something different this Season of Goods Donations by SHOPPING or DONATING GOODS at CENFACS Charity e-Store.

You can DONATE or SHOP or do both:

√ DONATE unwanted Easter GOODS, GIFTS and PRODUCTS to CENFACS Charity e-Store this April and Spring.

√ SHOP at CENFACS Charity e-Store to support good and deserving causes of poverty relief this April and Spring.

Your SHOPPING and or GOODS DONATIONS will help to the Upkeep of the Nature and to reduce poverty and hardships brought by the cost of living crisis.

This is what the Season of Giving is all about.

Please do not hesitate to donate goods or purchase what is available at CENFACS e-Store.

Many lives have been threatened and destroyed by the cost of living crisis.

We need help to help them come out poverty and hardships caused by the cost of living crisis.

To donate or purchase goods, please go to: http://cenfacs.org.uk/shop/

• All-year Round Projects Cycle (Triple Value Initiatives Cycle) –

Step/Workshop 7: Implementing your Play, Run and Vote Projects

After making the organisational structure of your chosen Play, Run and Vote Projects, it is now the time to proceed with the Implementation Step.

• • What is an Implementation Step?

There are many definitions within the literature about project implementation. One of them comes from ‘taskmanagementguide.com’ (3) which states that

“Project implementation is a practice of executing or carrying out a project under a certain plan in order to complete this project and produce desired results”.

The above definition indicates that one needs an implementation plan. As an all-year-round project implementor, you can draw up your implementation plan that shows the way you would like to execute and carry out your project.

Having said that Project Implementation is the step you put your project plan into action. You want your all-year-round project to fulfil and accomplish the goals and objectives you have set up for it. It is also the phase during which you can register, review and approve/reject any changes and variations. As an all-year-round project manager of your project, you need to coordinate all project aspects and resources to meet the objectives of the project plan. One of the aspects of the project implementation is change control.

• • What is Change Control in a Project implementation Process?

Drawing from what ‘ecampusontario.pressbooks.pub’ (4) states,

“It is a set of procedures that lets you make changes in an organised way”.

The same ‘ecampusontario.pressbooks.pub’ explains this:

“If you find a problem,… you will need to look at how it affects the triple constraint (time, cost, scope) and how it impacts the project quality… If you evaluate the impact of the change and find it won’t have an impact on the project triple constraint, then you can make the change without going through change control”.

• • An Example of Implementing your All-year Round Projects

Let us take the example of Voting your 2023 International Development and Poverty Reduction Manager.

Your goal is to find a person who will meet the managerial qualities of such a position. Amongst the objectives are the design of a job description and person specification that match with the profile of your ideal International Development and Poverty Reduction Manager of the Year.

In project implementation jargon, you will put approved plan into practice to proceed with the selection of your International Development and Poverty Reduction Manager of the Year. He/she must meet your selection criteria. If you are voting as a group, you could set up a selection panel or recruitment board like you will do it for real job interview. You can start by shortlisting 12 candidates, cutting down your list to 6, then to 3 until you reach/vote the last one, who has scored the best and most results of your jury questions and responded to most criteria.

For those who would like to dive deeper into Implementing their Play or Run or Vote project, they should not hesitate to contact CENFACS.

• CENFACS’ be.Africa Forum Discusses Protection of and for Women and Children in Africa

How to avoid overlapping crises lead to the reversal of the hard-won gains made on protection and development for women and children in Africa

The first debate of the Month of Protection within CENFACS’ be.Africa Forum of Ideas and Actions will be about finding sustainable paths to preserve the hard-won gains on the road of protection of and for women and children in Africa. Indeed, the overlapping crises (like the coronavirus pandemic, climate change, Russia-Ukraine conflict, the cost-of-living crisis, civil insecurity, etc.) have led to multiple adverse consequences across Africa.

Amongst the ripple effects are declining revenue for many States, rising debts, tightening of fiscal manoeuvre, worsening terms of trade, erosion of decades of development gains, increased poverty and economic hardships, in brief looming economic crisis. These crises and damaging consequences are threatening, if not destroying, many of established lives and the hard-won achievements made such as poverty reduction, protection of women and children and so on. They have reverberated in every aspect of life and resulted in increased inequalities and vulnerabilities in Africa. As we all know quite often women and children are the ones who often bear the brunt of these types of crises and damaging consequences.

There could be ways of stopping or avoiding that crises hamper the hard-won gains made on protection of and for women and children in Africa. In the first discussion of the CENFACS’ be.Africa Forum of Ideas and Actions, we shall carry out the following:

a) Explore ways of protecting and consolidating the achievements made in terms of protection of and for women and children in Africa

b) Think of ways of keeping protection for African women and children resilient and ring-fencing in face of the threats and risks from congruent effects of overlapping shocks that Africa is going through right now

c) Investigate the best way of growing protection beyond and despite the damaging consequences of these current overlapping and future shocks.

Those who may be interested in this discussion can join in and or contribute by contacting CENFACS’ be.Africa, which is a forum for discussion on matters of poverty reduction and sustainable development in Africa and which acts on behalf of its members in making proposals or ideas for actions for a better Africa.

To engage with the CENFACS‘ be.Africa Forum of Ideas and Actions and share what they know and think about protection of and for women and children in Africa in challenging times like now, please contact us by using our usual contact details on this website.

Message in French (Message en français)

• Magasinez à la boutique en ligne Zéro déchet du CENFACS pendant la saison des dons de Pâques

La boutique en ligne du CENFACS est ouverte pour vos dons de produits de Pâques et vos achats de biens.

À l’heure actuelle, de nombreuses personnes ont été touchées par la crise du coût de la vie, principalement en raison de la hausse des prix des produits de première nécessité (énergie, nourriture, transport, logement, taxe d’habitation, téléphone, etc.).

Les impacté(e)s de la crise du coût de la vie ont besoin d’aide et de soutien, car les prix et les factures ont augmenté de façon astronomique alors que les revenus réels sont moindres pour beaucoup de ceux ou celles qui vivent dans la pauvreté.

Chaque saison ou chaque mois est l’occasion de faire quelque chose contre la pauvreté et les difficultés. Ce mois d’avril aussi est un bon et excellent mois de l’année pour le faire.

Vous pouvez faire don ou recycler vos biens non désirés et inutiles à la boutique en ligne caritative du CENFACS, la boutique zéro déchet conçue pour aider à soulager la pauvreté et les difficultés.

Vous pouvez également acheter des biens d’occasion et des articles neufs à prix avantageux et bien plus encore.

La boutique en ligne caritative du CENFACS a besoin de votre soutien pour les ACHATS et les DONS MARCHANDISES.

Vous pouvez faire quelque chose de différent cette saison des dons de biens en MAGASINANT ou en DONNANT DES BIENS à la boutique en ligne de charité CENFACS.

Vous pouvez FAIRE UN DON ou ACHETER ou faire les deux:

√ DONNEZ des BIENS, CADEAUX et PRODUITS de Pâques indésirables à la boutique en ligne de la Charité CENFACS en avril et au printemps;

√ ACHETEZ à la boutique en ligne de charité CENFACS pour soutenir les bonnes et méritantes causes de lutte contre la pauvreté en avril et au printemps.

Vos ACHATS et/ou DONS DE BIENS aideront à l’entretien de la nature et à réduire la pauvreté et les difficultés causées par la crise du coût de la vie.

C’est ce qu’est la saison du don.

N’hésitez pas à faire un don ou à acheter ce qui est disponible sur la boutique en ligne du CENFACS.

De nombreuses vies ont été menacées et détruites par la crise du coût de la vie.

Nous avons besoin d’aide pour les aider à sortir de la pauvreté et des difficultés causées par la crise du coût de la vie.

Pour faire un don ou acheter des biens, veuillez vous rendre à : http://cenfacs.org.uk/shop/

Main Development

• Protection in the Context of Falling Real Household Disposable Income

The following items will help to approach Protection in the Context of Falling Real Household Disposable Income:

σ Basic Understanding of Real Household Disposable Income

σ Falls in Real Household Disposable Incomes

σ Income Protection

σ Identified Areas of Protection Work and Households to Work with in this April 2023

σ Action Plan for the Implementation of Protection this April 2023

σ Week Beginning Monday 03/04/2023: Income Protection through Savings

σ Other Areas of Protection: e.g., Protection of Flora and Fauna.

Let us briefly explain each of the above items making Protection in the Context of Falling Real Household Disposable Income.

• • Basic Understanding of Real Household Disposable Income

Disposable income is defined by Christopher Pass et al. (5) as

“The amount of income which a person has available after paying INCOME TAX, NATIONAL INSURANCE CONTRIBUTIONS and PENSION contributions” (p. 181)

However, disposable income needs adjustment for inflation. After being adjusted for inflation, disposable income becomes real. The website ‘tutor2u.net’ (6) explains that

“Real disposable income is the post tax and benefit income available to households after an adjustment has been made for price changes”.

In other words, changes in prices of goods and services can lead to the increase or fall in real household disposable incomes. In the context of this post, we are dealing with fall in real household disposable incomes.

• • Falls in real household disposable incomes

In recent years, prices and bills keep on rising while real household disposable incomes have failed to match this rising trend. That is to say, incomes are not fully index-linked to keep pace with inflation.

To highlight this fall, the website ‘finder.com’ (7) has revealed that

“The average British adult has £866 in disposable income a month in 2022, which is a reduction of £23 a month from 2020 (£889). Total monthly living costs on average have reached £1,125 with the average rent price being £437 and the average essential spending costs at £688 a month”.

Likewise, the Resolution Foundation (8) found that

“2022 was a year of double-digit inflation that drove a 3.3 per cent – or £800 per household – hit to real disposable incomes, the biggest annual fall in Century”.

The same Resolution Foundation forecasted that

“Household income falls in 2023 will be 3.8 per cent or £880 per household as big as those seen in 2022”.

As a result, living standards are unchanged or getting worse.

According to the Office for National Statistics (9),

“Median household disposable income in the UK was £32, 300 in the financial year ending (FYE) 2022, a decrease of 0.6% from FYE 2021, based on estimates from the Office for Natural Statistics Household Finances Survey… Median disposable income for the poorest fifth of the population decreased by 3.8% to £14,500 in FYE 2022; reductions were also observed in main original income and cash benefits”.

Also, the Office for National Statistics (10) argues that

“The Consumer Prices Index including owner occupiers’ housing costs (CPIH) rose by 9.2% in the 12 months to February 2023, up from 8.8% in January”. This CPIH figure was released on 22 March. The next release will be on 19 April 2023. Yet, the consumer price inflation in the UK was 6.2% in March 2022.

Similarly, the figure released on 22 March 2023 by the Bank of England (11) for the current bank rate was 4.25%, whereas the bank rate was 0.75% in March 2022.

Moreover, The Food Foundation (12) states that

“The percentage of households with children who are experiencing food insecurity was 25.8% in September 2022”.

This percentage of households with food insecure children could be another way of perceiving the fall in real household disposable income.

In meantime, bills like council tax, rent, telephone, transport, etc. have also risen. Although the energy price is capped at £2,500 on the average household energy bill, we are still waiting for the next policy announcement by the UK’s independent energy regulator, Ofgem, on 26 May 2023.

So, real disposable incomes for poor households have not risen to match the raising trends from bills and prices. This is despite income support has been given to those who are eligible. This mismatch between their real incomes and rising prices and bills can only lead to falling real household disposable incomes.

Falling real household disposable incomes can cause serious harms to households, especially to the poorest. This is why protection is needed to protect their incomes.

• • Income Protection

The kind of protection we are talking about is of income. What is income protection? Income protection can be viewed from many perspectives (economic, climate finance, governmental, insurance, etc.). Many of the definitions within the literature have a common ground as they take the insurance view of income protection. Amongst these definitions is the one provided by ‘which.co.uk’ (13) which states that

“Formerly known as permanent health insurance, income protection is an insurance policy that pays out if you’re unable to work because of injury or illness. It is there to help you pay your household bills, mortgage payments, credit card and everyday costs that you can no longer cover”.

However, for income protection to be relevant it has to be index-linked. Index-linked income protection is the one you add an index-link to the income protection. In other words, income protection rises with a measure of inflation (such as the consumer prices index or the retail prices index), each year. Adding an inflationary index-link will obviously increase the premium each year.

Yet, the kinds of households we are dealing with may or may not be able to buy income protection insurance since they cannot afford it. If so, then what is income protection for them? How can we innovate in terms of income protection for the poor households? Can income protection be conceived outside the framework of insurance policy? The answers to these three questions will be provided as we move along our protection notes of the month.

• • Identified Areas of Protection Work and People to Work with in this April 2023

Following some basic research relating to income protection for the poor households, we have identified the following areas and households to work with.

• • • Identified areas of protection work

We have identified four areas of work on income protection which are as follows:

a) Income protection from savings made by households

b) Income protection from statutory bodies like the Government

c) Income protection provided by employers or employer-sponsored income protection plan

d) Income protection sold by insurance companies or organisations.

In the plan for the implementation of protection this April 2023, we will consider the above-stated areas of protection.

• • • Households to work with for April 2023 Protection

We will be working with the following households needing support to protect their real disposable income:

√ Households unable to purchase income protection insurance

√ Those having savings but without income protection policy

√ Those looking for support to improve their income protection policy

√ Those grappling with a reduced income and struggling with bills and prices

√ Those who need income protection to deal with the cost-of-living crisis

√ The severely impacted by inflation (both imported and domestic inflation)

√ Those with less or low real disposable income

√ Those having less flexibility in their household protection budget

√ The income poor households

√ Those extreme poor households or living at or below the extreme poverty line

√ The food and energy poor households

√ Households incapacitated by multi-crises

√ The other poor and vulnerable households

Etc.

Many of these households we have listed could fall under these categories:

~ those looking for a cover on sick pay

~ those searching for savings to protect themselves

~ those surviving on government benefit or support

~ those supported by families or relatives.

To better work with them, an action plan is needed.

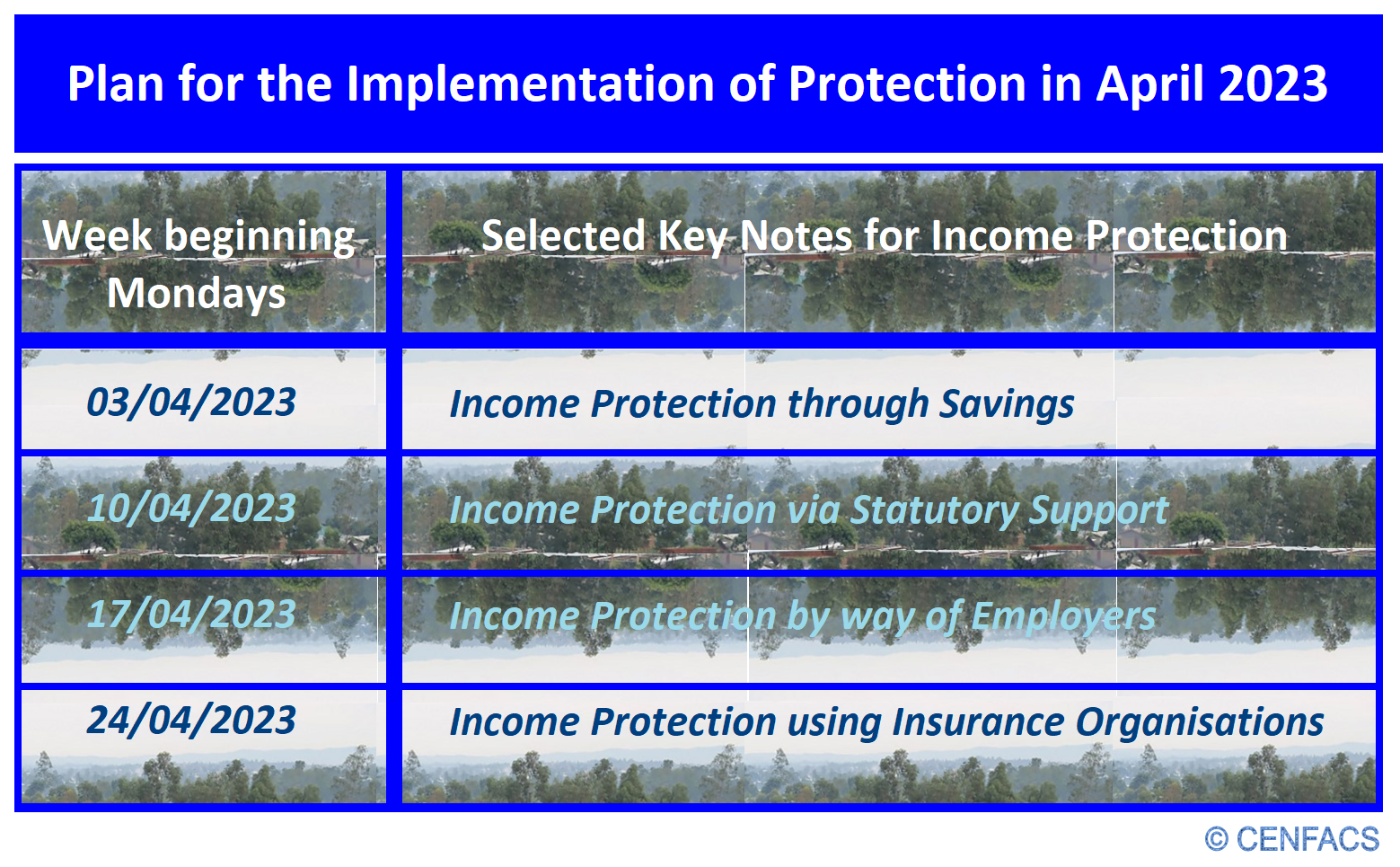

• • Action Plan for the Implementation of Protection this April 2023

To implement protection this April 2023, we have selected four key notes, which are given in the table below.

These notes will be developed starting every Mondays of April 2023 as scheduled above.

Also, this plan of protection needs to be combined with the Preview of Projects and Programmes for Spring Relief 2023 (which we released on the 15th of March 2023 in our Post No. 291).

Besides these selected notes and areas of protection, we would like to keep on working on other areas that need particular attention too, like protection of flora and fauna.

Before summarising these other areas of protection, let us look at the first selected key note of our plan, which is Income Protection through Savings.

• • Week Beginning Monday 03/04/2023: Income Protection through Savings

Households can use their savings (or a portion of their income that is not used for consumption or paying taxes) to protect them from any unexpected expenses, loss of job, sickness, retirement, etc. In order to do that they need to create a savings plan that can match their protection plan.

• • • Savings plan

The website ‘bitpanda.com’ (14) explains that

“A savings plan is useful if you want to establish an emergency fund for unforeseen expenses… It involves putting aside a portion of your income over a fixed period of time in order to reach a specific financial goal”.

To set up savings safety net by building an emergency fund, the theory on the matter states that your emergency fund needs to be equivalent to at least three months’ salary or essential outgoings available in an instant-access savings account.

You can use high-yield-savings account or money market account or savings bond or a certificate of deposit to create your savings. The practice suggests to save money using easy-access accounts or fixed-term savings account.

However, setting money aside as savings or sinking funds on a regular basis could be harder even impossible for extremely poor households. In other words, they cannot afford to buy savings plan. But, having a financial plan or saving can help in the wake of an emergency or unpredictable time. Likewise, having a protection plan could be life-saving.

Although it could be difficult or impossible for poor households to save money to take out income protection plan, there could be ways of working with them in order to explore ways of supporting them in case of emergency or unpredictability.

• • Ways in which CENFACS Can Work with the Community regarding Savings and Income Protection

There is a number of ways in which CENFACS can work with the community to boost their income protection to deal with the bad times. These ways of working together include the following ones:

√ Setting up a basic protection plan

√ Building a simple realistic savings plan

√ Getting informed about the current and near-future opportunities to save money

√ Providing them with leads to savings for the poor

√ Advising them on the best possible options to create savings or to move in the direction of savings road

√ Explaining them the savings products and tools offered on the market (like high-yield-savings account, money market account, savings bond or certificate of deposit offered by some financial institutions and banks)

√ Recommending them digital solutions to their savings problems (e.g. online saving plan calculator)

√ Working with them to restructure their accounts to create financial space for savings

√ Adding an inflationary index-link to their income protection plan

√ Helping them to read and understand savings and financial information

√ Advising them on how to react and prepare from financial news, warnings, notices and alert messages about savings and income protection

√ Developing the basic financial skills to interpret the impact of economic indicators (like inflation, interest rate, exchange rate, etc.) on savings

√ Building their financial literacy statistics and numeracy skills to enable them to read financial information pages about savings (e.g. charts, tables, in brief infographics about savings)

√ Organising activities or workshops to help them integrate savings habit in the handling of their household financial affairs and plans

√ Improving their knowledge in terms of the key financial dates to save in the calendar about key policy announcements (for example, the release date of budgets by the Government and how these budgets can impact their savings plans)

√ Motivating them to follow news and information about savings and income protection

√ Asking them to subscribe to free providers of savings and income protection information that touches their life (e.g. free subscription to magazines, papers and websites that provide information about savings and income protection for poor households)

Etc.

All these ways of working with the community will help to protect them and their income. This is because the more informed they are, the more they will find the tools, tips and hints they need in order to create savings or to be on the road to create savings. It is all about working with them to improve the way they can create and manage their income and life in order to overcome future emergencies and unpredictability.

• • Other Areas of Protection

There are many areas that will be highlighted and on which we will be working. One of them is protection of flora and fauna.

• • • Protection of flora and fauna

This month, we shall as well revisit progress made so far in protecting animals and plants. We shall do it by recalling our Build Forward Better Flora and Fauna Projects, which were one of our last XI Starting Campaign and Projects for Autumn.

Indeed, we continue to advocate for the protection of animals (fauna) in Africa and elsewhere in developing world whereby animals get killed, traded and extinct to such extent that some species are at the brink of disappearing.

We are as well extending our advocacy to other species in danger like trees, plans and flowers (flora). It is about building forward these species that are threatened with extinction.

To advocate and raise your voice to protect and build forward better endangered plant and animal species, contact CENFACS.

For any further details about CENFACS’ Month of Protection, please do not hesitate to contact CENFACS.

_________

• References

(1) https://www.cop28.com/en/ (Accessed in February 2023)

(2) https://news.un.org/en/story/2023/1134157 (Accessed in April 2023)

(3) www.taskmanagementguide.com/glossary/what-is-project-implementation.php (Accessed in April 2023)

(4) https://ecampusontario.pressbooks.pub/projectmanagement/chapter/chapter-17-project-implementation-overview-project-management/ (Accessed in April 2023)

(5) Pass, C., Lowes, B., Pendleton, A. & Chadwick, L. (1991), Collins Dictionary of Business, HarperCollinsPublishers, Glasgow

(6) https://www.tutor2u.net/economics/blog/s-macro-key-term-real-disposable-income (Accessed in March 2023)

(7) https://www.finder.com/uk/disposable-income-around-the-uk# (Accessed in March 2023

(8) https://www.resolutionfoundation.org/publications/new-years-outlook-2023/ (Accessed in March 2023)

(9) https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/bulletins/householddisposableincomeandinequality/financialyearending2022/previous/v1 (Accessed in April 2023)

(10) https://www.ons.gov.uk/economy/inflationandpriceindices (Accessed in March 2023)

(11) https://www.bankofengland.co.uk/monetary-policy-summary-and-minutes/2023/march-2023?trk=public-post-comment-text (Accessed in April 2023)

(12) https://www.foodfoundation.org.uk/publications/new-data-show-4-million-children-households-affected-food-insecurity (Accessed in April 2023)

(13) https://www.which.co.uk/money/insurance/life-insurance-and-protection/income-protection-explained-asH217E3fIZQ# (Accessed in April 2023)

(14) https://www.bitpanda.com/academy/en/lessons/what-it-a-savings-plan/ (Accessed in April 2023)

_________

• Help CENFACS keep the Poverty Relief work going this year

We do our work on a very small budget and on a voluntary basis. Making a donation will show us you value our work and support CENFACS’ work, which is currently offered as a free service.

One could also consider a recurring donation to CENFACS in the future.

Additionally, we would like to inform you that planned gifting is always an option for giving at CENFACS. Likewise, CENFACS accepts matching gifts from companies running a gift-matching programme.

Donate to support CENFACS!

FOR ONLY £1, YOU CAN SUPPORT CENFACS AND CENFACS’ NOBLE CAUSES OF POVERTY REDUCTION.

JUST GO TO: Support Causes – (cenfacs.org.uk)

Thank you for visiting CENFACS website and reading this post.

Thank you as well to those who made or make comments about our weekly posts.

We look forward to receiving your regular visits and continuing support throughout 2023 and beyond.

With many thanks.