Welcome to CENFACS’ Online Diary!

24 September 2025

Post No. 423

The Week’s Contents

• Autumn ‘Fresh Start’ Help, Resources and Setup Services – In Focus for 2025 Edition: Monitoring Economic Indicators

• Campaign to End Poverty Induced by Rising Costs of Living with Long-term Actions

• Act in the Interest of Children’s Education

… And much more!

Key Messages

• Autumn ‘Fresh Start’ Help, Resources and Setup Services – In Focus for 2025 Edition: Monitoring Economic Indicators

To facilitate the reading and understanding of 2025 Edition of Autumn ‘Fresh Start’ Help, Resources and Setup Services, we are going to briefly explain Help, Resources and Setup Services for a Fresh Start as well as the focus for this year’s Fresh Start. Fresh Start and Monitor Economic Indicators are key words and contextual framework of CENFACS‘ Autumn poverty reduction work.

• • Autumn ‘Fresh Start’ Help, Resources and Setup Services

Autumn ‘Fresh Start’ Help, Resources and Setup Services refer to various support programmes and means of solving difficulties experienced by beneficiaries of this support. They are designed to assist CENFACS Community members and sister community members in overcoming significant life challenges such as educational setbacks, out-of-school poverty, threat to homelessness, etc. The specific nature of these Autumnal Help, Resources and Setup Services depend on the given programme and the needs of the applicants.

Fresh Start Help is typically a remedial or relieving action that includes practical assistance, community support, skills development, advocacy, referrals and signposts, and so on to enable applicants to build a more stable and positive future.

Fresh Start Resources consist of:

σ Fresh Start Poverty Reduction Booklet (a guide to reduce autumnal poverty)

σ Fresh Start Accelerator (designed to help those who are lagging behind)

σ Free Resources (i.e., materials to help understand autumnal poverty and find practical ways to overcome it)

σ Poverty Reduction Skills Development.

Fresh Start Setup Services, which are broadly the arranged work to be performed for and on behalf of our users, assist individuals with tasks associated with fresh start Autumn season. They enable to connect people to and prepare our projects and programmes to function according to plan and people’s needs. They contribute to our fresh start services for use by beneficiaries as well as to the implementation and development of what we have planned to deliver as Autumn services for users.

These Fresh Start Help, Resources and Setup Services will assist those at risk of falling under poverty in the Autumn Season. They will provide those in need with strategies for a healthier, happier and thriving life. They come with relief and lasting support while connecting those in need to resources and opportunities for a fresh start from Autumn 2025.

Autumn ‘Fresh Start’ Help, Resources and Setup Services strike or kick off our Autumn programme and Autumn Starting XI Poverty Reduction Campaign. It is our Autumn project striker. Autumn ‘Fresh Start’ Help, Resources and Setup Services are made of fresh start skills, tips, hints, tweaks, hacks, etc.; help, resources and services designed to overcome poverty and hardships. They are indeed activities to turn endings of Summer to new beginnings, to manage new beginnings and plans for the future.

Our advice- and guidance-giving month of September continues as planned and will end next month. Advice- and guidance-giving services are part of our Help, Resources and Setup Services for Autumn Fresh Start. Although we put particular emphasis on advice-giving activity in our September engagement, other aspects of Autumn Fresh Start or striker are equally important and will continue beyond September.

Autumn ‘Fresh Start’ Help, Resources and Setup Services as a project comes with a bundle of Fresh Autumn Start (FAS) Resources and Setup Services. The highlights of the 2025 Edition of FAS, which are given below, take into account and focus on Monitoring Economic Indicators. The resources provided in FAS are non-financial help to understand and follow economic indicators that affect households on their daily life and poverty.

The focus will be on household economic indicators and the help that is available for households/users to follow them. It is also about the resources they can have not only to track these indicators and but also to use the information from this tracking exercise to further reduce poverty. It is further about the services that will facilitate this tracking exercise.

• • Monitoring Economic Indicators as a Focus for This Year’s Autumn ‘Fresh Start’ Help, Resources and Setup Services

This Year’s Autumn ‘Fresh Start’ Help, Resources and Setup Services will be on Household Economy Analysis. They will be about analysing household economies, understanding household vulnerabilities to economic shocks, and informing policy responses and interventions. In other words, we shall assess how households respond to economic changes while getting insights into their economic strategies and vulnerabilities.

To respond to economic shocks, households need to monitor economic indicators that run their lives. Monitoring Economic Indicators involves tracking various statistical measures that help analyse the health, size and direction of a country’s economy. These indicators provide insights into key factors such as production, employment, spending, and prices that influence Gross Domestic Product, inflation, productivity, and economic growth. These indicators can be monitored by households.

Indeed, households do not need to be economists to monitor economic indicators. They do not have to be economists to understand that when the price of food and energy go up, they have to pay more for food and energy, unless they get support for these increases. They can regularly check data on inflation (Consumer Price Index), unemployment rates, consumer confidence, retail sales, interest rate and real household income. These metrics, often available through government statistics websites and financial news outlets, provide insights into the economy’s overall health, the strength of the market, household purchasing power, and financial conditions. They can help households to plan in terms of consumption, investment, educational needs, housing, savings, etc. Even poor households need to track these economic indicators so that they can find way of getting out of poverty.

For instance, rising inflation erodes purchasing power, while declining unemployment signifies a stronger job market.

Monitoring Economic Indicators is basically a process of making it easier or possible – via support and setup services – for CENFACS members and project beneficiaries to track economic indicators on which their life depends. To monitor economic indicators, one may need a plan of action to achieve it.

However, CENFACS does not have the power to change the direction of these indicators (that is inflation rate, unemployment rate, consumer confidence, retail sales, interest rates, etc.). CENFACS can work with its members so that they can better follow these indicators. CENFACS has rather a voice to speak and can help through its voice so that those who can influence the economic factors and indicators (like inflation, interest rate, wages, etc.) do their best so that these factors and indicators do not harm those living in poverty. For instance, advocacy can be done so that they can stabilise prices, improve the welfare system and raise wages to match prices.

There are those of our members who can monitor these economic indicators. There are others who may not be able to track them. For the latter, Autumn ‘Fresh Start’ Help, Resources and Setup Services will assist them to monitor economic indicators and start freshly this Autumn 2025. In this respect, Autumn 2025 ‘Fresh Start’ Help, Resources and Setup Services to Monitor Economic Indicators as a resource contains new information, tips, tools and hints to help the community to better track economic indicators.

So, monitoring economic indicators can help to freshly start or reset or change things or settings. There is a say that every day is a fresh start. In this Autumn of the enduring cost-of-living crisis, fresh start is even more relevant than at any time to restore life. They need to freshly start since they could be still dealing with the lingering socio-economic effects of the cost-of-living crisis.

Further details about the above key words and contextual framework are given below under the Main Development section of this post.

To ask for ‘Fresh Start’ Help and or access ‘Fresh Start’ Resources and Setup Services to Better Monitor Economic Indicators, please work with CENFACS.

• Campaign to End Poverty Induced by Rising Costs of Living through Long-term Actions with a Focus on Aid in Planning for Future Crises

We are continuing with our Campaign to End Poverty Induced by Rising the Costs of Living, which started in October 2022. It is one of CENFACS Autumn Starting XI Poverty Reduction Projects for this this year. This Autumn, the focus for this Campaign is on Aid in Planning for Future Crises. Aid in Planning for Future Crises represents this Campaign on the list of Autumn 2025 Starting XI Poverty Reduction Projects which we released last week.

Before dealing with the focus of this Campaign, let us explain the Campaign itself, poverty attached to the cost of living, Campaign steps or phases, and Campaign actions (which include Aid in Planning for Future Crises).

• • What This Campaign Is about

The Campaign to End Poverty Linked to Rising Costs of Living is an organised series of actions to gain support for the cost-of-living poor so that something can be done for them. These actions need to result in change, particularly the reduction and end of poverty led by the cost-of-living crisis.

The cost-of-living poverty is linked to the fall in living standards. The campaign tries to address the root causes of the cost-of-living crisis. Amongst the causes is the mismatch of highly rising prices and slow wage/income growth of the cost-of-living poor.

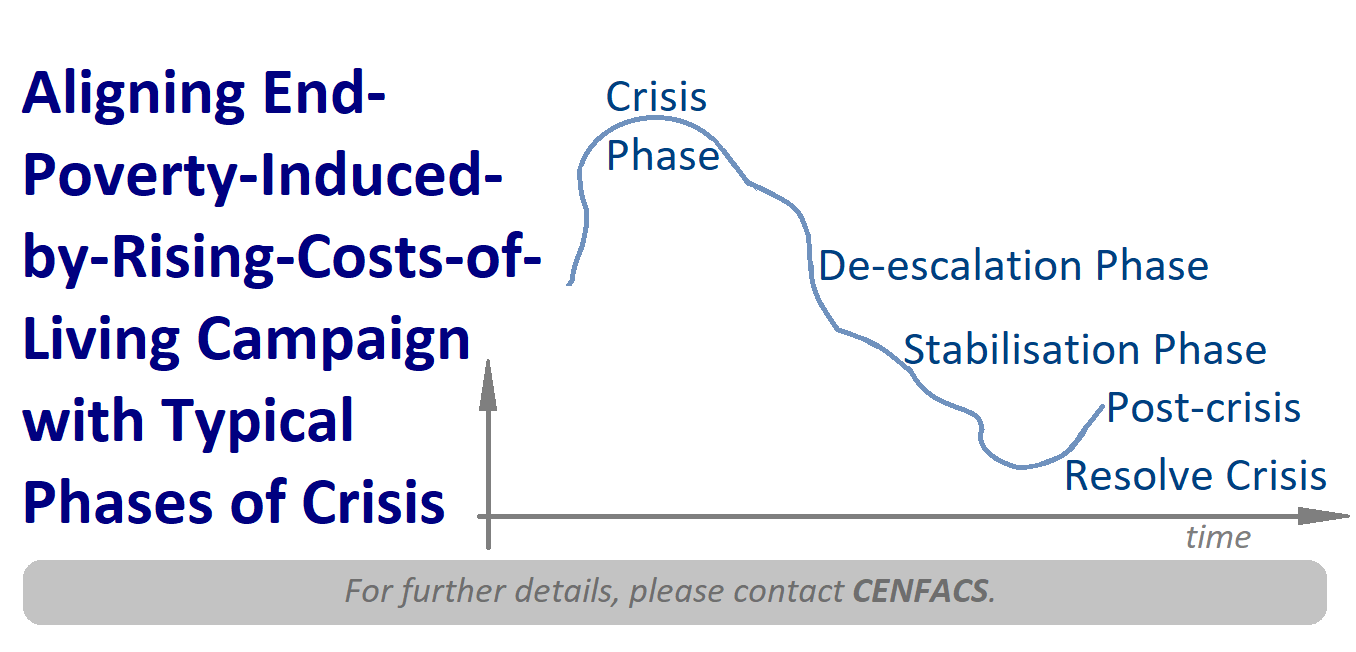

We are continuing our alignment of this campaign with the typical phases of crisis (i.e., crisis, de-escalation, stabilisation, resolve and post-crisis) as it was set up in October 2022.

The cost-of-living crisis is now a barrier for many poor. To tackle this barrier, one may need to understand poverty linked to the cost of living.

• • Basic Understanding of Poverty Attached to the Cost of Living

For anyone to understand poverty due to high costs of living, it is better to define the cost of living. The website ‘ben.org.uk’ (1) defines the cost of living as

“The amount of money needed to cover basic expenses such as housing, food, taxes, and healthcare in a certain place and time period”.

From the above definition, it is possible to argue that those who are poor, because of rising cost of living like at the moment, are those who are failing or totally struggling to meet this rise. The rise includes hikes in energy bills, food prices, taxes, interest rates, rent, fares, etc. In economic parlance, it is the rise of headline inflation (that is, all the changes in the values of things).

In order to deal with this rise, actions need to be taken to support or work with the cost-of-living poor so that they can reduce and eventually end poverty linked to rising costs of living.

Because there are phases or steps in any campaign, campaign actions will be taken according to the phases of our campaign.

• • Phases/Steps in the Campaign to End Poverty Induced by High Costs of Living

Any crisis has some phases or cycle to take or follow. Because of that, our campaign will follow the cycle of a typical crisis. We use the adjective typical because we do not exactly how the cost-of-living crisis will evolve. What we know so far, there has been a crisis (the cost-of-living crisis). And if we use the generic model of this typical crisis, we can guestimate that there will be de-escalation, stabilisation and resolve phases of the current crisis.

In each phase of our model of crisis curve, there will be actions to be taken. However, actions from each phase should not be treated separately without considering actions before and after each phase. This is because there could be communicating vessels between the two phases.

So, the phases or steps of our Campaign to End Poverty Induced by High Costs of Living will be aligned with the above-named phases (i.e., de-escalation, stabilisation and resolve). At the moment, our Campaign is between the crisis phase and the de-escalation phase.

• • Actions or Ways of Working with the Community to Reduce and Possibly to End Poverty Linked to Higher Costs of Living

There are those who believe that to end poverty linked to high costs of living, earnings and incomes or any benefits received by the poor have to be uprated to the rates of inflation. However, CENFACS as a charity does not have the means or power to adjust its members’ incomes or earnings or benefits for inflation. Instead, what CENFACS can do is to work with them in a series of actions or activities so that they can navigate their way out of poverty induced by the cost-of-living crisis. What are these actions or activities?

From this week, we are presenting the long-term actions from this campaign, actions which will start from October 2025. While we are preparing for these long-term campaign actions, we are continuing to offer the other two services (short- and medium-term services) linked to this campaign.

It takes a long time for a crisis like the cost-of-living crisis to end. Normally, this crisis can only end when real household disposable incomes are able to match the level of headline inflation in the economy. Because of that, it is better to have short-, medium- and long-term actions; actions that can stemmed from a strategy to end crisis.

Since it is difficult to know the duration of the cost-of-living crisis, we prefer to have an open strategy or plan which will run for the duration of the crisis. In this open strategy or plan, we can conduct short-, medium- and long-term actions.

Since this campaign was launched in October 2022, we had short-term or immediate actions (from October 2022 to until March 2023) and medium-term actions (from October 2022 to October 2024). At the end of October 2024, medium-term actions were totally covered while we were/are still in the long-term horizon or actions of this campaign.

• • • Long-term Campaign Actions to be taken with the community

On 2 November 2022, we put in place a long-term service or a programme between 2 and 10 years to accompany our community members for the duration of the cost-of-living crisis. The current cost-of-living crisis may not last for 10 years. However, we organised this service because we thought that even if the cost-of-living crisis ends, its effects will be still around for a while. Depending on service beneficiaries’ experience, some of them may need the service, others may not. There is at least a provision or service for the community should anyone needs it.

The aim of this third level of actions is to avoid that the cost-of-living crisis leads to intergenerational poverty; that is the transmission of poverty linked to high cost of living to future generations.

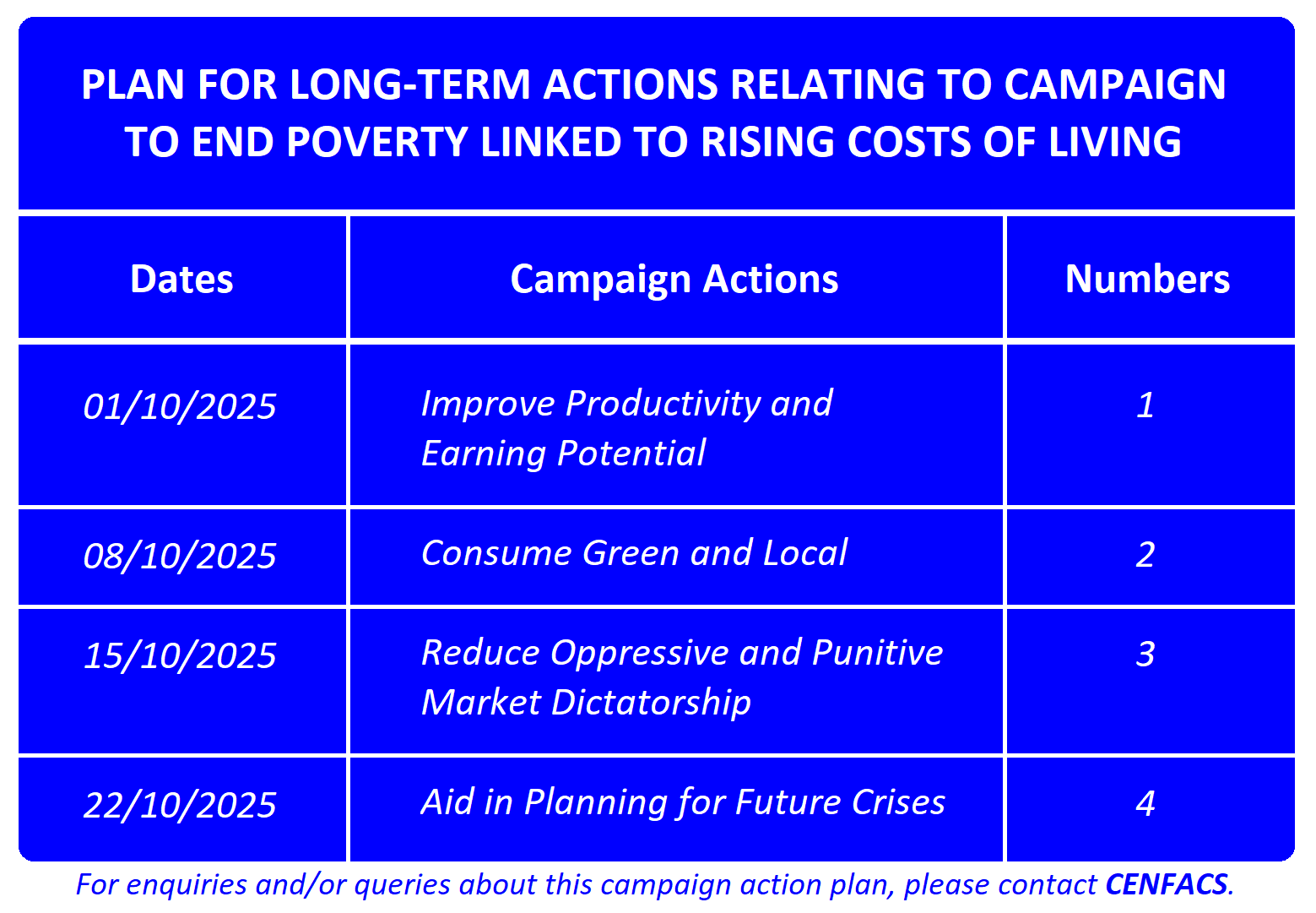

At this level, the long-term actions to be undertaken, actions which go from 2 to 10 years, are those listed below:

σ Help beneficiaries improve their productivity and capacity to earn or generate income

σ Support them to consume green and local so that they are less exposed to the volatility of the international prices of goods and services

σ Find ways of scaling down repressive or punitive market dictatorship on them

σ Aid them in Planning for Future Crises.

Furthermore, the above-mentioned campaign actions are just a selection amongst the ones we hope to take with the community. We will be taking them via what we called ‘GARSIA‘ (that is Guidance, Advice, Referrals, Signposting, Information and Advocacy) services.

Because there are phases or steps in any campaign, these actions will be taken according to the phases of our campaign.

The dates and actions to be taken are given below.

As said above, these actions will be taking via what we called ‘GARSIA‘ (that is Guidance, Advice, Referrals, Signposting, Information and Advocacy) services.

Let us now highlight the campaign action ‘Aid in Planning for Future Crises’.

• • • Aid in Planning for Future Crises as a Focus for Campaign to End Poverty Induced by Rising the Costs of Living

The campaign action about Aid in Planning for Future Crises, which is a specific activity and part of Campaign to End Poverty Induced by Rising the Costs of Living, refers to the support and assistance in the form of awareness raising efforts to plan for future crises. It will consist of working with households in the UK and organisations in Africa to prepare or plan for future crises. The plan with households will consist of building an emergency supply kit, staying informed, practising regularly and support. The plan with organisations in Africa will include crisis preparedness assessment, crisis training, integrated programme design, plan development, and on-call agreements.

The above is the summary of our Campaign to End Poverty Induced by High Costs of Living and of Long-term Actions of This Campaign as well as of the focus for this week. We shall come back on this campaign and its actions from the beginning of this coming October as indicated in the above-given table. To enquire and or support our campaign, please contact CENFACS.

• Act in the Interest of Children’s Education

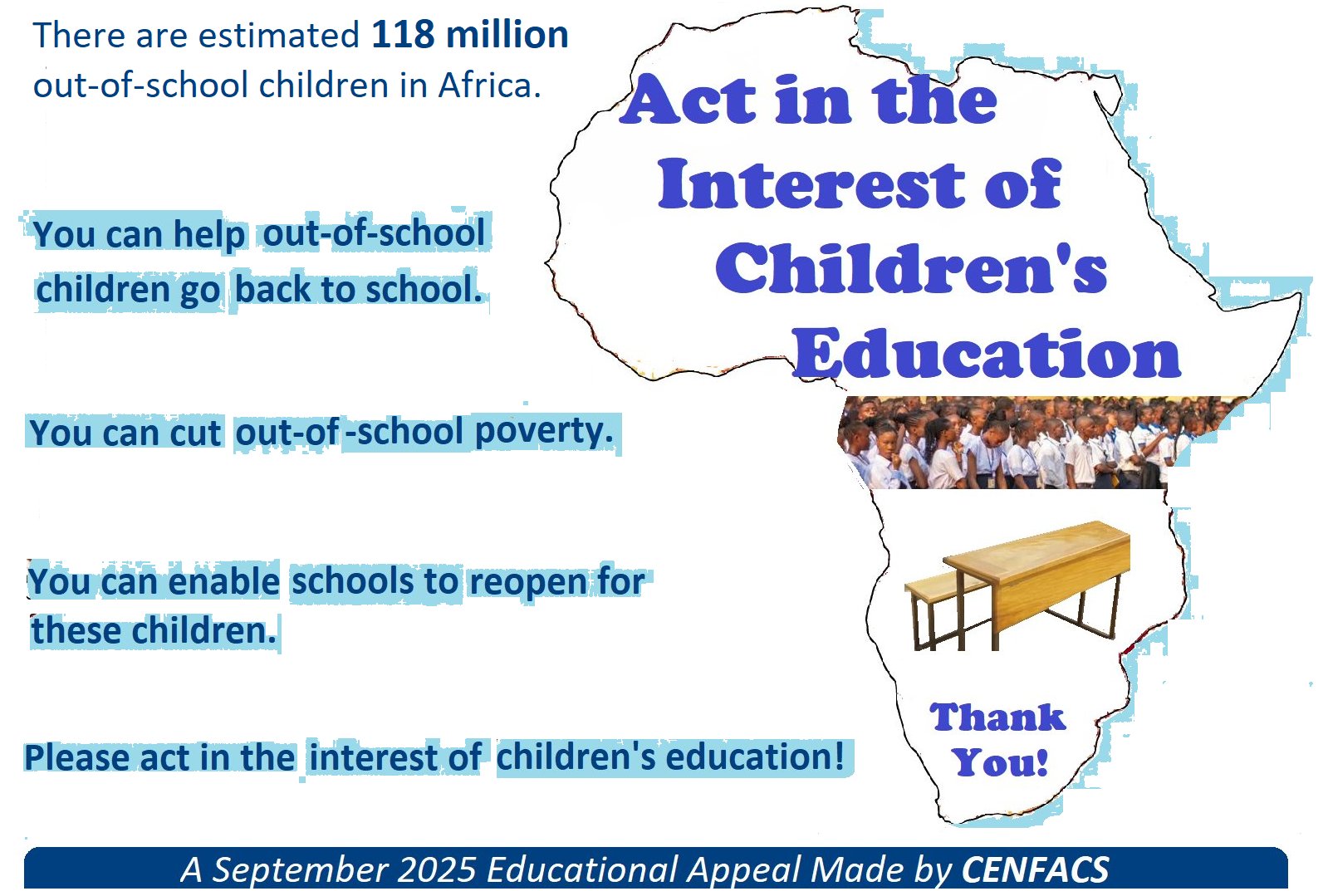

At the moment, in a number of places in Africa, there are children who have not been able to go back to school because of various causes or factors such as conflicts, displacement, natural disasters, economic hardship, and lack of resources.

Calculating the out-of-school rate, the UNESCO Institution for Statistics and Global Education Monitoring Report (2) indicate that

“In 2025 there are estimated 118 million out-of-school children in Africa, with this number having risen since 2015″.

According to the same report, factors contributing to this level of out-of-school children population in Africa include conflicts and crises, fragility, data gaps in conflict zones, funding cuts, gender inequality, rapid population, and poor educational quality.

Similarly, the website ‘humanitarian.org’ (3) explains that

“Africa has the highest out-of-school rates in the world, with over 100 million children and adolescents estimated to be out of school across all sub-regions except North Africa”.

Yet, it is possible reduce the number of out-of-school children in Africa. You can

σ Help out-of-school children to go back to school

σ Reduce out-of-school poverty in Africa

σ Strengthen teacher training in Africa

σ Donate money and / or give in kind or influence for children’s education, protection and security

σ Invest in inclusive education for vulnerable and educationally needy children

σ Enable schools to reopen for these children.

Please do not wait to donate or influence as the needs are pressing and urgent NOW.

To support and or enquire about this out-of-school relief appeal, please contact CENFACS.

Please act in the interest of children’s education in Africa.

Thank you for your generosity.

Extra Messages

• Orange Spaces-focused Note for Week Beginning 25/09/2024: Integration between Orange Spaces and Other Spaces in the Process of Poverty Reduction

• Financial Plan Updates for Households in 2025 – Third Update from Wednesday 24/09/2025: Keeping Household Financial Strategies on Track

• Intergenerational Financial Planning for Families – In Focus from Week Beginning Monday 22/09/2025: Creating a Roadmap for Passing on Wealth

• Orange Spaces-focused Note for Week Beginning 25/09/2024: Integration between Orange Spaces and Other Spaces in the Process of Poverty Reduction

Orange Spaces can be integrated with other spaces (Brown, Grey, Green and Blue Spaces) in the process of reducing poverty and enhancing sustainable development. Before looking at how this integration can help in poverty reduction, let us briefly explain these spaces.

• • Understanding Orange , Brown, Grey, Green and Blue Spaces

Let us start with Orange Space. Within the literature about spaces, Orange Space does not have a standard definition. It refers to areas shown as Orange on a poverty map to represent locations with rising poverty rates or increasing spatial concentrations of deprivation. The existence of Orange Spaces signals areas where economic well-being is worsening and they can be used to identify where new poverty traps are forming or where existing ones are intensifying, influencing urban planning and the provision of resources.

Regarding brown space, also known as brownfield. According to ‘gosolve.co.uk’ (4),

“Brownfield land refers to previously developed sites that have become underutilised or abandoned, often due to changing industrial practice or contamination from former use”.

Adversely, the website ‘eli.org’ (5) argues that there could be benefits deriving from the redevelopment of brown spaces.

Our understanding of grey space comes from Oren Yiftachel (6) who argues that

“The concept of ‘gray space’ refers to developments, enclaves, populations and transactions positioned between the ‘lightness’ of legality/approval/safety and the ‘darkness’ of eviction/destruction/death. Gray spaces are neither integrated nor eliminated, forming pseudo-permanent margins of today’s urban regions, which exist partially outside the gaze of state authorities and city plans” (p. 243)

Our notion of green space is given by what Abigail Isabella McLean (7) argues about it, which is

“Green space refers to the many types of green land, ranging from parks to natural areas. Hence, the green spaces … will encompass naturally occurring green spaces, such as forests, but also space created within human-made means such as green roofs and tree-lined streets”.

As to blue space, its definition comes from what the ‘environmentagency.blog.go.uk’ (8) states about it, which is

“Blue spaces are outdoor environments – either natural or manmade – that permanently feature water and are accessible to people. In short – the collective term of rivers, lakes or the sea”.

The above-mentioned definitions can be served as basis for exploring integration between the five spaces in the process of poverty reduction.

• • Spaces Integration and Poverty Reduction

When looking for ways of reducing poverty, it could be useful to work out how each space (orange, brown, grey, green and blue) can be a more or less contributing factor to poverty reduction. Taking this integrative approach can be worthwhile in judging each of spaces on their own merit.

The merits of green and blue spaces in enhancing health and wellbeing are already known and even undisputable. Those who are suffering from poor health can use the opportunities of green and blue spaces to improve their health.

As grey space provides the bases for self-organisation, negotiation and empowerment; its merit for poverty reduction can depend on its capacity to help people to move from darkness to lightness. This is despite many studies recognise that the development of grey space could result in harmful impact on health and the wellbeing of those living in and around this space.

Concerning brown spaces, Joseph W. Dorsey (9) explains that

“Brownfield initiatives are deeply intertwined with community economic development and job creation, and they are also important aids in health and safety issues, neighbourhood restoration, and the reuse of urban space to counter suburban sprawl into green, open spaces”.

Regarding Orange Space, it can be used as a way to fight poverty and support organisations that work to alleviate it. It can be utilised to reduce or end poverty attached to a group that has been visualised or identified or differentiated as poor in a spatial analysis by orange colour or space. It can be employed in fundraising activities or events to raise money to meet the needs of such group or any other good causes.

It would be useful in search for solutions to poverty to consider the five spaces. For example, Yaella Depietri and Timon McPhearson (10) suggest a hybrid approach which combines blue, green and grey approaches for reducing hazards in the urban context. They argue that

“Cities should rely on a mix of grey, green and blue infrastructure solutions, which balance traditional built infrastructures with more nature-based solutions” (p. 106)

However, they warn against turning easily to grey infrastructures as the default solution.

Writing a note about the above-mentioned integration is not the end of the theme of the Orange Spaces. The real aim here is how CENFACS can work with the communities in the UK and in Africa to empower these communities to use the merits of each space to escape from poverty.

• • Working with Communities to Access the Benefits Provided by Orange , Brown, Grey, Green and Blue Spaces through Their Integration

There are ways of working with communities to make the integration between the Orange , redevelopment of brown, grey, green and blue spaces work for them.

For example, if green and blue spaces can help reduce loneliness and stress, and loneliness and stress are seen as forms of poverty; then CENFACS can work with those members of its community who feel poor because of loneliness in order to alleviate this type of poverty.

Likewise, if the blue space can assist in reducing inequality, then CENFACS can work with those of its members who suffer from inequality, to tackle the matter via for example access to a river, lake, stream, etc.

Additionally, if grey space can be a principle on which an agreement can be based or made, we can work with those members of our community who are suffering from the effects of grey space to engage grey space to negotiate while empowering them.

As to brown space, after the clean-up process, there is a need to ensure that the Redevelopment of Brown Spaces does not bring injuries, liabilities or additional hazards. It does not pose any health and safety risks to the community.

Concerning Orange Space, it can be used to acknowledge the interconnectedness of issues whereby environmental, social and economic issues are connected and tackled together to end poverty sustainably.

In short, if one of our members needs orange, brown, grey, blue or green prescription; we can work with them on this matter through advice, information, guidance, signposting and social prescribing.

The above is our last note about the theme of Orange Space which we hope you have enjoyed and has added value to what you know about it. We also expect that through this theme, one will be able to approach Orange Space as a Campaign Theme to Reduce Poverty and as a Tool to Enhance Sustainable Development.

Saying that the above is our last note does not mean that we stopped working on Orange space or framework. We are still working on it even though we will not produce any further note for the rest of the days of September 2025. We are continuing with spatial analysis of poverty as well as the orange, brown, grey, green and blue frameworks to analyse poverty reduction and sustainable development.

For those who would like more information about any of the notes developed throughout this month about Orange spaces as well as those who need an orange, brown, grey, blue or green prescription; they are free to contact CENFACS.

For those who would like to support the theme of Orange Spaces and our work on poverty reduction using an integrative approach to space or spatial analysis, they should not hesitate to contact CENFACS with their support.

• Financial Plan Updates for Households in 2025 – Third Update from Wednesday 24/09/2025: Keeping Household Financial Strategies on Track

In order to keep household financial strategies on track, it is better to understand these strategies.

• • What Are Financial Strategies?

There are various definitions of financial strategies. In the context of these updates, let us refer to what ‘wallstreetmojo.com’ (11) argues about them, which is

“Financial strategies refer to the comprehensive plans and approaches that individuals, businesses, or organisations adopt to manage their financial resources effectively. These strategies encompass a wide range of activities, including budgeting, investment planning, debt management, risk mitigation, and overall financial decision-making”.

Households (that is, a person or people living together in the same dwelling who share meals or joint provision of living conditions) can adopt the plans and approaches to manage their financial resources without necessarily having to behave like business organisations.

• • How Households Can Keep Their Financial Strategies on Track

To keep their financial strategies on track, households can proceed with the following:

σ Regularly track and monitor their expenses

σ Review and check the bills

σ Set savings goals

σ Engage all household members in the budgeting process

σ Adjust the budget as needed.

Households can use the above-mentioned financial strategies to effectively manage their finances. They can keep track of their finances manually or using a personal finance app that fits their needs. There is a number of apps on the market (like Quicken, Personal Capital, You Need a Budget, etc.) that can help track and analyse household expenses. They need to adhere to money management tips, as well.

• • Working with CENFACS Community Members on Keeping Household Financial Strategies on Track via a Weekend Homework for Households

As a way of supporting this week’s topic relating to Keeping Household Financial Strategies on Track, we are asking to those who can to conduct this weekend homework activity:

Select a personal finance app or your bank app from your mobile phone to track, tabulate and analyse your expenses.

Those who may have some questions about this activity, they should not hesitate to contact CENFACS.

Those who may be interested in the Keeping Household Financial Strategies on Track can contact CENFACS for further details.

If you need support with your Financial Plan Updates or for us to look at your Financial Plan, please do not hesitate to communicate with CENFACS.

• Intergenerational Financial Planning for Families – In Focus from Week Beginning Monday 22/09/2025: Creating a Roadmap for Passing on Wealth

In order to introduce this topic, let us first explain roadmap and wealth, then deal with this roadmap in transferring wealth,

• • What Is a Roadmap?

According to ‘roadmunk.com’ (12),

“The basic definition of roadmap is simple: It’s a visual way to quickly communicate a plan or strategy”.

The literature about roadmap goes further by explaining that it is a visual plan that outlines the steps needed to achieve specific goals over time. It serves as a strategic planning tool that communicates a project’s goals and major deliverables on a timeline, helping to organise strategies and tasks while connecting them to larger objectives.

So, to transfer family wealth there is a need to create a roadmap, that is a visual plan that outlines steps needed to achieve the goals of this transfer.

• • What Is Wealth?

There are many ways of defining wealth or family wealth. According to ‘ffpractitioner.org’ (13),

“Family wealth is how each family defines its wealth and that is more important than the definitions of others”.

The same ‘ffpractioner.org’ cite James E. Hughes Jr. in his book Family Wealth, who defines the wealth of a family as “the human and intellectual capital of the family, with financial capital being used to support the growth of the family’s human and intellectual capital”.

In our work with families, the focus is/will be on family financial capital that can be transferred to others by will or by law. In particular, the focus is/will be on ‘Family Financial Balance Sheet’.

We do not undermine the value of family human and intellectual capital as well as social capital. Also, we do not underestimate the contributions of parents, grandparents and their successors in terms of their legacy and influence. Family human capital and social capital are all valuable assets to be transferred as part of heritage or inheritance. Unfortunately, in the context of this topic we are mostly dealing with the transfer of physical and monetary assets.

Knowing what is roadmap and what is family wealth, we can know speak about how a family can create a financial roadmap to passing on wealth.

• • Creating a Financial Roadmap for Passing on Wealth

It involves a structured approach to managing and transferring wealth across generations. To create a roadmap for transferring family wealth, one needs

σ To assess what the family financially stands

σ To determine what you want to achieve

σ To establish how you will achieve family transfer wealth goals.

There are guides in terms of steps to follow in order to create a roadmap for passing on wealth.

For instance, the website ‘allwealth.com’ (14) provides a step-by-step Guide which consists of 9 steps as follows:

1) Define your financial goals 2) Assess your current financial situation 3) Create a budget 4) Build an emergency budget 5) Reduce debt 6) Save and invest 7) Protect your assets 8) Continuously monitor and adjust 9) Seek professional advice.

By following these steps or any professional ones, families (that is, a group of people related by blood or marriage such as parents and their children only) can create a roadmap that can passes on wealth and ensures it is wisely managed for future generations.

We can work with families making the CENFACS Community and those from sister communities to help them find ways of Creating a Financial Roadmap for Passing on Wealth. We can work with them to assess their financial position, define their financial goals, establish family governance structure, communicate and update their legal documents, review and adjust their wealth transfer plan.

• • Working with CENFACS Community Members on Creating a Financial Roadmap for Passing on Wealth via a Weekend Homework for Families

As a way of supporting this week’s topic relating to Creating a Financial Roadmap for Passing on Wealth, we are asking to those who can to conduct this weekend homework activity:

Define your financial goals by determining whether you prioritise education, property, or retirement security.

Those who may have some questions about this activity, they should not hesitate to contact CENFACS.

Those who would like to know more about Creating a Financial Roadmap for Passing on Wealth and to work with CENFACS, they can contact us.

Similarly, those who may be interested in Intergenerational Financial Planning or in discussing any matter relating to the topic of Creating a Financial Roadmap for Passing on Wealth, they should feel free to contact CENFACS. Equally, those who would like to tackle intergenerational poverty can communicate with CENFACS.

Message in English-French (Message en Anglais-Français)

• CENFACS’ be.Africa Forum E-discusses Economic Sovereignty and Poverty Reduction in Africa

Economic sovereignty can enable nations to control their resources and shape their own development paths, rather than being constrained by external factors like foreign aid and conditionality that perpetuate dependency and undermine effective governance.

Building economic sovereignty involves fostering self-reliance through initiatives such as food sovereignty and investing in knowledge and digital infrastructure, which are essential to address the unique challenges of poverty reduction in Africa and avoid perpetuating its role as a source of raw materials and a marketplace for foreign goods.

Although there are challenges and hurdles in the pathways to economic sovereignty, the latter can help Africa to further reduce poverty as well as to achieve the kind of poverty reduction Africa would like to have. These challenges and hurdles to economic sovereignty make up the contents of this week’s e-discussion within CENFACS’ be. Africa Forum. We are e-discussing the extent to which the increase in economic sovereignty can open up the possibilities for further poverty reduction in Africa.

For instance, we can e-discuss whether the recent international and foreign aid cuts have boosted economic sovereignty and opportunities for Africa to further reduce poverty on its own terms or not. On the contrary, Africa has replaced cut aid with different types of aid or donors which still make economic sovereignty challenging and within the hands of new donors.

Those who may be interested in this discussion can join our poverty reduction pundits and/or contribute by contacting CENFACS’ be.Africa Forum, which is a forum for discussion on poverty reduction and sustainable development issues in Africa and which acts on behalf of its members by making proposals or ideas for actions for a better Africa.

To contact CENFACS about this discussion, please use our usual contact address on this website.

• Le Forum ‘Une Afrique Meilleure’ de CENFACS discute en ligne des Souverainetés Économiques et de la Réduction de la Pauvreté en Afrique.

La souveraineté économique peut permettre aux nations de contrôler leurs ressources et de façonner leurs propres chemins de développement, plutôt que d’être contraintes par des facteurs externes tels que l’aide étrangère et la conditionnalité qui perpétuent la dépendance et nuisent à une gouvernance efficace.

Construire la souveraineté économique implique de favoriser l’autonomie grâce à des initiatives telles que la souveraineté alimentaire et l’investissement dans les connaissances et l’infrastructure numérique, qui sont essentielles pour relever les défis uniques de la réduction de la pauvreté en Afrique et éviter de perpétuer son rôle de source de matières premières et de marché pour les biens étrangers.

Bien qu’il existe des défis et des obstacles sur les voies de la souveraineté économique, cette dernière peut aider l’Afrique à réduire davantage la pauvreté ainsi qu’à atteindre le type de réduction de la pauvreté que l’Afrique souhaite avoir. Ces défis et obstacles à la souveraineté économique constituent le contenu de la discussion en ligne de cette semaine au sein du Forum ‘Une Afrique Meilleure’ de CENFACS. Nous discutons en ligne dans quelle mesure l’augmentation de la souveraineté économique peut ouvrir des possibilités pour une réduction supplémentaire de la pauvreté en Afrique.

Par exemple, nous pouvons discuter en ligne si les récentes coupes dans l’aide internationale et étrangère ont renforcé la souveraineté économique et les opportunités pour l’Afrique de réduire davantage la pauvreté selon ses propres conditions ou non. Au contraire, l’Afrique a remplacé l’aide réduite par différents types d’aide ou de donateurs/rices, ce qui rend toujours la souveraineté économique difficile et entre les mains de nouveaux donateurs/rices.

Ceux ou celles qui pourraient être intéressé(e)s par cette discussion peuvent se joindre à nos experts en réduction de la pauvreté et/ou contribuer en contactant le ‘me.Afrique’ du CENFACS (ou le Forum ‘Une Afrique Meilleure’ de CENFACS), qui est un forum de discussion sur les questions de réduction de la pauvreté et de développement durable en Afrique et qui agit au nom de ses membres en faisant des propositions ou des idées d’actions pour une Afrique meilleure.

Pour contacter le CENFACS au sujet de cette discussion, veuillez utiliser nos coordonnées habituelles sur ce site Web.

Main Development

• Autumn ‘Fresh Start’ Help, Resources and Setup Services – In Focus for 2025 Edition: Monitoring Economic Indicators

The following two items cover the presentation of Autumn ‘Fresh Start’ Help, Resources and Setup Services:

∝ Making Autumn Start and Season Easier

∝ Key Summaries of FAS 2025 Edition.

Let us look at these items.

• • Making Autumn Start and Season Easier

In order to make Autumn Start and Season Easier it is better to understand Fresh Autumn Start and its context.

• • • What is Fresh Autumn Start (FAS)

FAS is a continuation of our Summer Support projects into the Autumn season. It is a building block or additional handy back up of useful survival tips and hints to embrace Autumn as smoothly and trouble-freely as possible.

It includes real life situations that users may face when and as they return from their Summer break or season on one hand, and possible leads to proffer solutions to their arising Autumn needs on the other hand.

This FAS resource is not exhaustive or an end itself. It needs other resources as complement. It is a good basic insight into a Fresh Start as it provides helpful advisory tools for a Fresh Start and confidence building from the beginning to the end of Autumn season. It could also be used as a reference for users to engineer their own idea of Fresh Start and the sustained management of autumn needs.

At the end of this resource, there are some websites addresses/directories for help and support. In this post, we have not included these websites addresses/directories. Those who would be interested in them, they need to request them from CENFACS. These sources of help and support are not exhaustive. We have mainly considered third sector organisations and service providers as well as social enterprises.

For further or extended list of service providers for Autumn needs, people can contact their local authorities and service directories (both online and in print).

• • • Fresh Autumn Start in the Context of Slow Rising Costs of Living

This Autumn, we are approaching Fresh Start Help from the perspective and context of Rising Prices at a slower pace or rate. It is the context in which prices of goods and services are slowly rising and sometimes going up and down in a sinusoidal way. Although inflation has eased, its cumulative effect is still felt, and households still face significantly higher costs. Low incomes are not still in position to catch up with slow rising costs or prices.

It is still the context of cost-of-living crisis since real household disposable incomes have not really increased since inflation is out of reach of the UK Government target of 2%. In this typical context, the most sufferers are those living in poverty as they cannot afford any rising prices and bills whether they are small or slow.

A context like the one we have depicted needs a response so that our users and members can meet their needs and navigate their way out of the cost-of-living crisis and poverty. Our users and members need help and support to improve the ways they are tackling the enduring cost-of-living crisis. Our users and members would like to see the end of higher living costs happening. They would like also to monitor economic indicators that affect their life. We can work with them so as they can get the help they need in order to monitor these indicators and meet their basic life-sustaining needs and requests.

Briefly speaking, Fresh Start Help is the first line of support we are providing in the process of monitoring economic indicators as well as ending higher living costs or their impact. The second line of support is Fresh Start Resources and Setup Services.

• • Key Summaries of FAS 2025 Edition

The key summaries of FAS 2025 Edition can be found under the contents below.

• • • Contents for FAS 2025 Edition

The contents for 2025 Edition of FAS include:

∝ Autumn scenarios and actions to take

∝ Examples of Summer break expenses track record and Autumn budget

∝ People needs and Autumn leads

∝ Integration of threats and risks

∝ Monitoring economic indicators

∝ What you can get from CENFACS

∝ Autumn online and digital resources.

Let us briefly explain each of these contents.

• • • • Imaginable Autumn Scenarios and Possible Actions

When returning from Summer break and/or season, people can find themselves in a variety of situations depending on their own individual circumstances and life experiences. This variety of situations may require or be expected to be matched with a diversity of responses in order to meet people’s Autumn needs.

These variable circumstances and diverse responses or a course of actions can take the different shapes as well as can be framed in order to take into account the continuing adverse impacts of the enduring cost-of-living crisis. One of these shapes could be to contextualise and customise back-to-relief, fresh start and build-forward-better support. This is what CENFACS tries to do via the advice service.

• • • • Examples of Summer Break Expenses Track Record and Autumn Budget

Tracking down and reassessing summer break/season expenses are a positive step to put one through an optimistic start of the Autumn season. As part of this positive step, FAS is packed with an example of Summer Break Expenses Track Record.

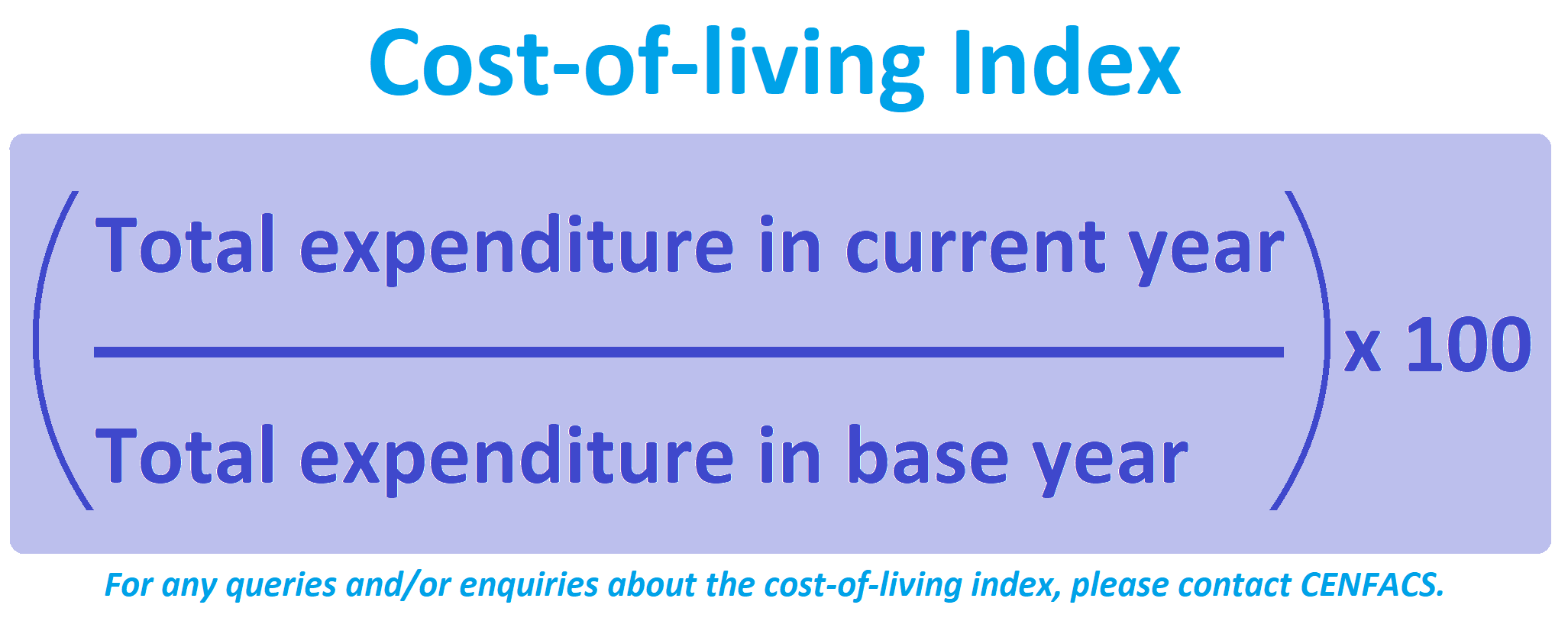

Budgeting Autumn items and needs is also good for a Fresh Start and for overall control over the start and rest of autumn season expenses. Since our focus is on ending higher living costs via the monitoring of economic indicators, one can write a budget that deals with the shape and direction of the rise of the costs of living.

To write a comprehensive budget, one needs to include in their budget possible projections or forecasting or even scenarios regarding key indicators or adjustment factors like interest rate, inflation, indexes of goods and services, etc. Such a budget will help in costing the activities planned in the process of improving ways and coming out of the cost-of-living crisis.

One of the precautions to take in your Autumn budget is to check affordability of your budget. In other words, you need to make sure that any budgeted outgoings match budgeted incomings, any actual outgoings balance with actual income. A positive difference means your budget is affordable, while a negative one signifies it is unaffordable.

To support this financial control, FAS contains two examples of budgets: Autumn budget adjusted for the cost-of-living index and fresh start budget.

• • • • People’s Needs and Autumn Leads

Variable circumstances can obviously result in multiple needs. One of these circumstances is the enduring cost-of-living crisis. To meet those needs, we may have to gather resources, tools and institutions to guide us. The 2025 Edition of FAS provides a table that gives an idea of the likely leads to satisfy people’s needs or just to guide them.

• • • • Integrating Threats and Risks from the Adverse Impacts of Various Factors into FAS

The FAS 2025 Edition integrates the damaging impacts of economic factors or variables such as interest rate change, inflation, the cost-of-living index, policy changes, geo-economic tensions, etc.

It also considers the probable evolution of these factors or variables in the medium term. Likewise, the probable adverse impacts of climate change are nevertheless taking into account and unavoidable.

This integration is at the levels of possible Autumn scenarios, Autumn budget and arising needs. It is the integration of both life-sustaining needs and other factors (like economic, social, climate, geo-economic, etc).

• • • • Monitoring Economic Indicators

Households cam monitor economic indicators by regularly checking data on inflation (Consumer Price Index), unemployment rates, consumer confidence, retails sales, interest rates, real household income, etc. These metrics, which are often available through government statistics websites and financial news outlets, provide insight into the economy’s overall health, the strength of the job market, household purchasing power, and financial conditions.

Before providing the key indicators to be monitored by households, let us briefly explain household economic indicators.

• • • • • What are household economic indicators?

They are data points that provide insights into the economic status of households, helping to understand their financial well-being and stability. They cover various areas or aspects of household life, such as income and wealth, spending and consumption, stability and confidence.

Regarding income and wealth, these three economic indicators can be mentioned:

σ Real Household Disposable Income (that is, income available for spending and saving after taxes and transfers)

σ Financial Net Worth (equals households’ total assets minus liabilities)

σ Households’ Indebtedness (expresses as the level of debt households hold).

Concerning spending and consumption, the economic indicators to be used can be:

σ Real Household Expenditure (which is the amount households spend on goods and services)

σ Consumer Price Index (measures inflation by tracking the cost of a basket of consumer goods and services).

With respect to stability and confidence, these two economic indicators can be utilised:

σ Consumer Confidence (is a measure of optimism about the economy)

σ Unemployment Rate (indicates the percentage of the labour force that is unemployed but looking for work).

Households need to track the above-mentioned indicators as well as the key indicators given below.

• • • • • Key indicators to be monitoring by households

Households can follow the news and information about the state, performance and evolution (or trends) about the key economic indicators below.

σ Inflation rate (Consumer Price Index): Measures the general increases in prices for goods and services, impacting the costs of living and household budgets;

σ Unemployment rate: The percentage of people actively looking for work indicates the health of the labour market and influences consumer spending;

σ Consumer confidence: A sentiment indicator that reflects how optimistic consumers are about the economy, which can influence their spending habits;

σ Retail sales: Measures the total sales of consumer goods, showing how much money households are spending on various products;

σ Interest rates: The cost of borrowing money, which affects mortgage payments, car loans, and credit card debt;

σ Real household income: This indicator shows how much household income increases after adjusting for inflation, providing a true measure of purchasing power;

σ Household consumption expenditure: Tracks the total amount of money households spend on goods and services as a key driver of economic activity.

• • • • • Where households can find economic data

Households can find the above-mentioned indicators or economic data from the following sources:

Government Statistics Websites (e.g., the Office for National Statistics), Financial News Outlets, International Organisations (e.g., Organisation for Economic Cooperation and Development), Non-profit Organisations and Universities, Specialised Economic Databases (e.g., Economist Intelligence Unit), etc.

For instance, ‘paydata.co.uk’ (15) reported on 18 September 2025 that

“The Consumer Prices Index rose by 3.8% in the 12 months to August 2025, unchanged from July;

The UK employment rate for people aged 16 to 64 years was estimated at 75.2% in May to July 2025;

The UK unemployment rate for people aged 16 years and over was estimated at 4.7% in May to July 2025;

The estimated number of vacancies in the UK fell by 10,000 (1.4%) on the quarter to 728,000, in June to August 2025″.

Likewise, speaking about Consumer Confidence, ‘brc,org.uk’ (16) indicates that

“According to BRC-Opinium data, consumer expectations over the next three months of:

# the state of the economy worsened to -36 in September, down from -32 in August

# their personal financial situation slightly worsened to -7 in September, down from -6 in August

# their personal spending in retail rose slightly to +5 in September, up from +4 in August

# their personal spending overall fell slightly to +14 in September, down from +16 in August

# their personal saving fell to 0 in August, down from +2 in September”.

Regarding Retail Sales as an economic indicator to be monitored by households, the Office for National Statistics (17) states that

“Sales volumes fell by 0.1% in the three months to August 2025, compared with the three months to May 2025. This was a slowing in the rate of decline when compared with the 0.6% fall in the three months to July 2025. August 2025 marks the third consecutive period of monthly growth, but volumes did not quite return to their recent March 2025 peak. However, when comparing with the three months to August 2024, sales volumes rose by 0.8%”.

Concerning Interest Rate, the Bank of England (18) argues that

“The interest rate in the UK as of September 2025 is 4%”.

As to Real Household Income, the Office for National Statistics (19) notes that

“As of September 2025, the Minimum Income Standard (MIS) in the UK requires a single person to earn £30,500 annually to meet a minimum acceptable standard of living. For a couple with two children, the required income is £74,000 annually. This indicates the economic challenges many households face, as income from work and benefits often fall short of these figures”.

Also, one needs to adjust the two figures of £30,500 and £74,000 for inflation, which is 3.8%. If one adjusts the figure of £30,500 for 3.8% inflation, this figure will become: £30,500 – (£30,500 x 3.8%) = £29,341

As far as Household Consumption Expenditure is concerned, ‘nimblefins.co.uk’ (20) estimates that

“In mid 2025, the average UK household budget is around £2,900 a month (or £34,500 a year) based on an average of 2.3 people per household. according to our [Nimblefins] analysis of ONS Family Spending data. But your housing situation can mean you spend a lot more or less… The average UK household spends £2,873 a month on household bills, according to the average (and unlikely!) household size of 2.3 people”.

The above-mentioned figures provide some state of the economic indicators which impact households life. They also tell us where to find them. However, there is also the need to know why to monitor them.

• • • • • Why households need to monitor economic indicators

Households should monitor economic indicators to inform their financial decisions, understand their personal economic well-being, and anticipate future economic trends. By tracking indicators like inflation, unemployment, and household income, households can make better choices about spending, saving, and investing. This can lead them to a greater financial security and a more informed approach to economically managing their households.

Let us consider the monitoring reasons relating to making informed decisions, understanding household personal economic well-being, and anticipating future trends.

a) Monitoring reasons relating to informed decision-making

Under this heading, we can include spending and saving, investment strategies, and debt management. Let us look at each of them.

~ Spending and saving

Monitoring indicators like consumer confidence and household disposable income can help households decide when it is best to make large purchases, save for the future, or adjust their overall spending habits.

~ Investment strategies

Understanding leading economic indicators can provide a sense of where the economy is heading. This will allow households to adjust their investment portfolios to align with future economic conditions.

~ Debt management

Tracking household indebtedness and financial net worth helps households understand their overall financial risk and make more informed decisions about taking on new debt or managing existing loans.

b) Monitoring reasons relating to understanding economic well-being

Under this heading, we can consider assessing personal finances and the evaluation of job market. Let us briefly explain each of these sub-headings.

~ Assessing personal finances

Indicators such as real household income, consumption expenditure, and the household savings rate provide a direct picture of an individual household’s economic situation and well-being.

~ Evaluating the job market

The unemployment rate and labour underutilisation rate are crucial for understanding job prospects and the overall health of the labour market, which directly impacts household income and stability.

c) Monitoring reasons relating to the anticipation of future trends

Under this heading, we can highlight these two reasons: forecasting economic direction and adapting to change.

~ Forecasting economic direction

Leading economic indicators can provide clues about the future direction of the economy, giving households an early warning of potential downturns or upturns.

~ Adapting to change

By staying informed about economic trends, households can adapt their personal strategies to better navigate potential changes in economic conditions, helping them prepare for unforeseen challenges.

• • • What You Can Get from CENFACS in Autumn under Autumn Help to Monitor Economic Indicators

The set of helps provided in the FAS 2025 is part of CENFACS’ UK arm of services and additional services we set up to overcome the negative side effects of crises and risks (like the coronavirus, the cost-of-living crisis, climate crisis, etc.). In this respect, FAS 2025 include ‘Fresh Start‘ activities or services that can be aligned with the typical phases of crisis after the crisis phase. These typical phases include de-escalation, stabilisation, post-crisis and resolve phases.

Because the focus of FAS 2025 is on Monitoring Economic Indicators, the activities we are going to undertake are those relating to those indicators. What are these activities?

There are three activities we would like to mention, which are:

a) activities relating to monitoring economic indicators that are essential for policy making, investment and analysis

b) activities relating to monitoring economic indicators that are vital for understanding household situation

c) activities relating to monitoring economic indicators that can be carried out by households.

Let us look at these activities.

• • • • Fresh Start Activities relating to monitoring economic indicators that are essential for policy making, investment and analysis

These activities are essential for policymakers, investors and analysts to assess economic performance and make informed decisions. They help in identifying economic cycles, allowing for proactive measures rather than reactive ones.

Among these activities, we can mention the following:

σ Economic surveillance, which involves the monitoring and analysis of economic developments and policies, producing cross-country analysis, and country-specific reports.

σ Economic monitoring, which includes systematic analysis of economic developments and prospect, providing insights into the evolution of foreign direct investment, fiscal and monetary policies, and the impact of global events like the war in Ukraine.

σ Tracking economic indicators, which involves the systematic monitoring and analysis of diverse economic variables, including leading, lagging, and coincident indicators, to gauge future trends and evaluate conditions.

σ Comprehensive guide to economic indicators

σ Monitoring of economic indicators in the context of financial and economic crises

σ Understanding key metrics

etc.

Because these activities are mostly designed for policymakers, investors and analysts; we are not going to undertake them with our community members unless they express the desire to work with us on them.

• • • • Fresh Start Activities relating to monitoring economic indicators that are vital for understanding household situation

As highlighted in their title, these activities are vital for households to understand their economic situation and to make informed decisions about their financial well-being. They aim to assess the economic well-being and health of individual households. They also play a significant role in the broader context of economic policy and development.

Among the fresh start activities relating to this second category, we can mention the following ones:

σ Conducting household surveys

These surveys aim to gather data on various aspects of household life, such as employment, income, consumption, and savings. They are essential for understanding household economic security and can be used to identify vulnerable groups for different programmes.

σ Analysing household economic security

There is a method used to identify household level economic security, which is called HES (Household Economic Security) 4 Step Assessment and Analysis Process. It involves data collection and analyse steps to determine household food security, basic needs, and livelihood needs, as well as risks.

σ Monitoring local economic indicators

These indicators reflect the economic health of a specific geographic area and include employment rates, household income, and business activity.

We shall conduct of some of these activities in the context of project planning and development with households making the CENFACS Community.

• • • • Fresh Start Activities relating to monitoring economic indicators that can be carried out by households

As their title suggests, these activities are essential for households to stay informed about their economic situation and to make informed decisions about their resources and strategies. They can as well play a significative role in the larger process of economic decision-making and policy formation.

They include:

σ Assessing household food, income, and expenditures

This involves evaluating the resources available to household and their ability to meet basic needs.

σ Identifying and classifying coping strategies

Households may develop different strategies to cope with economic challenges, and these can be classified based on their effectiveness and impact.

σ Identifying the most affected and vulnerable households

This includes recognizing those who are most impacted by economic changes and their specific needs.

σ Assessing how households vulnerability affects in different ways

Understanding the various ways in household vulnerability can manifest can help in developing targeted interventions.

σ Assessing markets functioning and prices

This involves collecting market information and analysing it to understand the economic environment and potential impacts on households.

σ Identifying the gap in livelihood needs

By analysing the needs of different households, it is possible to identify areas where additional support or resources are required.

We shall work with the households making the CENFACS Community and our sister communities on this third type of fresh start activities so that they can reduce poverty linked to the lack of or poor monitoring of economic indicators. Yet, a good monitoring of these indicators can help them to better analyse their household economy and further reduce poverty.

We shall work with them via Household Economy Monitoring Support (HEMS) which is our new autumnal service. HEMS refers to tools that can be used to understand how households making the CENFACS Community access essential life sustaining resources, monitor household economic security, assess vulnerability to shocks and crises, while informing policy and interventions.

Besides the above-mentioned provision, FAS 2025 Edition further takes into account specific needs of people that may require specialist organisations and or institutions to deal with them. In which case CENFACS can signpost or refer the applicants to those third parties.

• • • Autumn Online and Digital Resources

As explained earlier, FAS 2025 Edition contains a list of organisations and services that can help users in different areas covering basic needs. Most the provided resources, which are from the charity and voluntary sector, are online and digital. The list, which is not in this post, gives their contact details including the kinds of support or service they provide.

We hope that the basic tips and hints making the contents of FAS 2025 Edition will help you in some aspects of your Autumn needs, and you will find the relief you are looking for.

We would like to take this opportunity of the beginning of the new season to wish you a Happy and Healthy Autumn, as well as good luck in your efforts to Monitor Economic Indicators.

_________

• References

(1) https://www.ben.org.uk/how-we-help/for-me/articles/reduce-your-living-costs/ (accessed in September 2024)

(2) UNESCO Institution for Statistics & Global Education Monitoring Report: SDG4 Scorecard Progress Report on National Benchmarks Focus on the Out-of-school Rate available at bit.ly/sdg4scoreand2025 underinvestment; https://www.facebook.com/gemreportunesco/posts/-african-countries-have-pledged-to-reduce-their-out-of-school-population-by-58-m/1155537449949597/ (accessed in September 2025)

(3) https://www.humanitarian.org/en/millions-of-children-at-risk-of-missing-school-as-the-2025-academic-year-begins/ (accessed in September 2025)

(4) https://www.gosolve.co.uk/brown-grey-green-field-land-development (accessed in September 2024)

(5) https://www.eli.org/brownfields-program/brownfields-basics# (accessed in September 2024)

(6) Yiftachel, O. (2009), Critical Theory and ‘gray space’ Mobilisation of the Colonized at https://www.researchgate.net/publication/248930381_critical_theory_and_’gray_space’_Mobilisation_of_thecolonized (accessed in September 2023)

(7) McLean A. I., at https://peopleknowhow.org/wp-content/uploads/2019/01/what-are-the-benefits-of-green-and-blue-space.pdf (accessed in September 2022)

(8) https://environmentagency.blog.go.uk/2021/08/04/blue-space-the-final-frontier/ (accessed in September 2022)

(9) Dorsey, J. W. (2003). Brownfields and Greenfields: The Intersection of Sustainable Development and Environmental Stewardship. Environmental Practice, 5(1), 69-76, https://doi.org/10.1017/S1466046603030187 (accessed in September 2024)

(10) Depietri, Y. & McPhearson, T., (2017), Nature-based Solutions to Climate Change Adaptation in Urban Areas, Theory and Practice of Urban Sustainability Transitions, N. Kabisch et al. (eds.), DOI 10.1007/978-3-319-56091-5_6

(11) https://www.wallstreetmojo.com/financial-strategies/ (accessed in September 2025)

(12) https://roadmunk.com/guides/roadmap-definition/ (accessible in September 2025)

(13) https://ffpractitioner.org/the-myths-and-realities-of-defining-family-wealth-whose-definition-is-it-anyway/ (accessed in September 2025)

(14) https://allwealth.com/creating-your-financial-roadmap (accessed in September 2025)

(15) https://www.paydata.co.uk/hr-hub/reports/paystats-and-national-statistics/paystats-pay-and-labour-market-statistics-september-2025/ (accessed in September 2025)

(16) https://brc,org.uk/news-and-events/news/corporate-affairs/2025/ungated/high-inflation-weighing-on-consumer-confidence/ (accessed in September 2025)

(17) https://www.ons.gov.uk/businessindustryandtrade/retailindustry/bulletins/retailsales/august2025 (accessed in September 2025)

(18) https://www.bankofengland.co.uk/monetary-policy-summary-and-minutes/2025/september-2025?Fds-Load-Behavior=force-external (accessed in September 2025)

(19) https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/bulletins/averageweeklyearningsingreatbritain/september2025 (accessed in September 2025)

(20) https: //www.nimblefins.co.uk/average-uk-household-budget (accessed in September 2025)

_________

• Help CENFACS Keep the Poverty Relief Work Going This Year

We do our work on a very small budget and on a voluntary basis. Making a donation will show us you value our work and support CENFACS’ work, which is currently offered as a free service.

One could also consider a recurring donation to CENFACS in the future.

Additionally, we would like to inform you that planned gifting is always an option for giving at CENFACS. Likewise, CENFACS accepts matching gifts from companies running a gift-matching programme.

Donate to support CENFACS!

FOR ONLY £1, YOU CAN SUPPORT CENFACS AND CENFACS’ NOBLE AND BEAUTIFUL CAUSES OF POVERTY REDUCTION.

JUST GO TO: Support Causes – (cenfacs.org.uk)

Thank you for visiting CENFACS website and reading this post.

Thank you as well to those who made or make comments about our weekly posts.

We look forward to receiving your regular visits and continuing support until the end of 2025 and beyond.

With many thanks.