Welcome to CENFACS’ Online Diary!

10 February 2021

Post No. 182

The Week’s Contents

• Making Financial Risk Protection in Health Work for the Poor in the Era of COVID-19 and Lockdowns

• Pushed into Extreme Poverty by Out-of-pocket Health Spending: Share Your Experience

• Triple-value-initiative Start up

… and much more!

![]()

Key Messages

• In focus for week beginning 08/02/2021 of the month of sustainable development is:

Making Financial Risk Protection in Health Work for the Poor in the Era of COVID-19 and Lockdowns

Our work on the constituents of Target 8 of Goal 3 of the United Nations Sustainable Development Goals continues with Financial Risk Protection in Health (FRPH). We are looking at how to make financial risk protection in health work for the poor in the era of COVID-19 lockdowns. To make financial risk protection in health work for the poor, health protection needs to be built on some features like the following: needs-based solutions, valuable reliable universal health coverage, affordable, accessible by all, sustainable and able to lead to a good health and well-being.

Yet, in developing countries (like those of Africa) many peoples do not have health insurance cover. This lack of health insurance cover is coupled by the lack of universal health cover (UHC) like the UHC that exists in many industrial developed countries. Often, poor people are forced to pay from their own pockets for their health costs while making national insurance contribution which they do not often see the benefit.

In face of this situation, there are players in the market which try to do something to support those who are deprived from financial risk protection in health. Amongst these players are Africa-based Sister Organisations specialised in health matter which are trying to work with their users to make FRPH work for them. Their work is about how to reduce and possibly end poverty linked to the lack of health insurance cover or financial risk protection in health.

Under the Main Development section of this post, you will find more details about this first key message.

• Pushed into Extreme Poverty by Out-of-pocket Health Spending: Share Your Experience

As part of the work on financial risk protection in health, we would like to know if anyone of our community members has been pushed into extreme poverty because of out-of-pocket COVID-19-induced health spending. It is known that the way in which out-of-pocket money is spending on health can impact on poverty for low income people or households. In relation to that, the World Health Organisation (1) argues the following:

“Out-of-pocket health spending can force people to choose between spending on health and spending on other necessities” (p. 3)

“Out-of-pocket health spending can also push people into poverty” (p. 4)

“Out-of-pocket health spending is also a major driver of economic disadvantage compared with other factors” (p. 4)

Following these arguments, we are looking into the fact whether or not the coronavirus pandemic has similar effects for those in need who are spending their out-of-pocket money to meet the COVID-19 health bill.

Indeed, the coronavirus pandemic and subsequent lockdowns have pushed many people and families to the edge of or into extreme poverty. They have added health and personal hygiene costs (such as the costs of buying personal protective equipment, sanitation and disinfection products as well as those of cleaning) to their normal expenses budget. In doing so, these events have perhaps created new poor and or are holding the existing poor still poor.

If you have been pushed into extreme poverty by out-of-pocket COVID-19 induced health spending, we would like to hear your experience. To share your experience, just contact CENFACS.

• Triple-value-initiative Start-up/Planning

In order to support those who have decided or may decide to engage with All-year Round Projects or Triple Value Initiatives, we are running start up sessions for each of them (i.e. Run, Play and Vote projects). We are going to deal with different phases of project planning or start up from the idea (of running or playing or voting) to the initiative implementation, monitoring and evaluation.

Whether you want to run or play or vote; you need to do a basic project planning in terms of the way you want to do it. This basic project planning/start-up will include things like the following:

Aims (changes you plan to achieve), impact (a longer-term effects of your project), inputs (resources you put into your initiative), monitoring (regularly and systematically collecting and recording information), outcomes (changes and effects that may happen from your initiative), indicators (measures that show you have achieved your planned outcomes), budget (income and expenses for your initiative), etc.

As we all know, not everybody can understand these different steps they need to navigate in order to make their initiative or project a success story. That is why we are offering this opportunity to those who would like to engage with the Triple Value Initiatives (Run, Play and Vote projects) to first talk to CENFACS so that we can together soften some of the hurdles they may encounter in their preparation and delivery.

For those who would like to discuss with CENFACS their Triple-value-initiative plans or proposals, they are welcome to contact CENFACS.

Extra Messages

• Zero Income Deficit Campaign

In Focus: Uncut or Irreducible Expenses – How to deal with them

When one is poor, almost all their expenses are basic or life-saving. It is difficult to cut them in order to maintain a zero income deficit policy. How then can they not cut expenses in order to not create an income deficit that can lead to poverty and its transmission to future generations? It is dilemma.

The dilemma is that cutting them you create poverty. Not cutting them you need to find resources to refinance them. But, how do you solve this dilemma?

So, this week we are working with income deficit families and others on how to re-purpose their expenses or spending budget so that they are able to address the uncut or irreducible expenses in order to nullify or sensibly reduce income deficit.

Need to cut or manage your income deficit in your household accounts, you can contact CENFACS.

• Essential Consumption and Sustainable Development Month

Our wintry resource on Consume to Reduce Poverty (with a focus on Essential Consumption for this year) is still relevant in the month of sustainable development. To highlight this relevancy, we are extending the tips and hints provided in this resource to explore ways of improving our consumption habits to support the month of sustainable development.

As we are in a situation of the closure of non-essential economic activities, we can seize this opportunity to check if people’s essential consumption habits during the lockdown have improved their contribution to sustainable development. In other words, it is about finding out how essential consumption is positively impacting sustainable development.

For those who have anything to argue about the impact of essential consumption on sustainable development during this period of closure of non-essential economic activities, they can let CENFACS know their arguments.

• The CENFACS Community, Financial Risk Protection in Health and COVID-19 Expenses Coverage

The theme of financial risk protection in health (FRPH) gives us the opportunity to discuss with the CENFACS Community its understanding and level of tackling this issue. This is regardless of the fact that one benefits from universal health coverage or not.

We are putting the issue of FRPH in the context of COVID-19 crisis. We are trying to examine how the community is financially meeting the daily costs to protect itself against the COVID-19.

For example, one may try to find out whether the community is using its out-of-pocket money to cover these expenses or they have some sort of risk protection plans to cover from additional expenses generated by the pandemic. Alternatively, they may or not be getting support to cover the extra health costs brought by the coronavirus pandemic.

Briefly, this is a basic research or small pilot study on how the CENFACS Community is getting on in meeting the additional health costs induced by the coronavirus pandemic.

For those who would like to support this basic community research, they can feed us with information on COVID-19 induced spending coverage.

Main Development

• Making Financial Risk Protection in Health Work for the Poor in the Era of COVID-19 and Lockdowns

The following items will help to understand how to make financial risk protection in health work for the poor in the era of COVID-19 and lockdowns:

(a) Understanding financial risk protection in health

(b) Poorer households and their health accounts and budgets

(c) Household expenditure on health as a share of household total consumption/income for poor families

(d) The impact of COVID-19 on health spending budget for poor families without financial risk protection in health

(e) Africa-based Sister Organisations and their work to help locals’ needs in financial risk protection in health

(f) Actions on health finance and insurance

(g) African Diaspora money remitters and their contribution to health insurance cover in Africa

(h) Impact monitoring of financial risk protection in health of the poor at the time of COVID-19 and lockdowns

Let us look at one by one these selected items.

(a) Understanding financial risk protection in health

Our understanding of financial risk protection or the absence of a risk of financial hardship as far as health is concerned will be based on the sustainable development goal 3 and target 8 of it. This will include the context of universal heath cover. To simplify, we are using the definition of financial risk protection as given by the World Health Organisation (WHO).

From the WHO website (op. cit.), one can read the following:

“Financial protection is at the core of universal health coverage (UHC) and one of the final coverage goals. Health financing policy directly affects financial protection. Financial protection is achieved when direct payments made to obtain health services do not expose people to financial hardship and do not threaten living standards”.

“Out-of-pocket payments for health can cause households to incur catastrophic expenditures, which in turn can push them into poverty. Key to protecting people is to ensure prepayment and pooling of resources for health, rather than relying on people paying for health services out-of-pocket at the time of use”.

After reading the perception of UHC by WHO, one may notice that it is possible for poor people to be exposed to financial hardships and their living standards be threatened in places where there is no or partial healthcare insurance cover. In time of the COVID-19 crisis, it is even more complicated for those who have never had any health insurance policy to have any basic financial help for health protection if they do not get bailed out by the public authorities. In this respect, the WHO definition also helps in understanding the role and place of a UHC system based on a sound and practical policy of prepayment and pool of resources.

(b) Poorer households and their health accounts and budgets

One of the problems with health spending is that poorer households cannot afford to pay for their own health insurance (both public and private). Yet, in many low income countries (like those of Africa), they have to spend out-of-pocket money to do so even if they have not got any money to spend. This could mean money should come from somewhere else, which could be an extended family, loan, charitable source, etc. This problem raises the debate over universal health coverage which is one of the health targets for the United Nations sustainable development goal 3 related to good health and healthy well-being.

In time of the health crisis like the coronavirus pandemic crisis, this controversy about financial risk protection relating to health is even bigger. Like everybody, poorer households have experienced an increase in the amount of items and products they need to access in order to protect themselves and the public against the strains of coronavirus. This increase has affected their health accounts and budgets as they have (like anybody else) to purchase products to protect against COVID-19.

If anyone is concerned by what we have just described or have any interest, they can discuss the matter with CENFACS.

(c) Household expenditure on health as a share of household total consumption/income for poor families

The United Nations Sustainable Development Goal 3 and Target 8 use two indicators which are: coverage of essential health services (3.8.1) and proportion of population with large household expenditures on health as a share of total household expenditure or income (3.8.2). The first indicator measures coverage of selected essential health services on a scale of 0 to 100 while the second one helps to track progress towards universal health coverage.

In its World Health Statistics 2020, the World Health Organisation (2) published the following indicators for these African countries (Benin, Burkina Faso, Burundi, Cameroon, Congo, Cote d’Ivore and the Democratic Republic of Congo) which are part of its member states.

In 2017, the service coverage index for universal health coverage in comparable estimates were 40 for Benin and Burkina Faso, 42 for Burundi, 46 for Cameroon, 39 for Congo, 47 for Cote d’Ivoire and 41 for the Democratic Republic of Congo.

Between 2010 and 2018, the percentage of population with household expenditures on health bigger than 10% of total household expenditure or income from primary data were 10.9 for Benin, 3.1 for Burkina Faso, 3.3 for Burundi, 10.8 for Cameroon, 4.6 for Congo, 12.4 for Cote d’Ivoire and 4.8 for the Democratic Republic of Congo.

Between 2010 and 2018, the percentage of population with household expenditures on health bigger than 25% of total household expenditure or income from primary data were 5.4 for Benin, 0.4 for Burkina Faso, 0.4 for Burundi, 3.0 for Cameroon, 0.7 for Congo, 3.4 for Cote d’Ivoire and 0.6 for the Democratic Republic of Congo.

The above first set of figures tell us that if one needs to make financial risk protection in health work for the poor in the above named countries in the era of COVID-19 and lockdowns, the coverage of health service needs to be improved and expanded to those who do not have it.

For the second set of figures, the incidence of catastrophic health spending has to be reduced for those who pay out of their pockets. It also means that one needs to improve the tracking or progress in universal health coverage, particularly but not specifically for poor households.

For those who would like to discuss in depth about household expenditure on health as a share of household total consumption/income for poor families, they can let CENFACS know so that we can plan an activity or a discussion group about it.

(d) The impact of COVID-19 on health spending budget for poor families without financial risk protection

We have been doing some research on the impact analysis of COVID-19 on the realisation of climate and sustainable development goals for African children. This kind of analysis can be expanded to the realisation of a particular sustainable development goal and target (like goal 3 and target 8). To be more specific, this can be done on financial risk protection in health. This is what we are trying to do when talking about the impact of COVID-19 on health spending budget for poor families without financial risk protection.

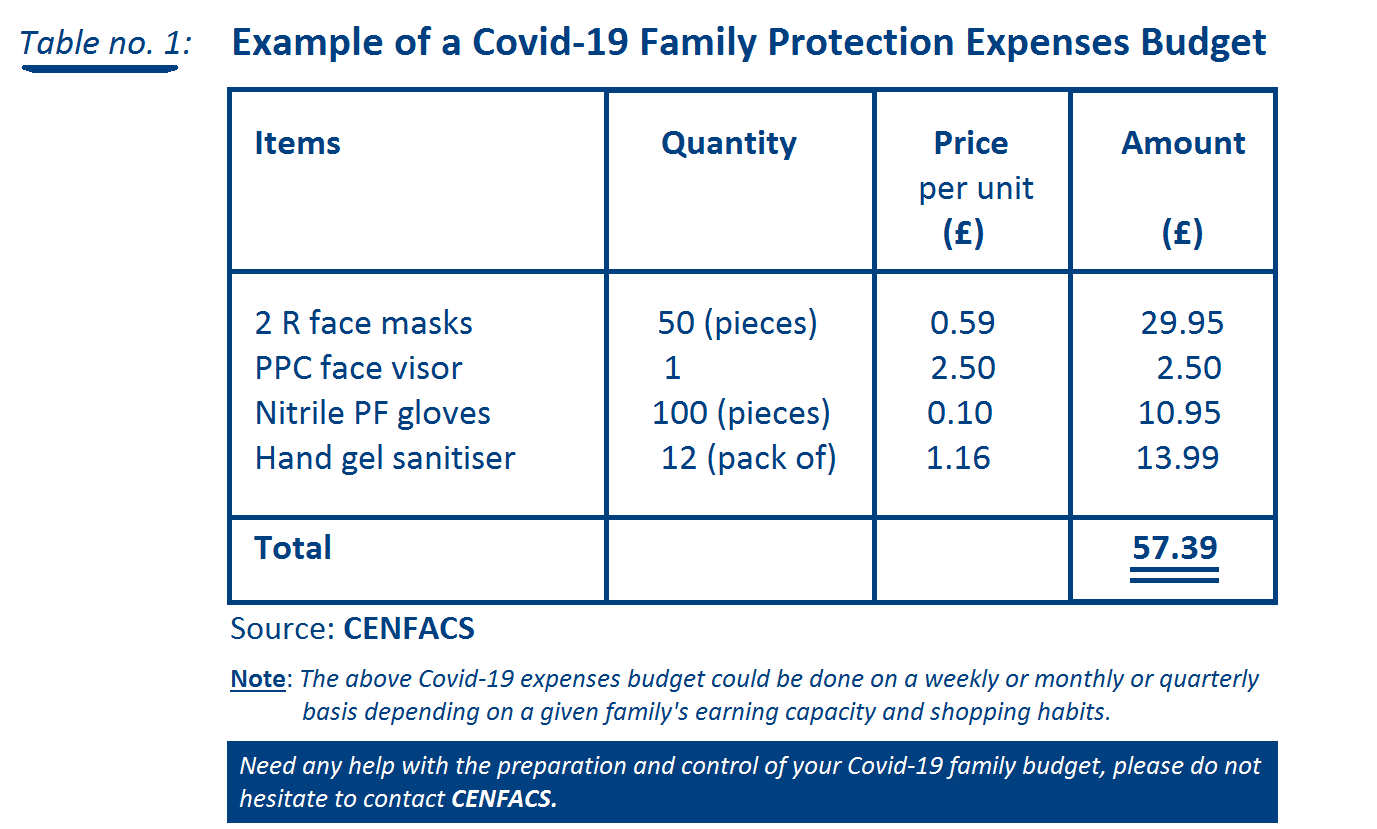

Indeed, apart from the fact that poor people can become COVID-19 patients, they have to spend like everybody else money to cover against COVID-19 strains or germs. This spending has to be included in their household budget as the example below show (Table no. 1)

The above figure (Table no. 1) gives us some indication about what could be a COVID-19 expenses budget for an average household.

In places where poor people get support to cover these additional costs to their current spending budget, they will have less trouble in living during this health crisis. However, where there is no or insufficient support, this can lead them to further poverty and hardships.

If a household has health protection policy and his policy can cover these additional costs, then there is no problem. Yet, many of these poor households cannot afford to buy insurance health protection policy to cover these types of expenses. If there are players (like a Government) who can help them to buy a policy, that is fine. If not, there could be a possibility of having further poverty in these households.

Let us take the example of the CENFACS Community. Like everybody else, many of the members of our community are suffering the impact of COVID-19 on their health spending budget, for those without financial risk protection in health. Because of COVID-19, their health spending budget has increased while their income has gone down. Many of them have lost their capacity of earnings without financial compensation as the lockdowns have detrimental effects on them like anybody else.

If anyone wants to share their experience about the impact of COVID-19 on their health spending budget or has any comment to make about their financial risk protection in health, they can share it with CENFACS.

(e) Africa-based Sister Organisations and their work to help locals’ needs in financial risk protection

There is always a debate between two ways of financing health risk protection in health which are: people’s out-of-pocket payments for health services and public health purse. This is found in both developing and developed countries.

For various reasons, financial risk protection relating to health is not organised in developing countries (like those of Africa) as it is in developed countries. Because of that, many people in developing countries (including those of Africa) are left without universal health coverage and without financial risk protection by their states. Some of these people try to get support they can or wonder when support will come to them. ASOs that work in the field of health try to make an effort to work with those locals who need some help to sort out their financial risk protection.

In the work that ASOs are doing they try to help those in need of financial risk protection in health in various ways such as:

√ Working with them to make an informed decision or decision between health spending and spending on necessities

√ Finding suitable ways of reducing or avoiding extreme poverty caused by health spending

√ Exploring with them alternative sources of financing their health spending

√ Ensuring that health spending does not induce an economic barrier

√ Advising them on how to stay healthy and maintain a good well-being

√ Working with them on how to get value for money in terms of financial risk protection schemes

Etc.

At this time of the battle against the coronavirus pandemic, the handling of financial risk protection in health becomes even more important for those in need of health risk protection. This is because there are still other services or viruses against which they may have to fight while the battle against the coronavirus continues. Likewise, lockdown and health measures to protect against COVID-19 are not making easy their work. However, one can hope that with what COVID-19 has revealed in terms of health systems in many places in Africa financial risk protection schemes will be taken seriously. The work that some ASOs are doing with very limited means will be valued and given support it deserves.

(f) Actions on health finance and insurance for ASOs

There are actions that can be undertaken to help those organisations that are involved in working with locals in financial risk protection matter. There are two levels of actions which are: actions on health insurance cover for the poor and those related to the direct support of ASOs.

f.1. Actions on health insurance cover for the poor and vulnerable

These actions revolve around the following:

√ Reduction of insurance premiums to improve affordability of health insurance for the poor and vulnerable people

√ Helping poor communities to buy health insurance policies (for example those related to COVID-19 protection) where there is no health insurance cover for them

√ Making risk insurance in health work for the poor

Etc.

f.2. Actions to support ASOs working on health risk protection

These actions may include activities undertaken that may help to mobilise finance to cover financial risk protection in health. These actions could be like the following:

√ Donations and support donor development programme

√ Financial products and services to fund health risk protection work carried out by ASOs

√ Private funds mobilisation

√ Health fundraising activities and events

√ Grant making for health insurance work

√ Income-generating activities to fund health risk protection

√ Online and digital fundraising for risk protection in health

Etc.

Although we are at the moment of health crisis with the coronavirus pandemic, one needs to think as well that after this crisis life will continue. Therefore, one needs to have a long term perspective in terms of actions to be conducted if they are going to make financial risk protection in health work for the poor.

(g) African Diaspora money remitters and their contribution to health insurance cover in Africa

It is well documented that African Diaspora’s remittances contribute to Africa’s development and the reduction of poverty. One area of contribution that Africans in the diaspora make is funding health needs of African family members in Africa who cannot afford health costs. These costs range from simple medicine like aspirin to more complicated cases of diseases.

Often, Africans in the diaspora have either to send money or purchase medicine to help those relatives and friends who are ill and do not have the means to buy a health cover policy because the way in which health systems operate in some places in Africa. Many in the CENFACS Community receive requests from families and relatives for medical and health support.

The positive responses to those demands are indeed an example of how African diaspora is contributing in making financial risk protection for those in need in Africa. This is despite the fact that the coronavirus pandemic and lockdowns have detrimental effects on this little but useful contribution Africans in the diaspora are making to health needs in Africa.

For those who want to discuss further about African diaspora’s contribution to the health and wellbeing in Africa, they can contact CENFACS.

(h) Impact monitoring of financial risk protection of the poor at the time of COVID-19 and lockdowns

In time of deep crisis like of the coronavirus pandemic, there could be confusion in terms of priorities. Financial risk protection for the poor could be neglected as there could be a tendency to tackle the priority of saving lives and other essential aspects of the economy than dealing with the finances for the poor.

Because of that, it is essential even life-saving to regularly and systematically collect and treat information relating to financial risk protection so that there is no further pressure on the existing health crisis. This will contribute to the impact of the action taken for good health and well-being. Also, this will give some evidence that the poor are not left behind as one is trying to save lives and the economy.

For further details about the impact monitoring of financial risk protection in health of the poor at the time of COVID-19 and lockdowns, please contact CENFACS.

________

References

(1) https://www.who.int/health_financing/topics/financial_protection/en/

(2) World Health Organisation (2020), World Health Statistics 2020: Monitoring health for the Sustainable Development Goals @WHO2020

________

Help CENFACS keep the Poverty Relief work going this year.

We do our work on a very small budget and on a voluntary basis. Making a donation will show us you value our work and support CENFACS’ work, which is currently offered as a free service.

One could consider a recurring donation to CENFACS in the future.

Donate to support CENFACS!

FOR ONLY £1, YOU CAN SUPPORT CENFACS AND CENFACS’ PROJECTS, JUST GO TO http://cenfacs.org.uk/supporting-us/

Thank you for visiting CENFACS website and reading this post.

Thank you as well to those who made or make comments about our weekly posts.

We look forward to receiving your regular visits and continuing support throughout 2021 and beyond.

With many thanks.