Welcome to CENFACS’ Online Diary!

25 October 2023

Post No. 323

The Week’s Contents

• FACS, Issue No. 81, Autumn 2023, Issue Title: Financial Inclusion for the Needy

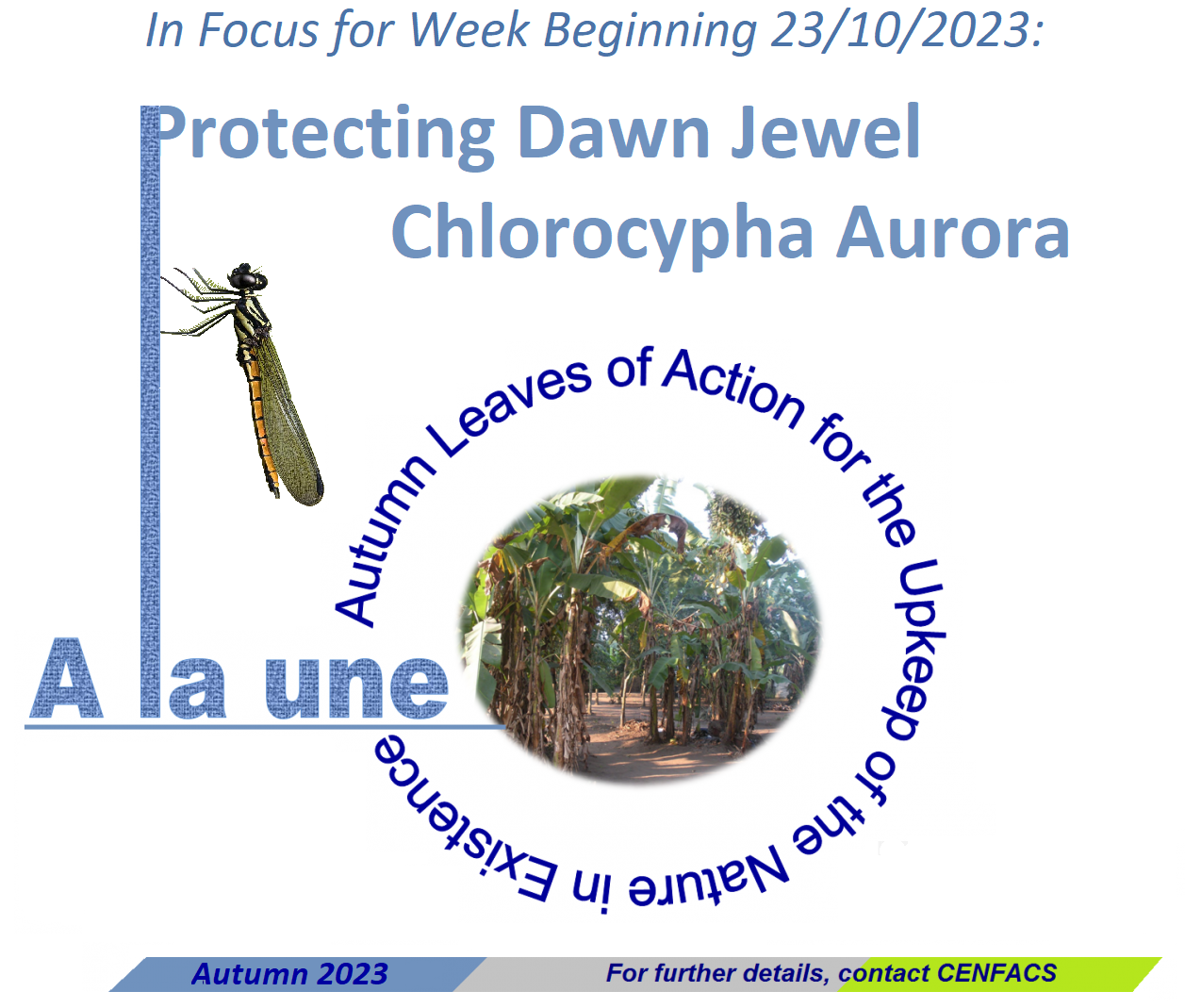

• “A la une” (Autumn Leaves of Action for the Upkeep of the Nature in Existence) Campaign and Themed Activities – In Focus for Week Beginning 23/10/2023: Protecting Dawn Jewel (Chlorocypha Aurora)

• Review of Medium-term Actions/Service under the Campaign to End Poverty Induced by Rising Costs of Living

… And much more!

Key Messages

• FACS, Issue No. 81, Autumn 2023, Issue Title: Financial Inclusion for the Needy

The 81st Issue of FACS stocktakes most of matters discussed in our last July Festival of Thoughts and Actions, which focussed on Financial Inclusion to Improve the Quality of Poor People’s Lives. The 81st Issue of FACS goes further in exploring ways of working with the communities here in the UK and in Africa to enhance financial inclusion for them.

The 81st Issue of FACS approaches financial access and inclusion from the “user-side” view, from the removal of demand-side constraints on the financially excluded. From this point of view, demand from unbanked individuals could be created to realise financial access and inclusion. The 81st Issue of FACS also is an experimental approach to financial poverty that draws inspiration from the financially excluded and needy people, and that uses deliberative practice or methodology.

The 81st Issue of FACS acknowledges the progress made to financially include many of the poor people, who work with our Africa-based Organisations, from exclusively cash-based transactions to formal financial services by using a mobile phone or other digital technologies to access these services. However, it also recognizes that there are still people who are finding it difficult to be part of this financial world. These financially excluded or underserved poor people, of which some of them make our community, could be struggling to improve the quality of their lives.

Amongst these strugglers, there are examples of poor women in rural areas of Africa who are lacking access to financial services. There are as well those highly indebted (because of the enduring cost-of-living crisis or the effects of other crises like the lingering effects of the coronavirus) who have been excluded from the financial world, apart from worrying how they could get back to this world.

They could be struggling because financial inclusion is more than just getting people, especially the poor ones, to move to financial digital products and services offered on the market. Jack Onyisi Abebe et al. (1) explain that

“Financial inclusion goes beyond improved access to credit to encompass enhanced access to savings and risk mitigation products, a well-functioning financial infrastructure that allows women and women-owned enterprises to engage more actively in the economy, while protecting their rights” (p. 11)

In this respect, the 81st Issue of FACS is a gripping story of Africa-based Sister Organisations that are working with their locals in their journey to financial inclusion, to find opportunities to reduce financial poverty. They are as well running projects to help the polycrises-impacted people to be financially re-included in the agenda for financial inclusion for all. They are further undertaking initiatives conducive to close gender gaps in financial inclusion and gender digital divide. They are finally joining forces with their users so that the latter can access financial inclusion programmes that are on offer where they live.

The 81st Issue of FACS is not only dealing with one generation of financial excluded. Instead, it caters for all generations. Amongst these generations, there is the older one. The 81st Issue of FACS addresses the gaps and challenges that prevent Africa’s older generation from accessing cost-saving means linked to financial services and products.

Far from being a theoretical story or account of the financial excluded people, the 81st Issue of FACS provides some clues for them to navigate their way out of financial exclusion. Full of fresh ideas about Africa-based Sister Organisations’ way of working with the financially excluded locals, the 81st Issue of FACS shows that financial inclusion can change the needy persons’ life.

The 81st Issue of FACS does not only explain the financial inclusion problems faced by these persons and the members of our community, but it makes recommendations for action. In this respect, it gives the readers and our audiences a good understanding of the financial inclusion challenges experienced by these persons and our members, as well as the efforts made to mitigate these challenges. In doing so, it dispels the myth of hopelessness for the financial excluded, while providing options and opportunities for them.

To get further insights about the Issue No. 81, please read the summaries presented under the Main Development section of this post.

• “A la une” (Autumn Leaves of Action for the Upkeep of the Nature in Existence) Campaign and Themed Activities – In Focus for Week Beginning 23/10/2023: Protecting Dawn Jewel (Chlorocypha Aurora)

To protect Dawn Jewel (Chlorocypha Aurora), we are going to highlight what is known about the treats and risks it faces and what it can be done to protect it. In addition to that, we are going to highlight the insect themed activity we planned for this week.

• • Dawn Jewel (Chlorocypha Aurora) is Threatened and at Risk

The conservation status of the Dawn Jewel (Chlorocypha Aurora) given by the International Union for Conservation of Nature’s Red List of Threatened Species (2) indicates that it is critically endangered. According to Spoorthy Raman (3), the Dawn Jewel (Chlorocypha Aurora) is a critically endangered damselfly from Cameroon. Its habitat is declining due to forest destruction, water pollution, and situation.

It is a situation that most dragonflies face; a situation of humans’ destruction of their wetland habitats, water pollution, and climate change. This destruction is mostly for settlements, farming, wood harvesting and logging.

If the Dawn Jewel (Chlorocypha Aurora) is threatened with and at risk of extinction, then it needs protection.

• • Protecting Dawn Jewel (Chlorocypha Aurora)

Research and work within the literature about Dawn Jewel (Chlorocypha Aurora) suggest the following initiatives to protect it:

~ taking care of wetlands in all scales

~ improving the protection of the wetland ecosystems in development projects

~ keeping away harmful pollutants (e.g., pesticides) that harmfully impact the prey of dragonflies and damselflies or change the quality of water

~ stopping any type of waste (be it industrial or sewage or mining) from polluting streams and rivers

etc.

• • Add-on Activity of the Week’s Campaign: E-discussion on Insects as Reducers of Plastic Pollution

The insect themed activity of this week is an online discussion space on how plastivore insects can degrade plastic waste. There are studies and publications that suggest that plastivore insects (4) can eat plastic waste or insects are degraders of plastics (5).

During our e-discussion, we shall talk about the gifts that beneficial insects can bring to our lives in helping us to deal with the garbage or trash crisis, in particular the crisis linked to plastic waste. People can contribute their answers and respond to other participants by making their agreement or difference, raising issues and sharing evidence, knowledge and data.

Those who may be interested in taking part in this e-discussion or insect themed activity, they can contact CENFACS.

To find out more about the entire “A la une” Campaign and Themed Activities, please communicate with CENFACS.

• Review of Medium-term Actions/Service under the Campaign to End Poverty Induced by Rising Costs of Living

We are continuing the Review of the Campaign to End Poverty Induced by Rising Costs of Living. This week, the Review is related to Medium-term Actions/Service under this Campaign. The review is about the second level of actions (medium-term service) we undertook together with our users in order to tackle the cost-of-living crisis.

The medium-term service was designed to avoid that the cost-of-living crisis settles in with the time and becomes a humanitarian issue or crisis. The service has been available for those members of our community who needed it and who would like to ask for it. Under the scope of this service, actions were supposed to be taken between 6 and 24 months.

In this current review, we are re-examining the following:

√ the assessment we made with users about how the cost-of-living crisis was affecting them and their needs as a result of crisis effects

√ any action plan we developed with the applicants to the medium-term service to come out of the cost-of-living crisis in medium term

√ any action of encouragement we advised them to take or any skills they learnt to adapt until now time and any skills that were meant to help them navigate out of the cost-of-living crisis

√ any support we provided to them to build energy and food security systems in the medium term and beyond.

The review will enable to know what has worked and did not work in the context of Medium-term Actions/Service under the Campaign to End Poverty Induced by Rising Costs of Living.

For any queries about this second review, please contact CENFACS.

Extra Messages

• Happening this Week: Making Memorable Positive Difference Project – In Focus: History of Cottage Industries in Reducing Poverty in Africa

• Taking Climate Protection and Stake for African Children at the Implementation with Installation Sub-phase (Phase 3.2) – Five Weeks Ahead of COP28

• CENFACS’ be.Africa e-Discusses the Outputs from the World Investment Forum 2023 and Not-for-profit Impact Investing in Africa

• Happening this Week: Making Memorable Positive Difference Project

In Focus: History of Cottage Industries in Reducing Poverty in Africa

The 15th Event of Making Memorable Difference Project will start on 27/10/2023 as scheduled. It will be the celebration of African Abilities, Talents, Skills, Legacies and Gifts to Africa and the world.

For those who would like to make contribution to our Two Days of African History, they are welcome to do so. They can contribute to the following:

a) Heritage/Patrimony/Champions’ Day on 27 October 2023, day which will focus on History of Profiles of Household-based Industry Proprietors and Labourers

b) Legacies and Gifts Day on 28 October 2023; day which will be dedicated to the Historical Contribution of the Household-based Industries in Reducing Poverty and in Creating Wealth in Africa.

• • To Engage and or Contribute to the History Days

You can tell and share with us what they know about

~ the identities and profiles household-based industry proprietors and labourers, and/or

~ the historical contribution of the household-based industries in reducing poverty and in creating wealth in Africa.

• • Forms of Your Telling

Your telling or sharing could be in the form of:

texts, documents, references, comments, audio and visual materials, oral communications, art objects and any other historical resources.

• • To Donate

In addition to donating what you know about cottage industries in Africa, people can donate money. For those who can, they could support CENFACS’ Two History Days and Making Memorable Positive Difference Project with a donation of money to acknowledge our efforts, to help us recover costs of organising such eventful days and to build forward better African History.

To engage with this year’s Making Memorable Positive Difference theme and or support this project, please contact CENFACS on this site.

• Taking Climate Protection and Stake for African Children at the Implementation with Installation Sub-phase (Phase 3.2) – Five Weeks Ahead of COP28

Under CENFACS’ CPSAC (Climate Protection and Stake for African Children) and its sub-phase 3.2., we are continuing to make the case for our demand to give a climate stake to children.

We are as well carrying out our preparation for the follow-up of the 28th session of the Conference of the Parties (COP 28) to the UNFCCC (United Nations Framework Convention on Climate Change), which will be convened in Dubai (United Arab Emirates) from 30 November to 12 December 2023 (6). This engagement or follow up will contribute to TCPSACI.

The slogan for this 2023 follow-up is: Dubai Raise Children’s Ambitions and Hopes.

As part of this preparation, we are discussing the ways of raising children’s ambitions and hopes in the light of the planned programme of COP28.

We are also considering the key points discussed at various climate meetings and events (e.g., Africa Climate Week 2023, Talks on Climate Loss and Damage, etc.) held so far in the preparation of COP28. We are reflecting on how these pre-COP28 Talks can fit into CENFACS’ CPSAC and its sub-phase 3.2.

To support and or enquire about CENFACS’ CPSAC and its sub-phase 3.2, please contact CENFACS.

• CENFACS’ be.Africa e-Discusses the Outputs from the World Investment Forum 2023 and Not-for-profit Impact Investing in Africa

The UNCTAD (United Nations Conference on Trade and Development) World Investment Forum 2023 was held in Abu Dhabi (United Arab Emirates) from 16 to 20 October 2023 (7). At this Investment Forum, many subjects were discussed, subjects such as public and private investment to transform agri-food systems and global crisis, the AfCFTA (African Continental Free Trade Area) Protocol on investment, investments for a livable planet, the scaling up of energy transition investments, the bridge on investment data gaps, etc.

Further to the outputs from the UNCTAD World Investment Forum 2023, CENFACS be.Africa Forum would like to debate the following two issues:

a) How Africa Sovereign Investors Forum (ASIF) can promote not-for-profit investments for impact in Africa (knowing that ASIF goal is to facilitate the mobilisation of long-term capital to develop Africa)

b) The extent to which a New Academic Research Agenda on Investment can be expanded to include not-for-profit investment projects and programmes in Africa since the probability of reducing poverty via this type of investments is high.

Those who may be interested in the above-mentioned issues can join in and or contribute by contacting CENFACS’ be.Africa, which is a forum for discussion on matters and themes of poverty reduction and sustainable development in Africa and which acts on behalf of its members in making proposals or ideas for actions for a better Africa.

They can as well join us with a donation or a gift to enable more actions and ideas to drive a positive impact on Africa.

To communicate with CENFACS regarding this discussion or support, please use our usual contact details on this website.

Message in French (Message en français)

• À l’affiche cette semaine: Projet ‘Faire une différence positive mémorable’

Gros plan sur l’histoire de l’artisanat dans la réduction de la pauvreté en Afrique

Le 15e événement du projet ‘Faire une différence positive mémorable’ débutera le 27/10/2023 comme prévu. Ce sera la célébration des capacités, des talents, des compétences, des héritages et des dons africains à l’Afrique et au monde.

Pour ceux/celles qui voudraient apporter leur contribution à nos Deux Jours de l’Histoire de l’Afrique, ils/elles sont les bienvenu(e)s. Ils/elles peuvent contribuer à ce qui suit:

a) Journée de l’Héritage/du Patrimoine/des Champions, le 27 octobre 2023; journée qui portera sur l’histoire des profils des propriétaires d’industries et des ouvriers familiaux

b) Journée des Legs et des Dons, le 28 octobre 2023; qui se concentrera sur la contribution historique des industries domestiques à la réduction de la pauvreté et à la création de richesse en Afrique.

• • S’engager et/ou contribuer aux journées de l’histoire

Vous pouvez nous dire et partager avec nous ce que vous savez sur

~ les identités et les profils des propriétaires d’entreprises et des ouvriers familiaux et/ou

~ la contribution historique des industries familiales à la réduction de la pauvreté et à la création de richesse en Afrique.

• • Formes de votre récit

Votre récit ou votre partage peut prendre la forme suivante:

les textes, les documents, les références, les commentaires, le matériel audio et visuel, les communications orales, les objets d’art et toute autre ressource historique.

• • Pour faire un don

Pour ceux/celles qui le peuvent, ils/elles pourraient soutenir les deux Journées de l’histoire et le projet ‘Faire une différence positive mémorable’ du CENFACS avec un don pour reconnaître nos efforts, pour nous aider à couvrir les coûts de l’organisation de ces journées riches en événements et pour construire une meilleure histoire africaine.

Pour participer au thème ‘Faire une différence positive mémorable’ de cette année et/ou soutenir ce projet, veuillez contacter le CENFACS sur ce site.

Main Development

• FACS, Issue No. 81, Autumn 2023, Issue Title: Financial Inclusion for the Needy

The contents and key summaries of the 81st Issue of FACS are given below.

• • Contents and Pages

I. Key Concepts Relating to the 81st Issue of FACS (Page 2)

II. Approach to Financial Inclusion (Page 2)

III. Theory of Financial Inclusion Used in the 81st Issue of FACS (Page 2)

IV. Africa-based Sister Organisations and their Work on Financial Inclusion (Page 3)

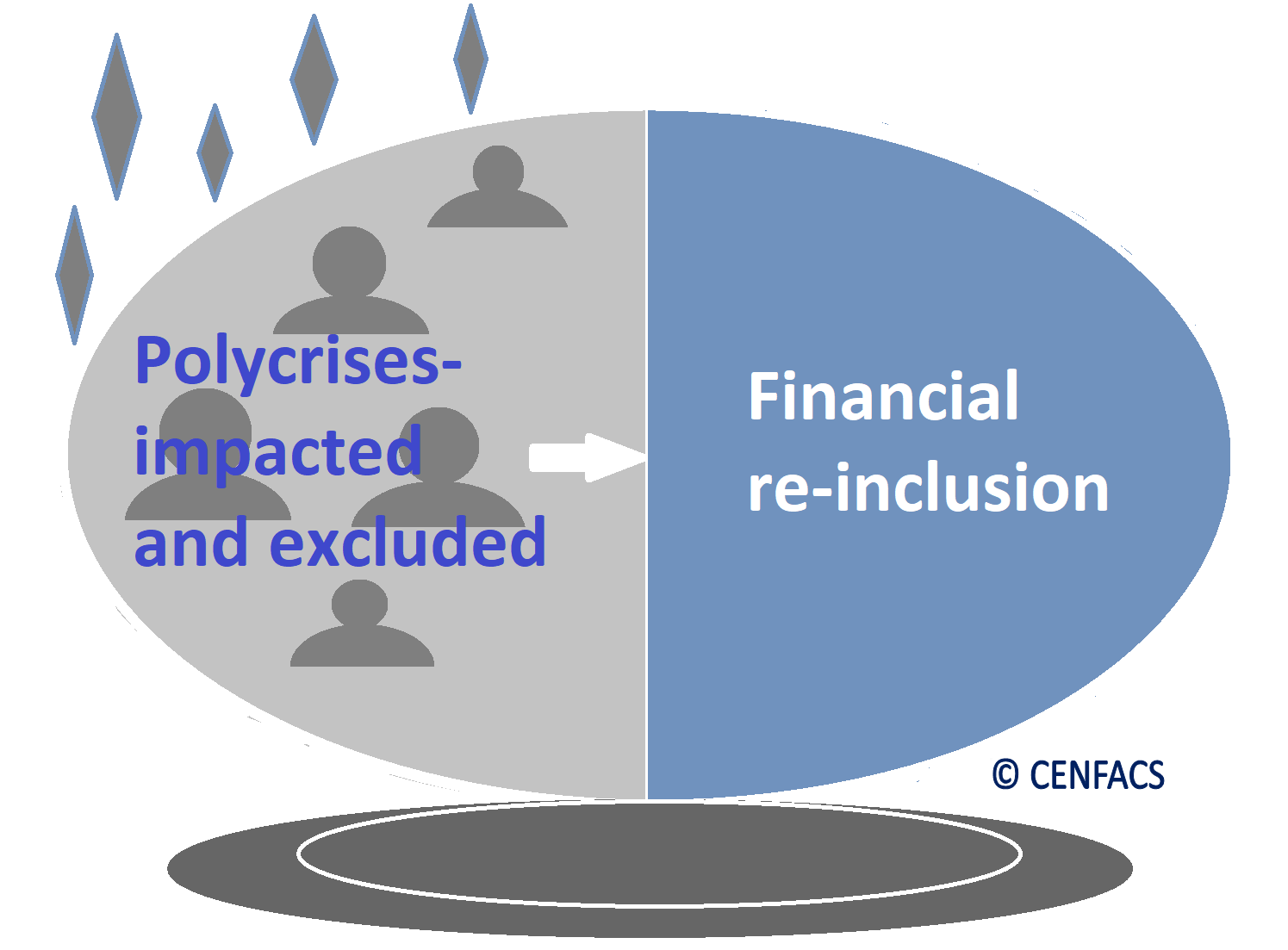

V. Africa-based Sister Organisations and the Financial Re-inclusion of the Polycrises-impacted (Page 3)

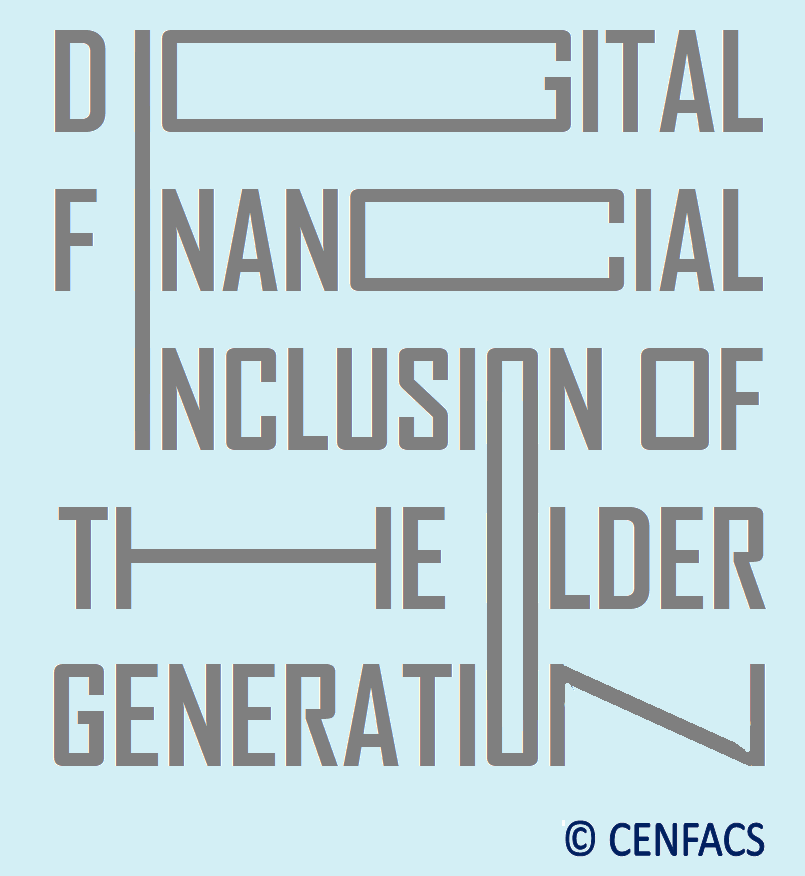

VI. Digital Financial Inclusion of the Older Generation in Africa (Page 4)

VII. Financial Inclusion through Economic Security of the Older Generation (Page 4)

VIII. Les organisations sœurs basées en Afrique et leur travail pour combler les écarts entre les sexes en matière d’inclusion financière (Page 5)

IX. L’inclusion financière par le biais du financement climatique (Page 5)

X. L’inclusion financière et la réduction de la pauvreté financière par les organisations sœurs basées en Afrique (Page 6)

XI. Les organisations sœurs basées en Afrique et leurs nouvelles idées pour travailler avec des habitants financièrement exclus (Page 6)

XII. Survey, Testing Hypotheses, E-questionnaire and E-discussion on Financial Inclusion and Poverty Reduction (Page 7)

XIII. Support, Tool and Metrics, Information and Guidance on Financial Inclusion and Poverty Reduction (Page 8)

XIV. Workshop, Focus Group and Booster Activity about Financial Inclusion and Poverty Reduction (Page 9)

XV. Giving and Project (Page 10)

• • Key Summaries

Please find below the key summaries of the 81st Issue of FACS from page 2 to page 10.

• • • Key Concepts Relating to the 81st Issue of FACS (Page 2)

There are three concepts used in the context of this Issue of FACS. These concepts are financial inclusion, the needy and financial inclusion programme. Let us briefly explain these concepts.

• • • • Financial Inclusion

There are many definitions of financial inclusion. The 81st Issue of FACS will focus on the definitions that are related to those living in poverty or experiencing financial hardships. One of these definitions comes from Peterson K. Ozili (8) who explains that

“Financial inclusion is the provision of, and access to, financial services to all members of population particularly the poor and the other excluded members of the population” (p. 3)

Generally speaking these poor and excluded are the needy.

• • • • The Needy

Our definition of the needy comes from ‘dictionary.com’ (9) which states that

“The needy is a noun referring collectively to people who are poor or otherwise in need”.

They are those lacking the necessities of life.

Form this definition and in the context of financial exclusion, we can include the following:

√ formerly financially excluded

√ financially underserved poor consumers of financial products and services

√ unbanked including poor women in rural areas

√ small women farmers and business women without links with formal financial institutions

√ those looking for opportunity to reduce financial poverty via financial inclusion

√ those highly indebted and financially excluded

√ the poly-crises impacted people

√ those exclusively relying on cash transactions

√ the financially excluded or underserved poor people

√ those without functional bank account or e-money account

√ financially digitally illiterate and innumerate

√ the older generations unable to handle digitally-enabled transactions and technologies

√ financially excluded by the adverse impacts of the overlapping multiple crises (the lingering effects of the coronavirus, the cost-of-living crisis, etc)

etc.

Many of these people listed above may need financial inclusion programme to get included or re-included.

• • • • Financial Inclusion Programme

It is a series of planned projects to be undertaken to achieve financial inclusion goal or aim. According to ‘assets.publishing.service.gov.uk’ (10),

“Financial inclusion programme is a series of projects aiming at increasing and improving the use of fair affordable and appropriate financial products and services that boost savings, increase protection against shocks, smooth incomes and increase access to and use of fair, affordable and appropriate credit”.

The above-named definitions shape the contents of the 81st Issue of FACS. However, definitions alone may not be enough to achieve financial inclusion. One may need to determine the approach they want to take in their journey to financial inclusion.

• • • Approach to Financial Inclusion (Page 2)

The 81st Issue of FACS approaches financial access and inclusion from the “user-side” view, from the removal of demand-side constraints on the financially excluded. From this point of view, demand from unbanked individuals could be created to realise financial access and inclusion.

From the above-mentioned perspective, the 81st Issue of FACS also is an experimental approach to financial poverty that draws its inspiration from the financially excluded and needy people, and that uses deliberative practice or methodology.

For example, looking at the demand-sided factors that influence financial inclusion in Africa, Anthony Yaw Nsiah and George Tweneboah (11) point out the work of Bekele (2022) who argues that

“In Kenya and Ethiopia, gender, age, employment status and ownership of a mobile phone significantly influence financial inclusion”.

The same Nsiah and Tweneboah refer to the work of Ndanshau and Njau (2021) who empirically examined demand-side factors that influence financial inclusion in Tanzania. According to Ndanshau and Njau,

“Employing the probit model, the study found that being male, middle aged, gain-fully employed, resident in urban area, having multiple streams of income and highly educated persons are more likely to be included in the financial sector in Tanzania”.

So, demand-sided factors (such as gender, education, age, income level, etc.) are significant contributing factors in one’s involvement in the financial sector. However, one may need a theory to back or explain the facts.

• • • Theory of Financial Inclusion Used in the 81st Issue of FACS (Page 2)

Financial inclusion definitions and approaches come with theories to support them. Likewise, financial facts may require financial theories to explain them. The 81st Issue of FACS uses the vulnerable group theory of financial inclusion. What this theory is about. According to Peterson K. Ozili (op. cit.),

“The vulnerable group theory of financial inclusion argues that financial inclusion programme in a country should be targeted to the vulnerable members of society who suffer the most from economic hardship and crisis, such as poor people, young people, women, and elderly people. The theory argues that vulnerable people are often the most affected by financial crises and economic recession, therefore, it makes sense to bring these vulnerable people into the formal financial sector. One way to achieve this is through government-to-person social cash transfers into the formal account of vulnerable people” (p. 7)

This theory will be amongst the arguments or tools to be used in order to advocate and advance the cause of the needy with regard to financial inclusion.

• • • Africa-based Sister Organisations and their Work on Financial Inclusion (Page 3)

Although in many parts of Africa, financial inclusion is being regarded as the area of expertise of financial institutions and supply side driven by financial institutions, our Africa-based Sister Organisations (ASOs) try to support their beneficiaries on matter linked to financial inclusion. ASOs work with them by providing services to them to move from exclusively cash-based transactions by using mobile phone and other digital technologies to access financial services and products.

ASOs’ services related to financial inclusion include financial advice and advocacy, awareness raising to bring down some myths about financial inclusion, financial skills development (e.g., financial literacy and numeracy), basic training on how to use e-money technologies, etc. In doing so, ASOs try to scale down the effects of barriers linked to demand-side factors of financial inclusion.

• • • Africa-based Sister Organisations and the Financial Re-inclusion of the Polycrises-impacted (Page 3)

In recent years, like other regions of the world Africa went through many crises (such as the coronavirus disaster, food crisis, energy crisis, debt crisis, climate crisis, wars in some parts of Africa, natural events, etc.). The impact of recent cascading and connected crises – call them polycrisis – has led to the economic collapse of many poor people. These people have been simply excluded, in some cases written off, from the financial sector and the books.

To support these economically collapsed poor people, our Africa-based Sister Organisations are working with them so that these excluded people of the polycrises era could be re-included and be part of the agenda for financial inclusion for all.

• • • Digital Financial Inclusion of the Older Generation in Africa (Page 4)

Africa is mostly populated by the younger generation. Like the younger generation, the older one needs to have some basic financial digital skills and knowledge in order to run their daily life matters and stay in tune with the evolution of the world they live in. To help them keep pace in their journey to digital financial inclusion, Africa-based Sister Organisations working on old age matter try to address the gaps and challenges that prevent the older generation of Africans from accessing cost-saving means linked to digital financial inclusion. In doing so, they try to help not to leave behind the older African generation.

• • • Financial Inclusion through Economic Security of the Older Generation (Page 4)

According to the Global Social Development Innovations (12),

“Economic security is the ability of individuals, households and communities to meet their basic and essential needs sustainably including food, shelter, clothing, health care, education, information, livelihoods and social protection”.

The older generation too wants to meet their basic and essential needs in a sustainable way. Financial inclusion could be one of the needs they would like to satisfy to avoid economic insecurity and old age poverty. In this respect, financial inclusion and economic security go hand in hand regardless of generations, whether it is in Africa or elsewhere.

• • • Les organisations sœurs basées en Afrique et leur travail pour combler les écarts entre les sexes en matière d’inclusion financière (Page 5)

Selon Majorie Chalwe-Mulenga and Gerhard Coetzee (13),

“l’Afrique subsaharienne est à la traîne par rapport aux autres en ce qui concerne la réduction de l’écart entre les sexes en matière d’inclusion financière et d’indicateurs relatifs à la valeur des services financiers”.

D’après eux,

“En Afrique subsaharienne, l’écart entre les sexes en matière de détention de comptes est passé de 5 % en 2011 à 12 % en 2021, soit trois fois plus que la moyenne mondiale et le double de celui des autres pays en développement”.

Ce faisant, les organisations sœurs basées en Afrique travaille pour réduire les obstacles et les goulots d’étranglement qui entravent l’accès et l’utilisation des services et produits financiers par les femmes. Leur travail peut être très utile de réduire la fracture numérique entre les sexes, tout comme la suppression des contraintes structurelles socio-économiques et de la demande qui pèsent sur les femmes.

• • • L’inclusion financière par le biais du financement climatique (Page 5)

Le financement d’activités visant à atténuer les impacts du changement climatique ou à s’y adapter peut également être un moyen de créer et de maintenir l’inclusion financière des personnes dans le besoin.

Cette création et ce maintien peuvent se produire si les programmes d’inclusion financière peuvent aider les pauvres et les personnes vulnérables à accéder et à utiliser le financement climatique (comme la finance verte inclusive) pour renforcer la résilience et atténuer les effets néfastes du changement climatique. De même, ceux ou celles qui deviennent pauvres (pauvres à cause du climat) peuvent être inclu(e)s financièrement.

• • • L’inclusion financière et la réduction de la pauvreté financière par les organisations sœurs basées en Afrique (Page 6)

L’histoire captivante des organisations sœurs basées en Afrique avec leurs sections locales dans leur cheminement vers l’inclusion financière porte sur la façon dont elles peuvent réduire la pauvreté grâce à cette inclusion.

En d’autres termes, le processus d’accès et d’utilisation des services et produits financiers doit ouvrir la possibilité de réduire le manque de revenus, d’épargne, d’accès à des prêts abordables, etc. À cet égard, l’inclusion financière a conduit certains de leurs bénéficiaires à réduire la pauvreté financière.

Mais, on a besoin d’une théorie du changement ou d’une histoire d’impact qui explique le mouvement (lien de cause à effet) vers la réduction de la pauvreté et l’augmentation du bien-être. Dans certains endroits (où des données étaient disponibles), il a été possible de réaliser ce changement en Afrique. Au contraire, là où il est difficile d’obtenir des données, les organisations sœurs basées en Afrique ont encore beaucoup de travail à faire pour passer de l’inclusion financière à la réduction de la pauvreté.

• • • Les organisations sœurs basées en Afrique et leurs nouvelles idées pour travailler avec des habitants financièrement exclus (Page 6)

L’inclusion financière peut être créée et innovée puisqu’il ne s’agit pas d’un domaine limité. Par le biais de pratiques délibératives et de travaux expérimentaux sur la réduction de la pauvreté, les organisations sœurs basées en Afrique ont recueilli de nombreuses idées et suggestions de la part des personnes financièrement exclues en Afrique sur la manière dont elles peuvent être aidées en termes d’inclusion financière.

Parmi ces idées, il y a des moyens de refléter les valeurs locales et les différences culturelles dans l’approche de l’inclusion financière, car l’inclusion financière n’est pas une science exacte. Les coutumes, les cultures, les valeurs, les croyances et les pratiques locales doivent être considerées si l’on veut une inclusion financière qui répond aux besoins et attentes locaux.

Pour éviter une inclusion financière déconnectée des réalités et vies locales, les organisations soeurs basées en Afrique essaient de rapprocher et de contextualiser l’inclusion financière avec les réalités locales tout en se gardant du décalage avec les principes et normes sous-jacents de l’inclusion financière.

• • • Survey, Testing Hypotheses, E-questionnaire and E-discussion on Financial Inclusion and Financial Poverty (Page 7)

• • • • Survey on financial inclusion

Financial inclusion can be measured in three dimensions, which are: access to financial services, usage of financial services, and the quality of the products and services delivery.

The purpose of this survey is to collect information from a sample of our users and community members regarding their access to, usage of and the quality of financial services and products they have been offered or delivered to them.

Participation to this survey is voluntary.

As part of the survey, we are running a questionnaire which contains some questions. One of these questions is:

Q: In your opinion, which of the above-mentioned dimensions of financial inclusion you are not satisfied with or failing to meet?

You can respond and directly send your answer to CENFACS.

• • • • Testing Hypotheses about causal relationships between financial inclusion and financial poverty reduction

For those of our members who would like to dive deep into the impact of financial inclusion on poverty, we have some educational activities for them. They can investigate the impact of financial inclusion on poverty reduction of the needy. They can test the inference of the following hypotheses:

a) Null hypothesis (Ho): Financial inclusion of the needy is positively associated with the reduction of poverty for them

b) Alternative hypothesis (H1): Financial inclusion of the needy is not positively associated with the reduction of poverty for them.

In order to conduct these tests, one needs data on financial inclusion and the needy.

• • • • E-questions about experience dealing with financial inclusion

Any of our readers and users can answer the following questions about the financial inclusion they need in order to change their personal life.

Q1: What kinds of challenges and gaps do you face from accessing cost-saving means linked to financial services and products?

Q2: Do you think that there are constraints that financially exclude you from financial services and products?

Q3: What do you need to stimulate demand from you to access and use quality financial services and products?

You can provide your answer directly to CENFACS.

For those answering any of these questions and needing assistance about their financial inclusion problem, CENFACS can work with them on this matter via its Advice-giving Service (service which we offer to the community for free) to find way forward to deal with financial inclusion issues they are experiencing.

• • • • E-discussion on one’s involvement in the financial sector

Many of our members have their own views on what determine one’s access to and use of financial services and products. Some think gender (being a male or female). Others argue it is education and employment status. Others more say, it is wealth (being rich or poor).

For those who may have any views or thoughts or even experience to share with regard to this matter, they can join our e-discussion to exchange their views or thoughts or experience with others.

To e-discuss with us and others, please contact CENFACS.

• • • Support, Tool and Metrics, Information and Guidance on Financial Inclusion and Poverty Reduction (Page 8)

• • • • Ask CENFACS for Support regarding the reduction of poverty linked to financial exclusion

Financial exclusion poverty is the inability to access and use affordable financial services and products.

For those members of our community who feel financially excluded and would like to navigate their way out of financial exclusion poverty, CENFACS can work with them to explore ways of coming out of it.

We can work with them under our Advice-, Guidance- and Information-giving Service. We can as well signpost them to organisations working on financial inclusion for those in need.

We can work with the community in the different areas of financial inclusion support including financial education (literacy, numeracy and digital), gender disparities in financial inclusion, improving users’ financial history, consumer protection on matter relating to financial inclusion, etc.

If you are a member of our community, you can ask us for basic support regarding your inability to access and use affordable financial services and products.

• • • • Tool and Metrics of the 81st Issue of FACS

• • • • • Financial Inclusion Tool: The Global Findex

One of the tools used to measure global financial inclusion is the Global Findex.

According to ‘microdata.worldbank.org’ (14),

“The Global Findex is the world’s most comprehensive database on financial inclusion. It is also the only global demand-side data source allowing for global and regional cross-country analysis to provide a rigorous and multidimensional picture of how adults save, borrow, make payments, and manage financial risks”.

Those who would like to discuss the relevancy of this tool and its application, they can feel free to contact CENFACS.

• • • • • Other Metrics to measure financial inclusion

The Issue 81 also considers other metrics that also can be applied to the needy. These other metrics are the three dimensions of financial inclusion and poverty gap ratio.

a) The three dimensions of financial inclusion

They include access to, the use of and the quality of affordable financial services and products delivered to them.

b) Poverty gap ratio

This is an interesting metrics of poverty as it measures the intensity of poverty.

The online ‘marketbusinessnews.com’ (15) explains that

“The poverty gap ratio or poverty gap index is the average of the ratio of the poverty gap to the poverty line. Economists and statisticians express it as a percentage of the poverty line for a region or whole country…The poverty gap ratio considers how far, on the average, poor people are from poverty line”.

The above tool and metrics can be used in dealing with financial inclusion and the reduction of financial exclusion poverty in Africa. For example, one can use the poverty gap ratio to measure the average shortfall of the income of the financial excluded from the poverty line.

• • • • Information and Guidance on Financial Inclusion and Poverty Reduction

Information and Guidance include two types areas of support via CENFACS, which are:

a) Information and Guidance on Financial Inclusion and Poverty Reduction

b) Signposts to improve users’ experience about Financial Inclusion and Poverty Reduction

• • • • • Information and Guidance on Financial Inclusion and Poverty Reduction

Those members of community who are looking for information and guidance on financial inclusion and who do not know what to do, CENFACS can work with them (via needs assessment) or provide them with leads about organisations and services that can help them.

• • • • • Signposts to improve users’ experience about Financial Exclusion and Poverty Reduction

For those who are looking for whereabout to find help about financial exclusion queries, we can direct them to the relevant services and organisations.

More tips and hints relating to the matter can be obtained from CENFACS‘ Advice-giving Service.

Additionally, you can request from CENFACS a list of organisations and services providing help and support in the area of financial inclusion and the reduction of financial exclusion poverty, although the Issue 81 does not list them. Before making any request, one needs to specify the kind of organisations they are looking for.

To make your request, just contact CENFACS with your name and contact details.

• • • Workshop, Focus Group and Booster Activity about Financial Inclusion and the Reduction of Financial Exclusion Poverty (Page 9)

• • • • Mini Themed Workshop on Financial Inclusion Skills to Reduce Financial Exclusion Poverty

Boost your knowledge and skills about the reduction of poverty linked to financial exclusion via CENFACS. The workshop aims at supporting those without or with less information and knowledge about financial exclusion poverty gain financial inclusion skills and knowledge while improving the quality of their lives. The workshop will provide recommendations for actions with options and opportunities for the financially excluded.

To enquire about the boost, please contact CENFACS.

• • • • Focus Group on Financial Inclusion in Time of Crises

You can take part in our focus group on ways of protecting yourself against crises (e.g., the cost-of-living crisis) through financial inclusion. This workshop is also part of a structured activity to improve your perception of financial inclusion. Participants will have one-on-one conversations with each other outside their comfort zone.

To take part in the focus group using deliberative practice strategies, please contact CENFACS.

• • • • Autumn Fresh Start Activity: Get Financially Included

This user involvement activity revolves around the answers to the following questions:

Q1: How included are you with financial services and products delivered to you?

Q2: How do many of you feel included when it comes to dealing with their financial matter?

Q3: How do many of you turn to professionals for guidance or advice on financial inclusion?

Q4: How do many of you understand the basic principles or issues surrounding financial inclusion?

Those who would like to answer these questions and participate to our Get-Financially-Included Activity, they are welcome.

To take part in this activity, please contact CENFACS.

• • • Giving and Project (Page 10)

• • • • Readers’ Giving

You can support FACS, CENFACS bilingual newsletter, which explains what is happening within and around CENFACS.

FACS also provides a wealth of information, tips, tricks and hacks on how to reduce poverty and enhance sustainable development.

You can help to continue its publication and to reward efforts made in producing it.

To support, just contact CENFACS on this site.

• • • • Project of Financial Inclusion for the Needy of Our Community (PFINOC)

PFINOC is a poverty-relieving project aiming at working with underserved members of our community so that they can gain access to, and use of quality affordable financial services and products through all means available and affordable for them including digital means.

As it is said, this financial inclusion project will not only measure access and usage of financial services and products, but it will help in lifting the financially excluded and needy of our community out of poverty and improve their livelihoods.

To support or contribute to PFINOC, please contact CENFACS.

For further details including the implementation plan of the PFINOC, please contact CENFACS.

The full copy of the 81st Issue of FACS is available on request.

For any queries and comments about this Issue, please do not hesitate to contact CENFACS.

_________

• References

(1) Abebe, J. O., Maina, L., Ondiek, J. & Ogolla, C. (2017), Driving Gender-Responsive Financial Inclusion Models in Africa – Background Paper, UN Women East and Southern Africa, Regional Office, Nairobi

(2) https://www.iucnredlist.org/species/84379630/176166094 (accessed in October 2023)

(3) https://news.mongabay.com/2022/02/new-assessment-finds-dragonflies-and-damselflies-in-trouble-worldwide/ (accessed in October 2023)

(4) https://www.washingtonpost.com/technology/2022/17/plastic-eating-superworm-garbage-crisis/ (accessed in October 2023)

(5) https://www.weforum.org/agenda/2020/03/plastic-waste-caterpillar-moth-larvae-biodegrade/ (accessed in October 2023)

(6) https://www.cop28.com/en/(accessed in October 2023)

(7) https://unctad.org/osgstatement/world-investment-forum-2023-high-level-closing-round-table-investing-sustainable (accessed in October 2023)

(8) Ozili, P. K., (2020), Theories of Financial Inclusion at https://www.researchgate.net/publication/338852717_Theories_of_Financial_Inclusion (accessed in September 2023)

(9) https://www.dictionary.com/browse/needy (accessed in October 2023)

(10) https://assets.publishing.service.gov.uk/media/5ab1050740f0b62d8291e37b/Financial_Inclusion_Statement_of_intent_/_pdf (accessed in October 2023)

(11) Nsiah, A. Y. and Tweneboah, G. (2023), Determinants of Financial Inclusion in Africa: Is Institutional Quality Relevant? Cogent Social Sciences, 9:1, DOI:10.1080/23311886.2023.2184305

(12) https://gsdi.unc.edu/our-work/economic-security/# (accessed in October 2023)

(13) https://www.cgap.org/blog/findex-2021-insights-boosting-financial-inclusion-in-africa (accessed in October 2023)

(14) https://microdata.worldbank.org/index-php/catalog/4607 (accessed in October 2023)

(15) https://marketbusinessnews.com/information-on-credit/gap-ratio–definition-meaning (accessed in August 2023)

_________

• Help CENFACS Keep the Poverty Relief Work Going this Year

We do our work on a very small budget and on a voluntary basis. Making a donation will show us you value our work and support CENFACS’ work, which is currently offered as a free service.

One could also consider a recurring donation to CENFACS in the future.

Additionally, we would like to inform you that planned gifting is always an option for giving at CENFACS. Likewise, CENFACS accepts matching gifts from companies running a gift-matching programme.

Donate to support CENFACS!

FOR ONLY £1, YOU CAN SUPPORT CENFACS AND CENFACS’ NOBLE CAUSES OF POVERTY REDUCTION.

JUST GO TO: Support Causes – (cenfacs.org.uk)

Thank you for visiting CENFACS website and reading this post.

Thank you as well to those who made or make comments about our weekly posts.

We look forward to receiving your regular visits and continuing support throughout 2023 and beyond.

With many thanks.