Happy New Year 2026 and

Welcome Back to CENFACS’ Online Diary!

07 January 2026

Post No. 438

The New Year’s Contents

• What Is New at the Start of the New Year and What Is on This January 2026?

• The 14th Issue of Consume to Reduce Poverty and Climate Change – In Focus: Thoughtful Consumption and Poverty Reduction

• Coming up This Winter: The New Year’s and Next Issue of FACS (The 90th Issue) to Be Titled as African Charities, the Double Transfer (of Climate Technology and Finance) and Poverty Reduction

… And much more!

The New Year’s Key Messages

• What Is New at the Start of the New Year and What Is on This January 2026?

To start 2026, we have planned new programmes, resource, run and skill projects. We are also continuing our Post 2025 Year in Review from where we left it.

• • New Programmes, New Resource, New Run, and New Skill to Bring New Relief and New Hope

New programmes, resource, run and skill projects are 2026 Starting strategic initiatives that focus on growth, innovation and impact. They are part of planning and investment processes in activities designed to better serve the community and beneficiaries while ensuring CENFACS’ long-term sustainability. Let us highlight these new initiatives.

~ New Programmes

They are new services, initiatives or areas of focus that align with CENFACS’ mission. From this January 2026, we have got the following programmes:

√ Financial Empowerment Programme for Households with 2026 Financial Monitoring and Controls, Guidance on Year-end Accounts for Households, and Access to AI-enabled Connected Finance Structured Micro-projects

√ Household- and Area-focused Programmes for Assets and Economy Building

√ Climate Programme Made of Projects to Combat Climate Disinformation, for Finance Mobilisation Roadmap, to Reduce Long-term Energy Poverty, for Voluntary Energy Transitions.

The above-mentioned programmes will help to address new or evolving needs and diversify our impact.

~ New Resource

The key resource for this January 2026 is

√ Consume to Reduce Poverty and Climate Change (Edition No. 14) with a Focus on Thoughtful Consumption and Poverty Reduction.

The resource will assist beneficiaries and service users in their efforts to shift towards sustainable, low-carbon and ethical practices that minimizes waste and support fair labour, local communities and the circular economy. It will guide and empower beneficiaries to make informed decisions by focusing on responsible use of resources.

~ New Run

This includes recurring events or campaigns, particularly fundraising and awareness-raising activities. At the start of this year, we have planned the following initiatives:

√ Financial Capacity and Capability Campaign 2026

√ Be.Africa Forum e-discussion Themes or Topics.

These activities will help to build from past experiences.

~ New Skill Project

This initiative will focus on

√ Zero-waste Skills Development.

At the start of the year, this initiative will help to build project beneficiaries’ capacity, empower them and improve service delivery. Zero-waste skills can help those who have or acquire them to pave their way to poverty reduction.

As ‘borgenproject.org’ (1) points out that

“Zero-waste living alleviates poverty by uplifting small businesses that prioritize ethical, sustainable products and packaging… Zero-waste living can help alleviate poverty by rejecting fast fashion, which exploits workers in impoverished communities”.

The above-mentioned initiatives are amongst the ones we have selected to kick-start 2026. Apart from them, we shall continue to reflect on the poverty reduction landscape of 2025 as part of Post 2025 Year in Review and how we can use the insights from this review to move forward during this year 2026.

• • Post 2025 Year in Review Continues

This is an ongoing series or discussion we are holding to reflect on the events, trends and outcomes of the year 2025 after it ended. The process of looking back and analyzing the past year is not yet finished. The process of evaluating, discussing or presenting the past year’s information and data is still in progress. As part of this process, we will be post-reviewing and working together with beneficiaries on the following:

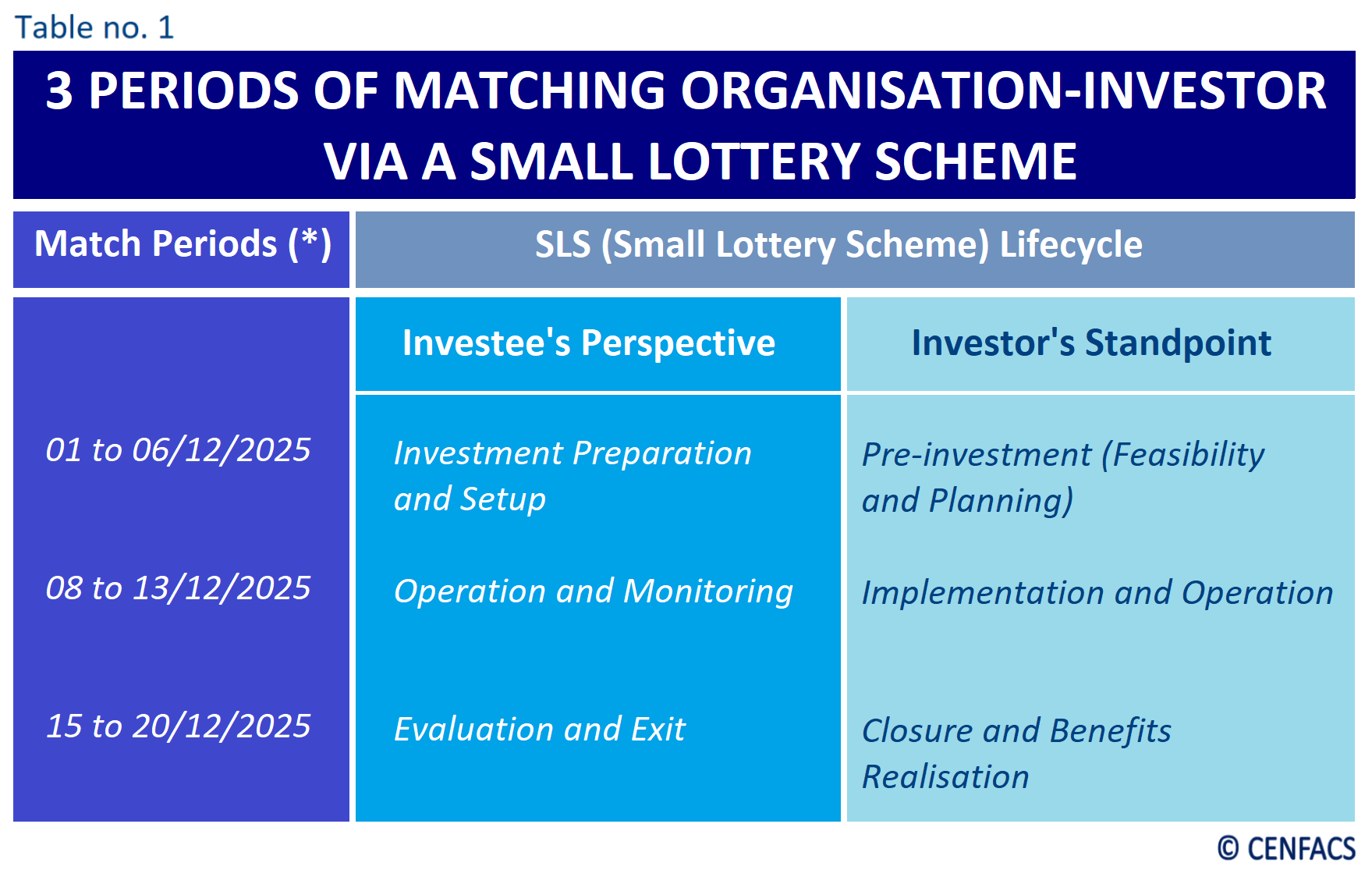

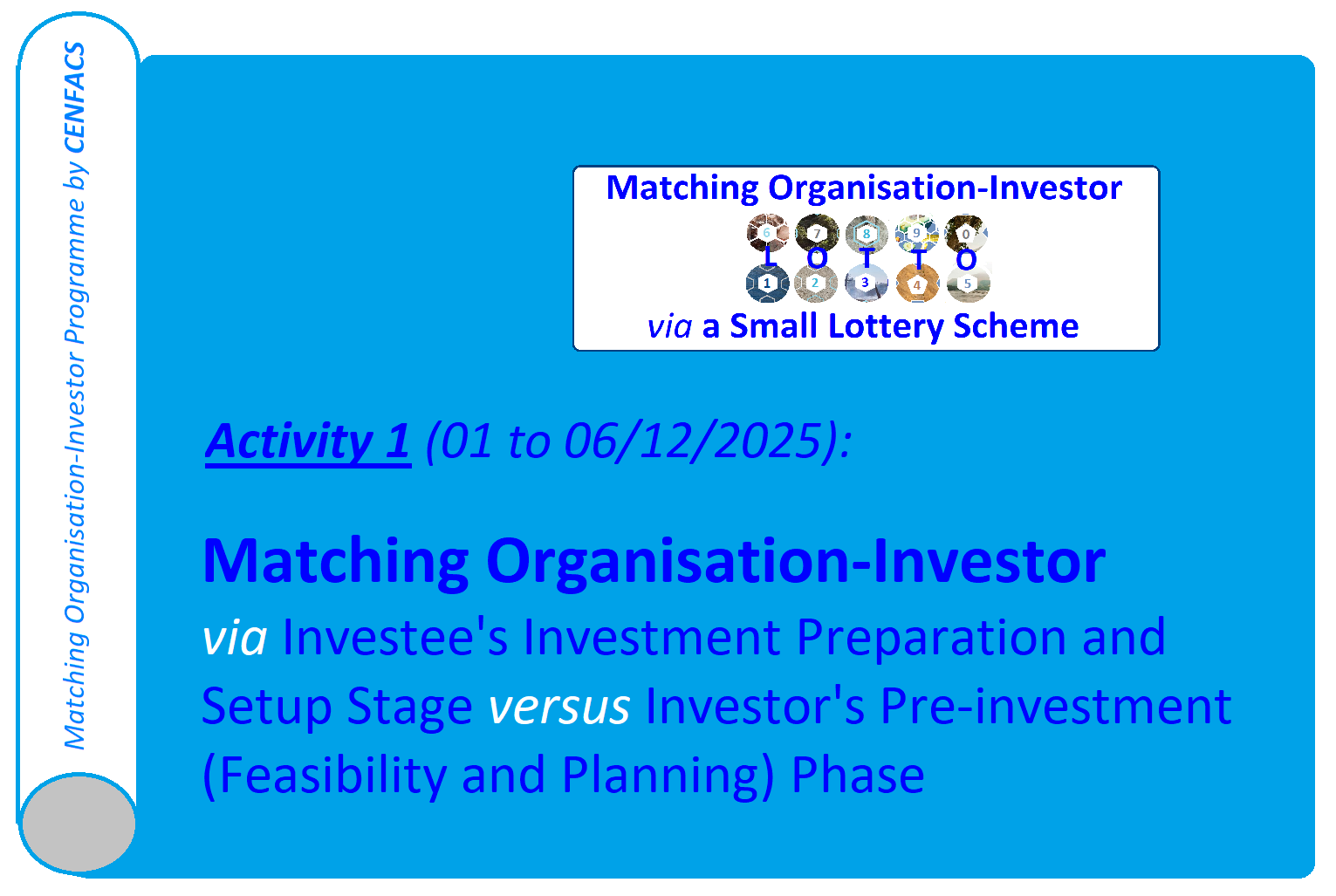

√ Year in Review of Matching Organisation-Investor Programme and Reflection on New Projects that Will Make This Programme in 2026

√ Monitoring, Evaluation and Learning of the Themes Discussed in 2025 in the Context of CENFACS’ be.Africa Forum and Prospects for Africa in 2026

√ Humanitarian Relief Appeals with Six Identified Areas of Priority Appeals that May Need Lighting a Blaze of Hope (as announced last week) to help address unfinished businesses or potential crises or tension hotspot places in Africa

√ Ways of Implementing the Takeaways from Volunteering Winter e-discussion (or Action Plan for 2026) to keep pace with our volunteering action and poverty reduction.

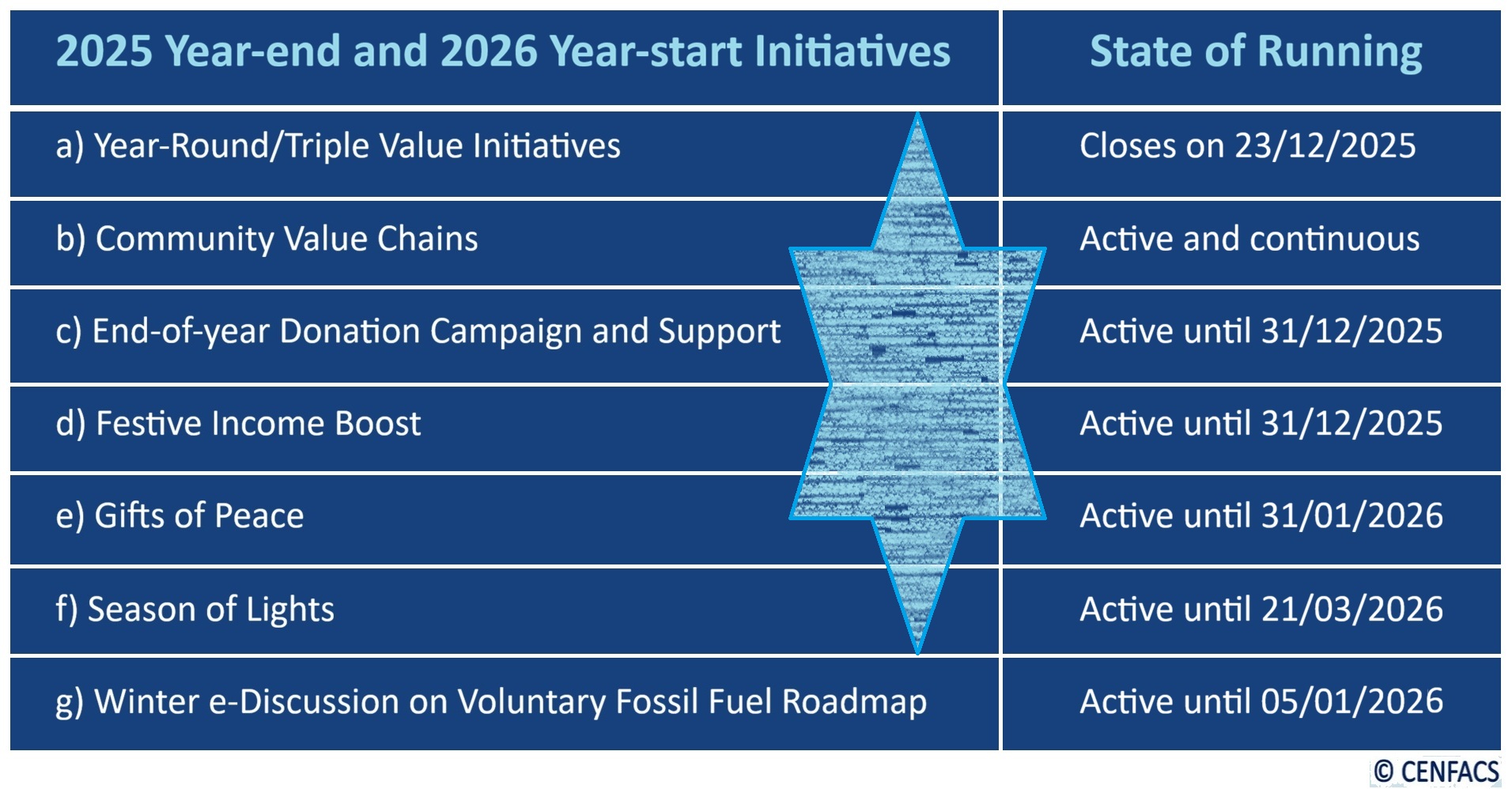

To complete the picture about our working plan for the first quarter of 2026, we shall soon unveil the remaining selected initiatives making the Season of Light at CENFACS.

• The 14th Issue of Consume to Reduce Poverty and Climate Change – In Focus: Thoughtful Consumption and Poverty Reduction

January is the month of Responsible Consumption for CENFACS. The initiative featuring this month is our resource entitled as Consume to Reduce Poverty and Climate Change (CRPCC). In this first post of 2026, we have highlighted the contents this year’s edition of CRPCC – Edition 2026 or the 14th Issue.

The 14th Issue of this resource will be on ‘Thoughtful Consumption and Poverty Reduction’. However, before giving the message about the 14th Issue of CRPCC, let us briefly re-explain what normally happen in January.

• • January as a Month of Responsible Consumption within CENFACS

Some of you are aware that January is our month of Responsible Consumption following CENFACS development calendar. It means that the theme for January is Responsible or Sustainable Consumption and the monthly project carrying this theme is Consume to Reduce Poverty and Climate Change.

• • • What does happen in January?

January is the month we act against poverty due to the lack of consumption, and we deal with measures of poverty reduction through consumption. It is also an opportunity to act to preserve a good relationship between the way in which we consume products on the one hand and the reduction of adverse climate change on the other.

Particularly, January is a climate reminder month as it is the month during which we raise awareness of the relationships between humans and the nature through sustainable consumption; that is consumption that does not destroy the nature or a change in consumption habits that are adjusted to human real needs and to choose market options of promoting environmental conservation and social equality.

• • • What will happen this January?

This January, we will take an extra step by exploring the relationship between humans and thoughtful products and services, between humans and ways of reducing poverty linked to consumption, particularly the consumption of thoughtful products and services.

• • • What is Consume to Reduce Poverty and Climate Change (CRPCC) ?

CRPCC is our users’ New Year supporting information and accompanying booster that focuses on Buying and Consumption elements conducive to the reduction of poverty and hardships and of negative effects of climate change. It is indeed a complimentary support to our Autumn Festive Income Boost (FIB) resource.

The FIB is an income-generating resource while CRPCC brings in a consumption-led look in our fight against poverty and negative climate change. The current Edition (Edition No. 14) of CRPCC deals with ‘Thoughtful Consumption and Poverty Reduction’ as mentioned above.

For further details about CRPCC project, go to http://cenfacs.org.uk/services-activities/

• • The 14th Issue of CRPCC (Consume to Reduce Poverty and Climate Change) – In Focus: Thoughtful Consumption and Poverty Reduction

Our work on making sustainable consumption choices at the start of the year kicks off with Thoughtful Consumption. This work is the continuation of the one carried out on Mindful Consumption in January 2025. In the 13th Issue of CRPCC, the focus was on Mindful Consumption. Consumption was approached as inward on awareness and act of using (that is, intention or presence), addressing personal well-being and habits.

In this Issue (the 14th one), consumption will be looked at outward and at the impact (that is, ethics, environment and society), of the product’s entire lifecycle. Using a conscious approach to consumption, we will try to reflect on values, priorities and impact that one’s consumption can have. In other words, we shall question systems and origins of the products we consume. It is about Thoughtful Consumption. The 2026 Edition of CRPCC is about Thoughtful Consumption and Poverty Reduction. What is then Thoughtful Consumption (TC)?

There are many views on TC. According to ‘Sustainability-directory.com’ (2),

“Thoughtful consumption means making informed, values-aligned choices about what we buy and use, considering impact and purpose”.

The website ‘ranacheikha.com’ (3) takes similar view by arguing that

“At its core, Thoughtful Consumption is the practice of being intentional with what we buy and how we use it. It is about moving away from impulse purchases and instead asking: a) Do I really need this? b) Who made it and under what conditions? c) Will I use it often, and will it stand the test of time?”.

So, the focus for Thoughtful Consumption is external and the goal is to reduce negative externalities (waste, pollution, and unfair labour) by supporting responsible production and systems.

As poverty reduction is part of CENFACS work, Thoughtful Consumption will be approached in its capacity to reduce poverty, notably poverty linked to the lack of conscious or thoughtful consumption.

Thoughtful Consumption can support sustainable products, encourage regenerative agriculture, reduce other forms of consumption (like of meat), promote sustainable fashion, enhance reforestation and conservation, save renewable energy, etc. It can as well help reduce poverty as poor consumers can use awareness of sustainability to make informed decisions on their consumption.

Findings from research can as well back the benefits of Thoughtful Consumption.

For instance, it emerges from Which’s Food Behaviour Dashboard (4) – which is Sustainability Tracker data on consumer food habits, including reducing, recycling and composting food waste and eating less meat and dairy – that a yearly survey with around 2,000 UK adults a year, sampled and weighted to represent the UK population,

“# 41% cut down on food waste by planning what food they buy

# 40% cut down on food waste by composting as recycling leftover food

# Only 27% buy food produced locally”.

The above-mentioned data is from June 2025.

The 2026 Edition of CRPCC is therefore about working with users

a) to support them on the consumption decisions they make and how their decisions can reduce negative externalities and poverty

b) so that they can reduce the stress associated with overconsumption and waste, foster a more peaceful and fulfilling lifestyles conducive to poverty reduction

c) on how they can reflect these consumption decisions on their budget while respecting the 50/30/20 budgeting rule.

The 2026 Edition of CRPCC does not stop there. It provides tips and hints for those who would like to improve their thoughtfulness as far as thoughtless consumption-based poverty is concerned.

Under the Main Development section of this post, we have further explained the theme of ‘Thoughtful Consumption and Poverty Reduction’.

• Coming up This Winter: The New Year’s and Next Issue of FACS (The 90th Issue) to Be Titled as African Charities, the Double Transfer (of Climate Technology and Finance) and Poverty Reduction

The topic of transfer, whether it is about technology or finance, has always be at the heart of the climate talks. The same topic cannot be detached from the problematic of poverty in Africa. This is because if one wants people, in particular the poor ones, to transition away from the use of fossil fuel energies to clean ones, they are required to ensure that these poor people have both the technology and finance to do so. Yet, these poor people may not easily transition away from poverty since the kind of poverty they are experiencing could be linked to the type of technology they are using or do not have, and at the same time they are lacking financial resources to acquire clean technologies. In this respect, there could be a need to operate a double transfer of both climate technology and climate finance to these peoples or communities in need of energy transition and of means to finance this transition.

Perhaps, to elucidate what we are talking it is better to explain the concepts of climate technology, climate finance and the double transfer. Let us start with climate technology. From the perspective of ‘unepccc.org’ (5),

“Climate technologies are all those technologies that are instrumental in contributing to achieving mitigation and adaptation objectives and they exhibit similar patterns as other technologies, particularly in terms of geographical concentration in high income countries and low levels of diffusion in developing countries”.

As to climate finance, the website ‘explorian.io’ (6) explains that

“Climate finance in developing countries refers to financial flows support, and investment provided by developed countries, international institutions and other sources to assist developing nations in implementing climate action initiatives, such as mitigating greenhouse gas emissions and adapting to the impacts of climate change”.

Both climate technology and climate finance can be transferred. It is this double transfer that this Issue 90 is dealing with. Within the climate literature, double transfer in climate action refers to the linked process of transferring climate technology and climate finance from developed to developing countries. The double transfer suggests that there is a need for a coordinated approach that involves both the transfer of technology and the transfer of financial resources.

Concerning this double transfer, African Charities – particularly CENFACS’ Africa-based Sister Organisations working on the ground in their areas of operation in Africa – found there is a lack of or gap in climate technology and climate finance. It is the interlinkage of these two problems and their links to poverty or poverty reduction that the 90th Issue of FACS is about.

The 90th Issue deals with challenges and potential negative impacts (such as challenge linked to accessing climate funds by African Charities, capacity gaps, the character donor-centric of climate finance, the lack of local ownership in technology transfer, the problem of climate accountability and transparency, and funding disparities).

Both technology and finance transfers do not happen in the vacuum. They happen through a channel. The 90th Issue will highlight the key mechanisms for technology transfer (like direct financial support, technical assistance, and capacity building, collaborative partnerships, hard technology deployment). In this respect, the 90th Issue will deal with the economic case for climate technology transfer as climate technologies offer new or alternative solutions in different areas that are important to economic development and poverty reduction.

In the context of the 90th Issue, we are going to consider the transfer done through multinational charities or charitable corporations. From this perspective, the 90th Issue of FACS will deal with the transfers of both climate technology and climate finance to Africa or African Charities in the context of multinational charitable entities, while looking at the principles or theories and practices underpinning these transfers.

In this regard, the 90th Issue will consider theories and frameworks for climate technology transfer (like national innovation systems, market-based mechanisms and firm level theories, enabling environments, equity and redistribution claims, intellectual property rights, etc.) and theories of climate finance (such as transformational finance theory, additionality principle, theory of change models, etc.), as well as their suitability or unsuitability with the contents of the 90th Issue.

The 90th Issue will particularly focus on the double transfer theory, which posits that climate technology transfer and climate finance transfer are intrinsically linked and mutually reinforcing. The double transfer theory emphasizes the importance of understanding the specific bottlenecks that constrain the transfer of climate technologies and the role that development cooperation can play in enabling it. It also highlights the need for international support to accelerate the transfer of climate technologies to developing countries.

The 90th Issue will as well look at the key relationships between African Charities, climate finance transfer, climate technology transfer and poverty reduction in Africa. These relationships will be checked at the levels of access to climate finance, project implementation and technology, capacity building and innovation, barriers to access to climate technologies and finance by African Charities, poverty reduction and local relevancy.

Finally, the 90th Issue will treat of the role that Africa Charities play as intermediaries, capacity builders, and project implementors in the transfer of climate technologies and finance, particularly in reaching local communities and having projects align with local needs.

More details about what the 90th Issue of FACS will be given this Winter. However, for those who would like to enquire about it before it appears, they should not hesitate to contact CENFACS.

The New Year’s Extra Messages

• Goal of the Month: Reduction of Poverty Linked to Thoughtless Consumption

• Guidance for Households to Manage and Close Year-end Accounts

• The Gifts of Peace, Edition 2025-2026

• Goal of the Month: Reduction of Poverty Linked to Thoughtless Consumption

To approach this Goal, it is better to explain thoughtless consumption and provide what can be done to reduce this type of poverty.

• • What Is Thoughtless Consumption or Poor Spending Habit?

It emerges from the consumption literature that thoughtless consumption is used to describe the behaviour that can lead to financial hardship. From this finding, poverty will be approached from the perspective of individual deficiency theory of poverty, which attributes being poor is a personal choice or lack of effort.

Indeed, it is known that consumption choices can reduce or exacerbate poverty. Households with limited resources can stay above the poverty line if they thoughtfully consume. Because of this possibility of staying above the poverty line, this suggests that it is possible to reduce poverty linked thoughtless consumption.

• • Actions to Reduce Poverty Linked to Thoughtless Consumption

There are actions that can be taken at systemic and policy levels, and individual level to reduce poverty linked to thoughtless consumption. By focusing on individual-level solutions, the theory on this matter recommends the following key actions:

∝ Practise mindful consumption

∝ Buy second-hand or borrow

∝ Reduce meat and energy consumption

∝ Support sustainable businesses

∝ Plan and avoid waste

∝ Advocate for change

Etc.

By taking these actions, one can navigate out or transition away from poverty linked to thoughtless consumption.

• • Implications for Selecting the Goal for the Month

After selecting the goal for the month, we focus our efforts and mind set on the selected goal by making sure that in our real life we apply it. We also expect our supporters to go for the goal of the month by working on the same goal and by supporting those who may be suffering from the type of poverty linked to the goal for the month we are talking about during the given month (e.g., January 2026).

For further details on the goal of the month, its selection procedure including its support and how one can go for it, please contact CENFACS.

• Guidance for Households to Manage and Close Year-end Accounts

As part of our Financial Empowerment Programme for Households, we are providing guidance on financial management, offering support for preparing year-end accounts, and facilitating access to professional accounting services. This guidance service includes financial guidance, accounting support, and community engagement.

• • Financial Guidance

It involves advice on managing finances, budgeting and understanding financial statements to help households navigate their year-end accounts.

• • Accounting Support

It includes providing professional accounting service or signposts to assist households in preparing their year-end accounts, ensuring compliance with regulatory or regular requirements.

• • Community Engagement

It is about engaging with the community to promote financial literacy and numeracy, as well as providing informational resources for households to effectively manage their finances.

Those who will be interested in this Guidance Service, they should not hesitate to contact CENFACS.

• The Gifts of Peace, Edition 2025-2026

The Gifts of Peace for Edition 2025-2026, which are already running and trending, will end on 31 January 2026. If you have not yet supported, you can still do something for poverty relief.

Although the deadline for the Season of Donation for these gifts is 31 January 2026, we will still accept any donations made after this deadline to enable those who will not be in a position to donate by this deadline to have a chance to donate after.

Please do not wait for the expiration of the deadline as the needs are pressing and urgent.

We know that many supporters of good causes have been affected by the polycrises of recent years. We are as well aware of the current economic situation of the UK economy which does not make easier for people of all financial abilities to donate to good causes.

However, for those who can please do not hesitate to support these noble causes of peace since the potential beneficiaries of them are trebly impacted by:

a) The lingering economic effects of previous crises

b) The already extremely poor conditions in which they are living

c) The scars of the enduring high costs of living.

Every support counts to help reduce and end extreme poverty.

Please keep the Gifts of Peace in your mind as the giving season continues.

For further details about these Gifts of Peace (that keep making helpful difference) and or to support, go to http://cenfacs.org.uk/supporting-us/

We look forward to your support. Thank you!

The New Year’s Message in French (Le Message du Nouvel An en Français)

• À Paraître cet Hiver : Le Nouvel An et le Prochain Numéro de FACS (le 90ème numéro) qui s’intitulera « Oeuvres de Charité Africaines, le Double Transfert (de la Technologie et des Financements Climatiques) et la Réduction de la Pauvreté »

Le sujet du transfert, qu’il s’agisse de technologie ou de finance, a toujours été au cœur des négociations sur le climat. Le même sujet ne peut être dissocié de la problématique de la pauvreté en Afrique.

En effet, si l’on veut que les populations, en particulier les plus pauvres, passent de l’utilisation des énergies fossiles à des énergies propres, il est nécessaire de s’assurer que ces personnes pauvres disposent à la fois de la technologie et des ressources financières pour le faire. Cependant, ces personnes pauvres peuvent ne pas réussir facilement à sortir de la pauvreté, car le type de pauvreté qu’elles connaissent peut être lié au type de technologie qu’elles utilisent ou n’ont pas, et en même temps, elles manquent de ressources financières pour acquérir des technologies propres. Par conséquent, il pourrait être nécessaire d’opérer un double transfert à la fois de technologies climatiques et de financements climatiques vers ces populations ou communautés ayant besoin d’une transition énergétique.

Peut-être, pour éclairer ce dont nous parlons, il est préférable d’expliquer les concepts de technologie climatique, de financement climatique et du double transfert. Commençons par la technologie climatique.

Du point de vue de ‘unepccc.org’ (5), “Les technologies climatiques sont toutes ces technologies qui contribuent de manière instrumental à l’atteinte des objectifs de mitigation et d’adaptation et elles présentent des schémas similaires à d’autres technologies, notamment en termes de concentration géographique dans les pays à revenu élevé et de faibles niveaux de diffusion dans les pays en développement”.

En ce qui concerne le financement climatique, le site ‘explorian.io’ (6) explique que “Le financement climatique dans les pays en développement fait référence aux flux financiers, au soutien et aux investissements fournis par les pays développés, les institutions internationales et d’autres sources pour aider les nations en développement à mettre en œuvre des initiatives d’action climatique, telles que la réduction des émissions de gaz à effet de serre et l’adaptation aux impacts du changement climatique”.

La technologie climatique et le financement climatique peuvent tous deux être transférés. C’est ce double transfert que traite ce numéro 90. Dans la littérature sur le climat, le double transfert dans l’action climatique fait référence au processus lié de transfert de la technologie climatique et du financement climatique des pays développés vers les pays en développement. Le double transfert suggère qu’il y a besoin d’une approche coordonnée impliquant à la fois le transfert de technologie et le transfert de ressources financières.

Concernant ce double transfert, les Oeuvres de Charité Africaines ou Associations Caritatives Africaines – en particulier les Organisations Sœurs Africaines de CENFACS travaillant sur le terrain dans leurs zones d’opération en Afrique – ont constaté qu’il y a un manque ou une lacune en matière de technologie climatique et de financement climatique. C’est l’interconnexion de ces deux problèmes et leurs liens avec la pauvreté ou la réduction de la pauvreté qui est abordée dans le 90e numéro de FACS.

Le 90e numéro traite des défis et des impacts potentiellement négatifs (tels que les défis liés à l’accès aux fonds climatiques par les associations africaines, les lacunes de capacités, le caractère axé sur le donateur du financement climatique, le manque de propriété locale dans le transfert de technologies, le problème de la responsabilité et de la transparence climatiques, et les disparités de financement).

Le transfert de technologies et de financements ne se fait pas dans le vide. Il se fait à travers un canal. Le 90e numéro mettra en évidence les principaux mécanismes de transfert de technologies (comme le soutien financier direct, l’assistance technique et le renforcement des capacités, les partenariats collaboratifs, le déploiement de technologies avancées). À cet égard, le 90e numéro traitera des arguments économiques en faveur du transfert de technologies climatiques car les technologies climatiques offrent de nouvelles solutions ou des solutions alternatives dans différents domaines importants pour le développement économique et la réduction de la pauvreté.

Dans le cadre du 90ᵉ numéro, nous allons examiner le transfert effectué par le biais d’associations caritatives multinationales ou de sociétés caritatives. Dans cette perspective, le 90ᵉ numéro de FACS traitera des transferts à la fois de technologies climatiques et de financements climatiques vers l’Afrique ou les Oeuvres de Charité Africaines (Associations Caritatives Africaines) dans le contexte d’entités caritatives multinationales, tout en analysant les principes ou théories et pratiques sous-jacents à ces transferts.

À cet égard, le 90ᵉ numéro examinera les théories et cadres pour le transfert de technologies climatiques (comme les systèmes nationaux d’innovation, les mécanismes basés sur le marché et les théories au niveau des entreprises, les environnements favorables, les revendications d’équité et de redistribution, les droits de propriété intellectuelle, etc.) et les théories du financement climatique (telles que la théorie du financement transformationnel, le principe d’additionalité, les modèles de théorie du changement, etc.), ainsi que leur pertinence ou inadaptation par rapport au contenu du 90ᵉ numéro.

Le 90e numéro se concentrera particulièrement sur le double transfert, qui postule que le transfert de technologies climatiques et le transfert de financements climatiques sont intrinsèquement liés et se renforcent mutuellement. La théorie du double transfert souligne l’importance de comprendre les goulots d’étranglement spécifiques qui limitent le transfert de technologies climatiques et le rôle que la coopération au développement peut jouer pour le faciliter. Elle met également en évidence la nécessité d’un soutien international pour accélérer le transfert de technologies climatiques vers les pays en développement.

Le 90e numéro examinera également les relations clés entre les Oeuvres de Charité Africaines (Organisations Caritatives Africaines), le transfert de financements climatiques, le transfert de technologies climatiques et la réduction de la pauvreté en Afrique. Ces relations seront analysées aux niveaux de l’accès aux financements climatiques, de la mise en œuvre des projets et des technologies, du renforcement des capacités et de l’innovation, des obstacles à l’accès aux technologies et financements climatiques par les organisations caritatives africaines, de la réduction de la pauvreté et de la pertinence locale.

Enfin, le 90e numéro traitera du rôle que jouent les associations africaines en tant qu’intermédiaires, bâtisseur(se)s de capacités et responsables de mises en œuvre de projets dans le transfert des technologies et du financement climatiques, en particulier pour atteindre les communautés locales et aligner les projets sur les besoins locaux.

Plus de détails sur ce que sera le 90e numéro de FACS seront donnés cet hiver. Cependant, pour ceux ou celles qui souhaitent se renseigner avant sa parution, ils/elles ne devraient pas hésiter à contacter le CENFACS.

The New Year’s Main Development

• The 14th Issue of Consume to Reduce Poverty and Climate Change

In Focus: Thoughtful Consumption and Poverty Reduction

• • Key Highlights, Tips and Hints about the 14th Issue of CRPCC

The key highlights, Tips and Hints include the following:

∝ Key Terms

∝ Relationships between Thoughtful Consumption and Poverty Reduction

∝ Approach to Thoughtfulness and Thoughtful Consumption Model

∝ Thoughtful Consumption Shopping Basket

∝ Thoughtful Consumption as Part of the United Nations Sustainable Development Goal Targets 12.1 and 12.5

∝ Thoughtful Consumption and the Growing Climate Economy

∝ Thoughtful Consumption in the Context of Changing Climate and Life-threatening Impacts of Climate Change

∝ Thoughtful Consumption and Crises

∝ Thoughtful Consumers and Their Affordability of Thoughtful Products

∝ Thoughtful Consumption Good Practices within the Community

∝ Demonstrative Projects of Thoughtful Consumption

∝ Tackling Barriers to Achieve Thoughtful Consumption Goals

∝ Budgeting for Thoughtful Consumption

∝ Thoughtful Consumption Indication on Products for Verification, Identity and Authenticity

∝ Thoughtful Security and Guarantee

∝ Looking for Help and Support on Thoughtfulness.

Let us consider these key highlights, tips and hints.

• • • Key Terms

There are three terms that facilitate the understanding of the 2026 Edition of CRPCC. These terms are thoughtful consumption, thoughtful spending, and the 50/30/20 budgeting rule. Let us briefly explain them.

• • • • What is Thoughtful Consumption?

To understand thoughtful consumption, we are going to start by explaining consumption. Consumption is understood here from the definition given by Chris Park (7) as

“The process of using resources to satisfy human wants or needs” (p. 96)

From this definition, consumption is being perceived from the micro-economic perspective (from the point of view of individuals, households and firms), not at national or aggregate demand level. Consumption is here the use of goods and services by individuals or households. That consumption can be thoughtful or thoughtless.

There are many views on Thoughtful Consumption (TC). According to ‘Sustainability-directory.com’ (op. cit.),

“Thoughtful consumption means making informed, values-aligned choices about what we buy and use, considering impact and purpose”.

The website ‘ranaacheikha.com’ (op. cit.) takes similar view by arguing that

“At its core, Thoughtful Consumption is the practice of being intentional with what we buy and how we use it. It is about moving away from impulse purchases and instead asking: a) Do I really need this? b) Who made it and under what conditions? c) Will I use it often, and will it stand the test of time?”.

So, the focus for TC is external and the goal is to reduce negative externalities (waste, pollution, and unfair labour) by supporting responsible production and systems.

As poverty reduction is part of CENFACS work, TC will be approached in its capacity to reduce poverty, notably poverty linked to the lack of conscious or thoughtful consumption.

In this 14th Edition of CRPCC, we are interested in that part of consumption that is thoughtful or relating to essentials or real needs.

Thoughtful consumption is related to thoughtful spending or essential expenses. Like any spending or expenses, they are part of budgeting rule. Amongst budgeting rules, there is a 50/30/20 budgeting rule.

• • • • What is the 50/30/20 Budgeting Rule?

The website ‘thebalancemoney.com’ (8) argues that the 50/30/20 rule of thumb, which originates from the 2005 book written by US Senator Elizabeth Warren and her daughter Amelia Warren Tyafi, is

“A way to allocate your budget according to three categories: needs, wants and financial goals”.

According to this rule, you should spend 50% of your income on needs (essentials like rent/mortgage, utilities, insurance, healthcare and groceries); 30% on wants (that is, discretionary spending on things like dining out, entertainment, hobbies, streaming services, and shopping beyond basic needs); and 20% on savings/debt repayment (which include contributions to retirement funds, emergency savings, and extra payment in debt).

TC complements the 50/30/20 budget rule by aligning spending with personal values, making it easier to meet savings goals, and reducing expenses in the ‘wants’ part of this rule.

If one follows this rule, thoughtful spending is the one we are dealing with here.

• • • • What is Thoughtful Spending?

Online research suggests that Thoughtful Spending (TS) is the conscious act of making purchase decisions based on your values and financial goals, rather than habit or emotion. There is a link between TS and 50/30/20 rule. In particular, the link between TS and 50/30/20 rule is strong in managing the ‘wants’ category.

Key aspects of TS include intentionality, awareness, goal orientation, and the distinction of needs from wants. To practise TS, one needs to do the following:

∝ to budget

∝ to pause before buying

∝ to identify the root motivation behind their desire to buy

∝ to calculate cost in hours of work it takes to afford an item

∝ to invest in quality or longevity

∝ and to spend on things that improve their well-being.

To put thoughtful spending in practice, one can create a budget journal for it.

In the context of the 14th Edition of CRPCC, we are interested in the 30% of our users’ budget or ‘Wants‘ category. We would like to ensure that expenses in the ‘Wants’ category are intentional and aligned with personal values, rather than impulse purchases. This discipline helps keep spending with the 30% allocation, making the overall budget achievable and effective for financial goals.

We are looking at if there is any relationship between TC or TS and poverty reduction and how we can work with the users of CRPCC to reduce consumption-based poverty, which could be linked with thoughtless consumption.

• • • Relationships between Thoughtful Consumption and Poverty Reduction

TC can help reduce poverty by promoting sustainable practices and addressing the needs of the poor. This can be done via consumer choices, social inclusion and sustainable practices. This can be explained as follows.

~ Consumer choices: TC can encourage consumers to prioritize quality and sustainability, which can lead to poverty reduction by fulfilling basic needs and reducing reliance on non-essential items.

~ Social inclusion: TC can help shift spending priorities towards essential items, thereby improving the quality of life for those in need.

~ Sustainable practices: By conserving resources and promoting efficient use, consumers can contribute to a more sustainable future that benefits the poor.

• • • Approach to Thoughtfulness and Thoughtful Consumption Model

The 2026 Edition of CRPCC refers to the minimalist approach which considers quality possessions rather than a large quantity of stuff. The approach takes into account the interplay between the awareness of needs and wants, as well as how to focus on real needs rather than wants. By taking this approach, one will agree to consume less and care for repair, reuse and recycle.

Those using this approach will obviously adopt its underlying model and premises. The definition of this model is contained in the definition of TC itself.

Indeed, a TC model is an approach to purchasing and using goods and services that involves a deliberate consideration of their environmental, social and economic impacts. It encourages consumers to move beyond impulsive or habitual buying and make informed, value-aligned choices.

The core principles of this model are the distinction between genuine needs and fleeting wants, quality over quantity, awareness of impact, values alignment, and the 5 R’s (Reduce, Reuse, Repair, Recycle and Rot).

Briefly speaking, the model is a transformation from wasteful consumption into a conscious, intentional practice that contributes to both personal well-being and sustainable world.

• • • Thoughtful Consumption Shopping Basket

Let us start with this question:

What is a thoughtful consumer products shopping basket?

It is a conceptual collection of goods that reflects the purchasing choices of consumers who are deliberate, budget-conscious, and potentially focused on sustainability and ethical concerns. The basket includes carefully considered purchases, value and quality focus, conscious choices, sustainability and tics, and mindful consumption products.

Using the internet, e-mail, social networks and other communication technologies; it is possible to get enough information on how to go thoughtful and which products and services that meet thoughtful consumption while reducing poverty linked to thoughtlessness at the same time. It is as well possible to find resources and websites that compare and contrast these kinds of products, services and prices. People can then choose products and services that are good value for TC and add them to their online shopping basket or to make their shopping basket.

• • • Thoughtful Consumption as Part of the United Nations Sustainable Development Goal Target 12.1 and 12.5

The United Nations Sustainable Development Goal 12 (9) is:

“Ensure sustainable consumption and production patterns“.

Its Target 12.1 is:

“Implement the 10-year framework of programmes on sustainable consumption and production, all countries taking action, with developed countries taking the lead, taking into account the development and capabilities”.

Its Target 12.5 is:

“By 2020, substantially reduce waste generation through prevention, reduction, recycling and reuse“.

As these goal targets were written, TC echoes them. TC reduces the stress associated with overconsumption and waste, foster a more peaceful and fulfilling lifestyles. In doing so, it helps demand for products and practices that do not harm forests and contribute to deforestation and overgrazing. Briefly, it reduces environmental footprint.

• • • Thoughtful Consumption and the Growing Climate Economy

The process of using resources in a frugal way to satisfy human wants and needs can go hand in hand with an organised system for the production, distribution and use of goods and services that takes into account the changing weather conditions. In other words, consuming anti-wasteful and essential products and resources can help reduce adverse climate change.

As climate economy (that is, a system which attempts to solve the basic economic problem of climate) continues to grow, it can bring new climate educational opportunities, economic savings and improved well-being for the poor. These attributes of the Growing Climate Economy (GCE) can help them consume goods and services that are thoughtful/essential and have less or no harmful wasteful materials.

Research can continue to enlarge the scope of thoughtful goods and services that do not cause harms and wastes to the environment. Findings from this research can help boost the GCE.

• • • Thoughtful Consumption in the Context of Changing Climate and Life-threatening Impacts of Climate Change

Maybe enough has been said about the impacts of changing climate. If not, then one area of work could be for humans to rethink about the positive results that their TC can create and properly market or raise awareness of these outcomes or results. There are positive outcomes or results deriving for TC that need to be known by the members of the public and be part of their daily life.

At CENFACS, the Guidance Service on Thoughtfulness, which we will be running this January, is part of the efforts to support the members of our community who would like to stay or be thoughtful with their consumption and spending. By taking this thoughtful drive, this can help to reduce or mitigate the threats and impacts of the changing climate on them.

• • • Thoughtful Consumption and Crises

In times of crises, TC can offer numerous benefits by helping individuals manage resources, reduce waste, and build community resilience.

Benefits of TC in a crisis can include the ones below.

~ Financial resilience: Prioritizing essential needs and avoiding impulse purchases helps individuals manage their finances more effectively during economic instability caused by a crisis.

~ Resource management and availability: Buying only what is needed rather than engaging in panic buying or hoarding.

~ Waste reduction: Crises often strain waste management systems. TC reduces the amount of waste generated, easing pressure on public services and conserving raw materials.

~ Supporting local economies: Focusing on local businesses and producers can help maintain the economic health of the community during a crisis.

~ Building community solidarity: Consuming thoughtfully demonstrates that one has consideration for their neighbours and contribute to a stronger bond.

~ Reduced environmental impact: By thoughtfully consuming, individuals lessen their overall environmental footprint.

~ Mental well-being: TC provides a sense of control and purpose during the uncertainty of a crisis. So, making conscious choices about what to buy and use helps individuals feel more grounded and less anxious about resource scarcity.

Briefly speaking, crises and shocks (like the economic ones) could be a reminder of the benefits of thoughtfulness in our life.

• • • Thoughtful Consumers and Their Affordability of Thoughtful Products

The question that one should answer is this:

Are Thoughtful Consumer Products Affordable for Everyone?

They are not universally unaffordable when considering long-term value and a range of purchasing strategies. They emphasize durability and quality over quantity, and they can lead to savings over time. In other words, TC is not always the cheapest one. Not everybody can afford to buy thoughtful goods as many of the people living in poverty have a low real disposable income. Not all the low-income families or households can afford to finance the basic necessities of life or to consume thoughtfully. Many of them need some support to supplement their real disposable income since many of have income below the international poverty line.

Giving them advisory support in terms how to increase your income, to make some changes in their expenses budget and find affordable TC goods and services should be a priority amongst other ones. In this respect, a list of where to find affordable thoughtful consumption goods and services in this CRPCC resource can be lifesaving.

• • • Thoughtful Consumption Good Practices within the Community

Despite the problem of affordability of TC goods for low-income poor people and families, there could be nonetheless TC good practices within our community. To back up these practices, the 14th Issue of CRPCC highlights some cases of TC good initiatives undertaken by the CENFACS Community that underpins TC accounts as part of every day’s human life.

In this respect, those who have cases of TC practices and who may find them worthwhile to share and be added to this issue of CRPCC, they can let CENFACS know.

• • • Demonstrative Projects of Thoughtful Consumption

In TC economy, every shopper can demonstrate the ability to follow the rules of consuming thoughtfully. There could be those consumers who do more by taking a proactive action to consume thoughtfully.

Likewise, there could be local projects (for example, local thoughtful charitable shops, thoughtful budget stores and community organisations) that could display demonstrative talents and skills in promoting TC goods, services and habits which are zero-waste or net zero.

These projects focus on building community and reducing environmental impacts by sharing, repairing, and localising resources. These initiatives challenge the ‘take-make-waste’ model of consumerism and promote a more circular and sustainable lifestyle.

Types of these projects include repair cafés, tool libraries or libraries of things, community swap events, local food co-ops, community gardens, clothing swaps, community fridges, sustainable fashion initiatives, etc.

They empower residents to share resources, reduce waste, and build skills, while promoting social cohesion and connection alongside environmental benefits.

For those members of our community who have developed this kind of demonstrative projects of TC, it could be a good idea to let us know so that we can add them to this CRPCC resource.

• • • Tackling Barriers to Achieve Thoughtful Consumption Goals

There could be some handicaps for people and families to achieve TC goals. One of the barriers is the lack of income or awareness or education that extremely poor people experience that could push them out of reach of TC products. Despite that in charitable world and economy in which no one is left behind, there could be still access for everybody to TC goods and services.

However, people and families do not like TC to happen to them in this way since they would like to work and pay for their TC. Because of the barriers they face in finding opportunity to work and earn decent income, their prospect for meeting their TC goals can become remote. This is without forgetting hikes in price of consumption goods and services, including the thoughtful ones.

As part of tackling these barriers, the current resource provides some leads in terms of print and online resources that users can further explore in order to respond to some their TC problems.

To tackle barriers to achieve TC goals involves a combination of personal strategies to address psychological hurdles and broader efforts to drive systemic change.

Individual strategies can include breaking habits gradually, prioritizing sufficiency, automating sustainable choices, education yourself, building your own support system, and tracking your impact.

Systemic approaches can involve advocating for policy changes, promotion education and transparency, supporting sustainable infrastructure, and challenging consumer culture.

• • • Budgeting for Thoughtful Consumption

It is a good idea for users to budget for TC goods and services as part of the overall of household budgeting process. This kind of preparation in terms of financial statement for any planned incomes and expenses for a particular period can help to maximise the use of resources and reduce wasteful spending in terms of what is thoughtful and thoughtless consumption. It can as well provide alternative to thoughtless consumption to reduce poverty and hardships due to waste.

• • • Thoughtful Consumption Indication on Products for Verification, Identity and Authenticity

It is a good idea for any consumer, rich or poor, to check thoughtful features on their buys and other specifications and read other people’s testimonies, reviews or comments about it. In this respect, selling the positive idea of TC could be helpful for thoughtful consumers.

• • • Thoughtful Security and Guarantee

When buying thoughtful consumption products and services (whether using online or a physical store), one needs to check, compare and contrast products, terms and conditions of business, buying terms, prices, etc. There is a need to check as well guarantees and safety policies for thoughtful features.

If you are buying online, before you sign up, add to your TC shopping basket and purchase an item; you need to read, discuss and check what you are agreeing on. You need to proceed with the following:

<> Investigate a product’s supply chain, labour practice and environmental cost

<> Choose brands that are fair-trade, eco-friendly or locally sourced

<> Consider the broader social and environmental consequences of your purchase

Etc.

You may even take more precautions when selecting items, filling up buying forms to enter your personal, financial information and sensitive details.

In today’s world of digital and artificial intelligence technologies (e.g., AI Chatbots), you can even ask these technologies your thoughtfulness questions to find answers for you.

You should also be aware of scams and illegal and malicious practices. For your own online security, use the e-safety tools and advice.

• • • Looking for Help and Support on Thoughtful Consumption

As explained earlier, TC is a conscious and deliberate approach to purchasing and utilising goods and services, where individuals consider the environmental, social, and personal impacts of their choices. There are individuals who can easily adopt this approach. There are others who may be struggling in their TC steps or drive.

For those users who are looking for help and support, we can work with them so that they can navigate their way out of thoughtless consumption-based poverty. We can together explore the following options or tips to deal with thoughtful or thoughtless spending:

√ Improving their spending intent

√ Creating a budget to track income and expenses and deal with emotional triggers

√ Pausing before purchasing

√ Identifying the root motivation (boredom, stress and true need) behind the desire to buy

√ Setting up cost cutting targets on budget items such as takeaways, eating out, clothing, etc.

√ Calculating cost in hours by determining how many hours to work it takes to afford an item

√ Switching to cheap thoughtful retailers to save money

√ Investing in quality or longevity by choosing durable or sustainable items that last and reduce future waste

√ Trimming budget

√ Prioritising expenses

√ Setting up a policy not to borrow money for thoughtless expenses

√ Adopting cost-saving behaviour

√ Spending on things that genuinely improve their well-being

√ Briefly, developing a strategy or policy for TS to help them decide that their money is invested in things that support well-being, connection, and meaningful experiences, not just accumulation.

We can even work with them on a project to write their budget journal for TS.

The above-mentioned options or tools will help them to build confidence throughout 2026 and beyond.

For those users who would like to dive into the reduction of thoughtless consumption-based poverty, we can provide them with online and print resources relating to this matter. These resources highlight the TS tips and hints.

There is a lot of online resources and websites they can sign up and receive advice on this matter.

The above are the key highlights, tips and hints about the 14th Issue of CRPCC, which we wanted to share with you.

For any further details about Thoughtful and Responsible Consumption and to get the full 2026 Edition of Consume to Reduce Poverty and Climate Change, please contact CENFACS.

_________

• References

(1) https://borgenproject.org/zero-waste-living (accessed in December 2024)

(2) https://lifestyle.sustainability-directory.com/term/thoughtful-consumption/ (accessed in January 2026)

(3) https://ranacheikha.com/blogs/the-shoe-advisor-leather-sgoe-care/thoughtful-consumption-choosing-what-matters (accessed in January 2026)

(4) https://www.which.co.uk/policy-and-insight/article/food-dashboard-aa9SR6s2NqVe (accessed in in January 2026)

(5) https://unepccc.org/wp-content/uploads/2023/06/tech-transfer-policy-brief-oecd.pdf (accessed in January 2026)

(6) https://explorian.io/climate-finance-in-developing-countries (accessed in January 2026)

(7) Park, C. (2011), Oxford Dictionary of Environment and Conservation, Oxford University Press, Oxford & New York

(8) https://www.thebalancemoney.com/the-50-30-20-rule-of-thumb-453922 (accessed in January 2024)

(9) https://sdgs.org/goals (accessed in January 2026)

_________

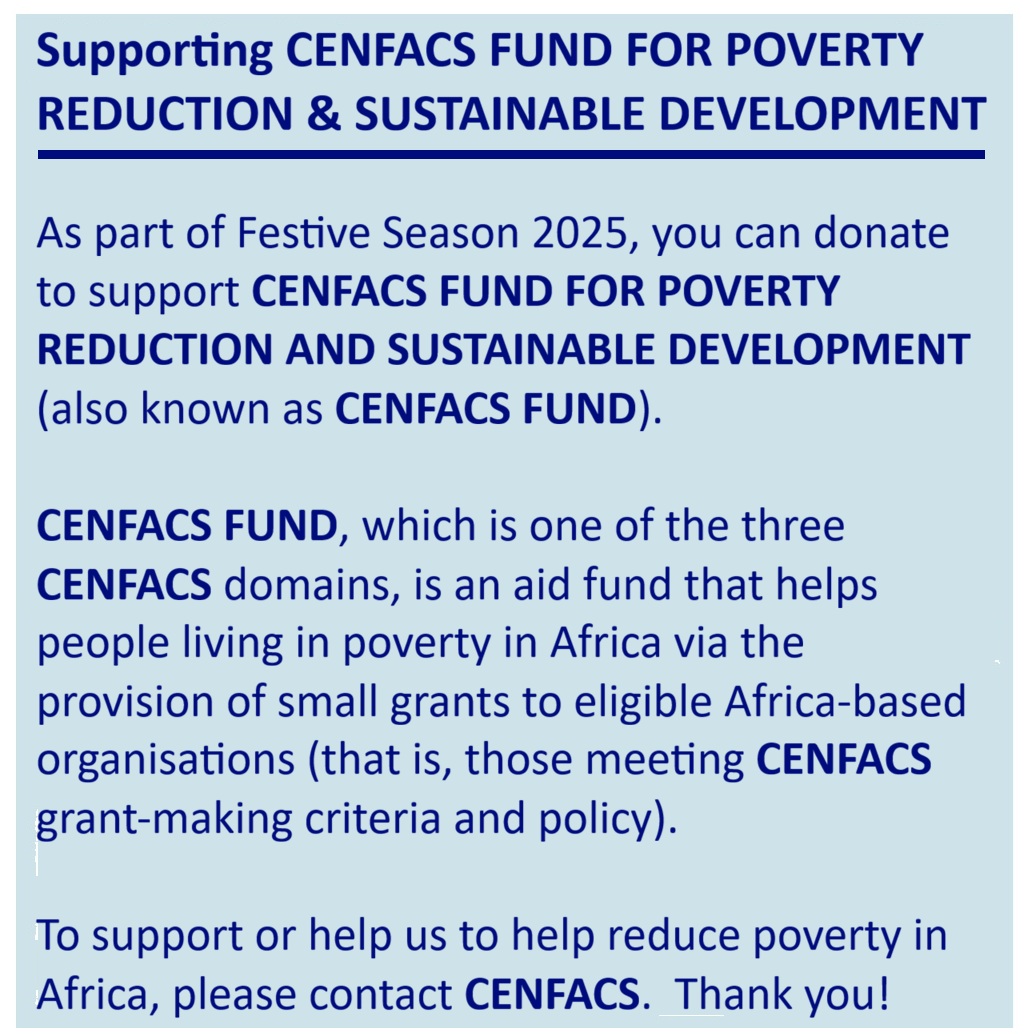

• Help CENFACS Keep the Poverty Relief Work Going This Year

We do our work on a very small budget and on a voluntary basis. Making a donation will show us you value our work and support CENFACS’ work, which is currently offered as a free service.

One could also consider a recurring donation to CENFACS in the future.

Additionally, we would like to inform you that planned gifting is always an option for giving at CENFACS. Likewise, CENFACS accepts matching gifts from companies running a gift-matching programme.

Donate to support CENFACS!

FOR ONLY £1, YOU CAN SUPPORT CENFACS AND CENFACS’ NOBLE AND BEAUTIFUL CAUSES OF POVERTY REDUCTION.

JUST GO TO: Support Causes – (cenfacs.org.uk)

Thank you for visiting CENFACS website and reading this post.

Thank you as well to those who made or make comments about our weekly posts.

We look forward to receiving your regular visits and continuing support until the end of 2026 and beyond.

With many thanks.

_________