Welcome to CENFACS’ Online Diary!

26 April 2023

Post No. 297

The Week’s Contents

• FACS Issue No. 79 of Spring 2023 Titled as Financial Education, Information and Communications for and with the Poor

• Protection Key Note 4 for Week Beginning 24/04/2023: Income Protection from Insurance Organisations

• Supporting Networking and Protection against Poverty in 2023

… And much more!

Key Messages

• FACS Issue No. 79 of Spring 2023 Titled as Financial Education, Information and Communications for and with the Poor

Financial education is not a new topic in the field of development or as a way of working with part of the population who is not financially educated. Although it has been around quite a while, it does not reach all the poorest sections of the population, particularly but not exclusively in Africa. Financial information and communications do not cover everybody as well.

For several reasons or factors, a large proportion of poor people do not receive the amount of financial educational skills, information tools and communication settings they need in order to make jumps or leaps in poverty reduction. They may not always have access to financial information they need which apparently could be available.

In the 79th Issue of FACS, we are looking at the three areas of poor people’s financial empowerment (that is; financial education, information and communication) in the current setting or landscape of development in Africa. We will explore ways of making financial information designed with and for the poor reach them. In other words, we shall look at the handicaps or hurdles that prevent poor people in Africa from getting the financial educational skills, information resources and communications tools they need in order to move out of poverty.

The Issue will focus on the basic functional financial educational skills, the financial information market and the travel of this information to the poor in Africa. In this respect, the means of transportation of financial information and how it is consumed by the poor will also be highlighted and revealed.

Furthermore, the Issue will feature how Africa-based Sister Organisations are working with their local poor to bridge the gaps in financial education, information and communication. This is without forgetting the problems they are encountering in trying to reduce poverty linked to the lack of functional financial skills, financial information and financial communications. Of course, this will be done without ignoring the needs of the financial educationally needy, financial uninformed or under informed and communication poor people.

To gain more insight into this new Issue, please read the summaries of its pages provided under the Main Development section of this post.

• Protection Key Note 4 for Week Beginning 24/04/2023: Income Protection from Insurance Organisations

In this last note of Protection Month’s Programme, we are going to explain what we mean by Income Protection from Insurance Organisations and how CENFACS can work with its community regarding this type of income protection.

• • Income Protection from Insurance Organisations

It is simply about buying income protection insurance policy directly from an insurance company or indirectly from an independent financial adviser. If you do not have income protection insurance through your employer or a combined insurance policy or savings, you can consider taking out income protection insurance from an insurance company. There are insurance companies and brokers on the market offering different insurance services and products at competitive prices. What one needs to do is to check their terms and conditions, in particular their eligibility criteria.

However, to buy such a policy one needs to have income in order to meet insurance providers’ purchasing requirements. Those members of our community who can afford can buy such policy. Those who cannot, they may require some support to purchase the policy. Regardless of the affordability problem, CENFACS can work with all its members needing some support about income protection provided by insurance organisations.

• • Working with the Community Regarding Income Protection from Insurance Organisations

Without pretending that CENFACS can do everything including dealing with income protection sold by insurance companies, CENFACS can provide some general and limited support to its members or users who are able to purchase an income protection policy. Our limited and targeted service consists of:

σ Making income protection enquiries on behalf of our members

σ Comparing and contrasting income protection prices between different insurance providers by using online comparison websites and web views

σ Providing leads about the cheapest premiums or insurance providers or policies.

Besides the above-mentioned ways of supporting, we are opened for enquiries for those who have matters to raise regarding their income protection covers from insurance organisations.

As indicated above, Protection Key Note 4 is the last one of our Protection Month’s Programme. However, it does not conclude our Month of Protection since we still have the Protection Day to deal with.

As a way of summarising the four Protection Key Notes presented so far, we would like to remind our users and supporters that protection is above all about preventing and responding to threats and risks of any kinds to the members of our community. Working with our members so that they can find ways of improving or building income protection is part of delivering protection with them.

For those members of our community who are struggling to improve or get income protection insurance they need, they can work with CENFACS on this matter.

For any other queries and enquiries about CENFACS‘ Protection Month, the theme of ‘Income Protection’ and Protection Key Note 4; please do not hesitate to contact CENFACS.

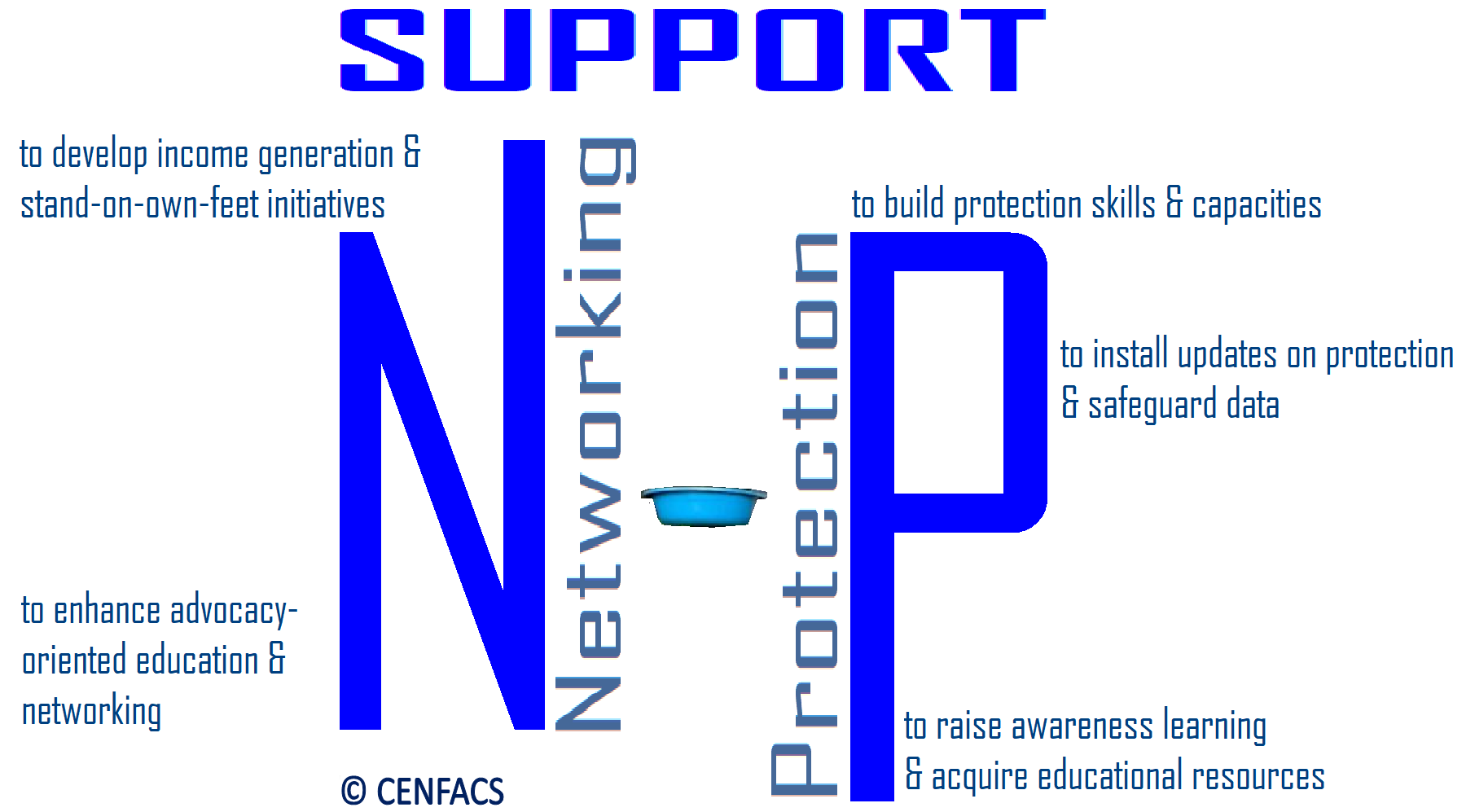

• Supporting Networking and Protection against Poverty in 2023

The Month of Protection within CENFACS is also a giving one towards protection. It is the month of supporting CENFACS’ Networking and Protection project. To support this project, one may need to understand it.

• • What is CENFACS’ Networking and Protection project?

It is a child poverty reduction initiative designed to help and support the vulnerably poor children from HARMS, THREATS and RISKS from any forms of exploitation, neglect and abuse in Africa through the improvement of the flow of information, knowledge development, self-help activities, the increase and diversification of opportunities and chances together with and on behalf of these children. One can back this project by Supporting Networking and Protection against Poverty in 2023.

• • What Supporting Networking and Protection against Poverty in 2023 is about

It is about the following:

√ Improving the flow of information with and amongst the vulnerable people and communities for poverty relief

√ Preventing and responding to any forms of vulnerability threats and risks coming from close and global environments

√ Re-empowering the vulnerable by increasing and diversifying opportunities and strengths amongst them.

• • What Your Support Can Achieve

It will help

√ To raise awareness and improve the circulation and dissemination of information for poverty relief

√ To prevent human exploitation (particularly child exploitation) and respond to child protection and safeguarding issues

√ To re-empower and re-strengthen poor people and communities’ capacities to protect young generations

√ To widen and diversify opportunities to the vulnerable to escape from poverty

√ To develop a well-informed base to reduce information gap and other types of vulnerabilities linked to the lack of networking, interconnectedness and protection.

• • How to Support Networking and Protection against Poverty in 2023

You can DONATE, PLEDGE AND MAKE A GIFT AID DECLARATION for any amount as a way of supporting Networking and Protection against Poverty in 2023.

To donate, gift aid and or support differently, please contact CENFACS.

You can donate

*over phone

*via email

*through text

*by filling the contact form on this site.

On receipt of your intent to donate or donation, CENFACS will contact you. However, should you wish your support to remain anonymous; we will respect your wish.

Extra Messages

• All-year Round Projects Cycle (Triple Value Initiatives Cycle) – Step/Workshop 10: Terminating Your Play, Run and Vote Projects

• Goals Combination: Reduction of Holiday Poverty and of Poverty as a Lack of Income Protection

• Nature Projects and Nature-based Solutions to Poverty: Working Plan for the Second Series of Activities

• All-year Round Projects Cycle (Triple Value Initiatives Cycle) – Step/Workshop 10: Terminating Your Play, Run and Vote Projects

There are various reasons that can lead to project termination. ‘Taskmanagementguide.com’ (1) states that

“Failure and success are two basic reasons for terminating projects”.

The same ‘taskmanagementguide.com’ explains that success happens when project goals and objectives are accomplished on time and under budget, while failure occurs when project requirements are not met.

The above reasons for project termination can be related to the types of project termination to a certain degree; types which could be termination by addition or by integration or by starvation. In the end, what is project termination?

• • Defining Project Termination

There are similarities in the definition of project termination. To simplify the matter, let us refer to the definition of ‘taskmanagementguide.com’, which is

“Project termination is a situation when a given project is supposed to be closed or finalised because there’s no more need or sense for further continuation”.

Similarly, Project Management Institute (2) argues that

“Projects by definition are time bound, and must terminate”.

However, to effectively finalise a project, one needs to follow project closure procedures.

Let us follow project closure procedures to close out one of our all-year-round projects.

• • Example of Terminating Your All-year Round Projects

Realistically speaking, any of your All-year Round Projects close out just a week before 23/12/2023. As explained above, there is a procedure for terminating them. This procedure can be simple or complex depending on project. Let say, you want to finalise your Play Project. To do that, we are going to use a 8-step model of terminating a project as provided by ‘taskmanagementguide.com’ (op. cit.)

To terminate your Play Project, you need proceed with the following:

a) Close any agreements you made with any third parties (e.g., if you borrow materials from the library to research on poverty reduction performance of African countries, you need to close the given borrowing agreement by returning the materials, which can be a book, video, tape, etc.)

b) Handover responsibilities and accountabilities (i.e., transfer assignments to your play mates)

c) If you have been playing with friends and family members, you will dismiss them

d) Release the resources used (e.g., returning books to the lending library)

e) If you open a project book to record your results and accounts, you need to close it

f) Record and report your lessons learnt and experiences

g) Accept or reject your result which in this case should be the best African country poverty reducer

h) Share your result with the community and CENFACS by 23/12/2023.

The above is one of the possible ways of terminating your All-year Round Projects. For those who would like to dive deeper into Terminating their Play or Run or Vote project, they should not hesitate to contact CENFACS.

• Goals Combination: Reduction of Holiday Poverty and of Poverty as a Lack of Income Protection

Our Season’s Goal is the Reduction of Holiday Poverty or Poverty Linked to the Lack of Means to Enjoy a Decent Holiday Whether at Home or Away from Home. Our Goal for April Month of Protection is the Reduction of Poverty as a Lack of Income Protection.

This week, we are combining the two lacks as they both fall under the problem of not having or having less means to protect against loss of income and to finance holiday budget/plan. It is also the combination of efforts to find solutions to fund both protection and holiday. Both protection and holiday are basic life-sustaining goods or needs; and failure to satisfy them can be seen as an symptom or indication of poverty and financial hardship.

The above is our combined goal which we expect our supporters and audiences to support. For further details on this goals combination including its support, please contact CENFACS.

• Nature Projects and Nature-based Solutions to Poverty: Working Plan for the Second Series of Activities

This week, we are announcing the second series of activities that feature the new generation of Nature Projects and Nature-based Solutions to Poverty. The second series of these activities, which will be covered in 4 weeks in May 2023, include the following:

Activity 1: Participatory Integrated Biodiversity Inclusive Spatial Planning

Activity 2: Effective Management Processes for Land and Sea Use Change

Activity 3: Rights of Indigenous Peoples and Local Communities, and their Contributions to Nature Solutions to Poverty

Activity 4: Bringing Lost Areas of Biodiversity Close to Net Zero.

The above-mentioned activities will start from week beginning Monday 1st of May 2023. Details of each of them will be released next week. For any further information before their release, please do not hesitate to contact CENFACS.

Message in French (Message en français)

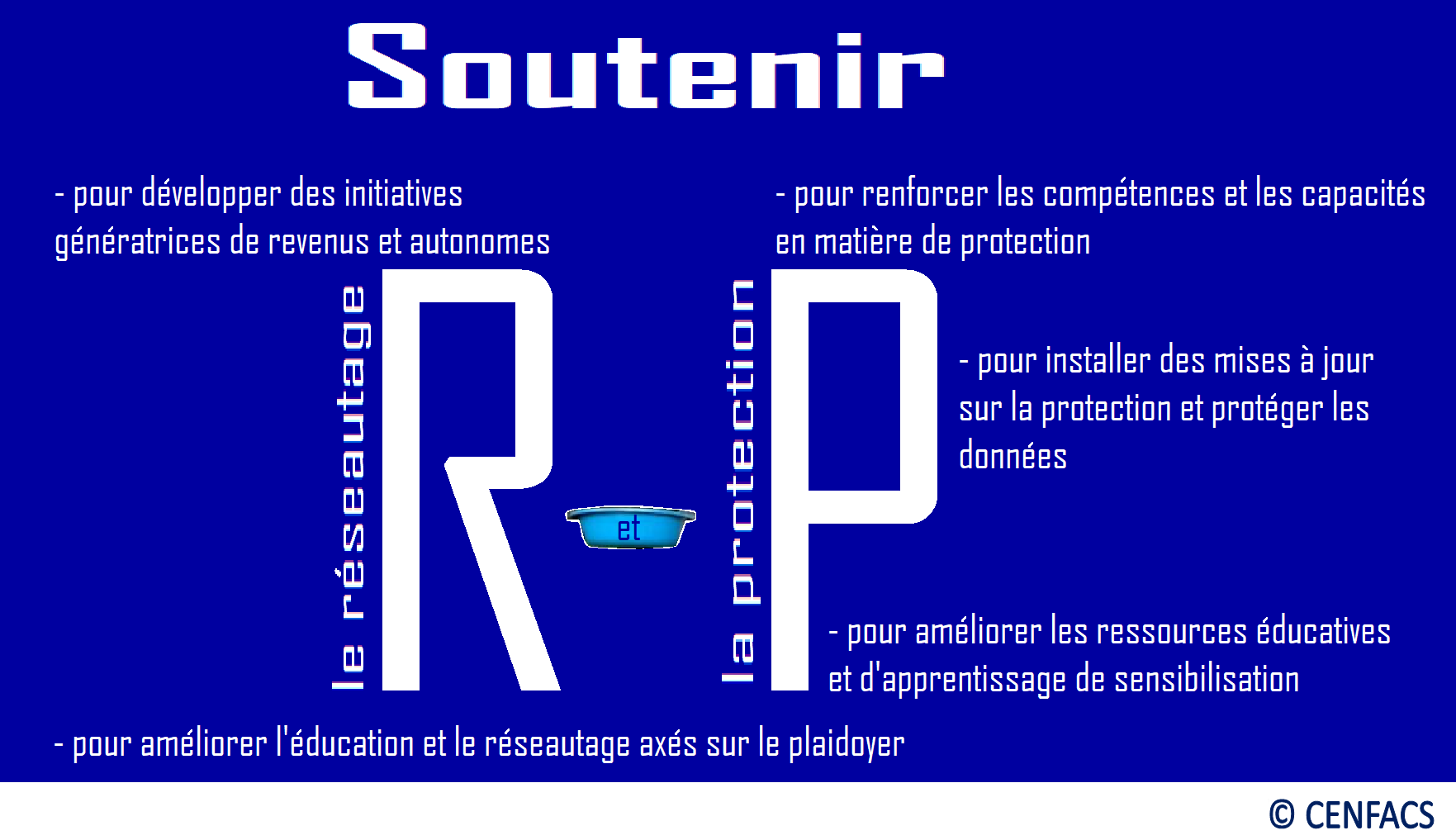

• Soutenir le réseautage et la protection contre la pauvreté en 2023

Le Mois de la Protection au sein du CENFACS est également un mois propice à la protection. C’est le mois du soutien au projet de réseautage et de protection du CENFACS. Pour soutenir, il serait mieux d’avoir une idée de ce projet.

• • Qu’est-ce que le projet de réseautage et de protection du CENFACS?

C’est une initiative de réduction de la pauvreté infantile conçue pour aider et soutenir les enfants vulnérables et pauvres contre les MÉFAITS, les MENACES et les RISQUES venant de toute forme d’exploitation, de négligence et d’abus en Afrique par l’amélioration de la circulation de l’information, le développement des connaissances, les activités d’auto-assistance, l’augmentation et la diversification des possibilités et des chances avec et au nom de ces enfants. On peut contribuer à ce projet en soutenant le réseautage et la protection contre la pauvreté en 2023?

• • Comprendre le soutien au réseautage et à la protection contre la pauvreté en 2023

Il s’agit de ce qui suit :

√ Améliorer la circulation de l’information entre les personnes et les communautés vulnérables pour lutter contre la pauvreté

√ Prévenir et répondre à toutes les formes de vulnérabilité, menaces et risques provenant d’environnements proches et mondiaux

√ Redonner du pouvoir aux personnes vulnérables en augmentant et en diversifiant les possibilités et les forces entre elles.

• • Ce que votre soutien peut accomplir

Votre soutien aidera à

√ Sensibiliser et améliorer la diffusion et la dissémination de l’information pour la lutte contre la pauvreté

√ Prévenir l’exploitation humaine (p. ex., l’exploitation des enfants) et répondre aux questions de protection et de sauvegarde de l’enfance

√ Redonner aux pauvres les moyens d’agir et de les renforcer à protéger les jeunes générations

√ Élargir et diversifier les possibilités offertes aux personnes vulnérables pour échapper à la pauvreté

√ Développer une base bien informée pour réduire les lacunes en matière d’information et d’autres types de vulnérabilités liées au manque de réseau, d’interconnexion et de protection.

• • Comment soutenir le réseautage et la protection contre la pauvreté en 2023

Vous pouvez FAIRE UN DON, PROMETTRE ET FAIRE UNE DÉCLARATION D’AIDE AU DON pour n’importe quel montant afin de soutenir le réseautage et la protection contre la pauvreté en 2023.

Pour faire un don, donner de l’aide ou soutenir différemment, veuillez contacter le CENFACS.

Vous pouvez faire un don

*par téléphone

*par e-mail

*par texte

*en remplissant le formulaire de contact sur ce site.

Dès réception de votre intention de faire un don, le CENFACS communiquera avec vous. Cependant, si vous souhaitez que votre soutien reste anonyme; Nous respecterons votre souhait.

Main Development

• FACS Issue No. 79 of Spring 2023 Titled as Financial Education, Information and Communications for and with the Poor

The contents and key summaries of the 79th Issue of FACS are given below.

• • Contents and Pages

I. Key Concepts Relating to the 79th Issue of FACS (Page 2)

II. Links between Financial Education, Financial Information and Financial Communication (Page 3)

III. Potential Beneficiaries of Financial Education, Information and Communication Making the 79th Issue (Page 3)

IV. Making Financial Information Reach the Poor in Africa (Page 3)

V. How Poor People Consume Financial Information in Africa (Page 4)

VI. What Handicaps or Prevents Poor People in Africa from Having Financial Access (Page 4)

VII. Financial Education for Female-owned Micro-enterprises in Africa (Page 4)

VIII. Les organisations sœurs basées en Afrique et leur travail pour combler les lacunes en matière d’éducation, d’information et de communication financières (Page 5)

VIX. Expériences africaines en éducation financière : les cas congolais en République Démocratique du Congo (Page 5)

X. Organisations sœurs basées en Afrique et la réduction de la pauvreté liée au manque d’éducation, d’information et de communication financière (Page 6)

XI. Les marchés de l’information financière et les pauvres en Afrique (Page 6)

XII. Survey, Testing Hypotheses, E-questionnaire and E-discussion on Financial Education, Information and Communication (Page 7)

XIII. Support, Top Tool, Information and Guidance on Financial Education, Information and Communications for the Poor (Page 8)

XIV. Workshop, Focus Group and Enhancement Activity on Financial Education (Page 9)

XV. Giving and Project (Page 10)

• • Key Summaries

Please find below the key summaries of the 79th Issue of FACS from page 2 to page 10.

• • • Key Concepts Relating to the 79th Issue of FACS (Page 2)

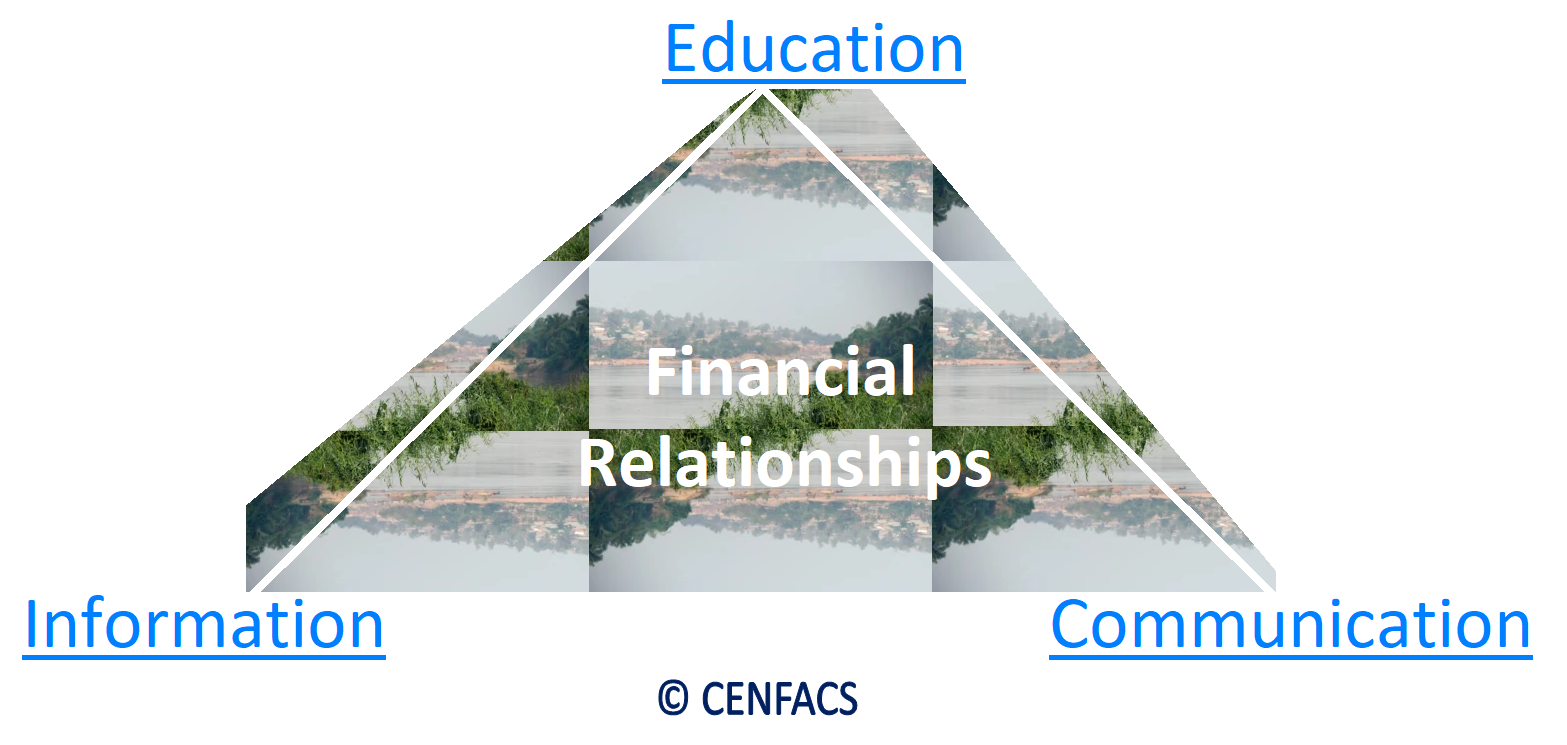

There are three financial concepts that will help the readers of FACS to better understand the contents of the 79th Issue. These concepts are financial education, financial information and financial communication. The working definitions selected for these concepts are those that can apply to the types of people listed in the 79th Issue – the poor. Let us look at each of these concepts.

• • • • Financial Education

Our working definition of financial education comes from ‘wealthdiagram.com’ (3) which states that

“Financial education is the ability to understand how financial resources work. It helps someone to manage the expenses and planning for the future. It is broad and includes financial literacy, economics and others”.

The website ‘sciencemystic.com’ (4) goes further by giving the components of financial education. According to ‘sciencemystic.com’,

“Financial education generally includes the ability to (a) manage money and assets (banking investment), credit insurance and tax (b) time value and money distribution in basic investments (c) plan, implement and evaluate financial decisions. In other words, financial education means understanding the importance of money and money use or getting information about it”.

Arguing about the status of financial education in Africa, Messy and Monticone (5) think that

“Well-designed financial education initiatives can reduce demand-side barriers to more effective financial inclusion and can empower vulnerable individuals economically so that they can better manage household resources and develop income generating activities”.

The above-mentioned definition of financial education and its elements will be applied to the poor.

• • • • Financial Information

Financial information can be perceived in many ways. To limit ourselves, we are going to refer to what ‘wallstreetmojo.com’ states about it. From the perspective of ‘wallstreetmojo.com’ (6),

“Financial information refers to information that involves money. Non-financial information is any other information that can be availed of an individual or company and is unrelated to money”.

The website ‘wallstreetmojo.com’ provides various sources of financial information which include banks, financial statements of companies, financial data, credit card statements, etc. Put it simply, for both individuals and companies, financial information is gathered in financial statements like balance sheet, profit and loss statement, cash flow statement, etc.

• • • • Financial Communication

Like financial education and information, financial communication can be approached from different perspectives. From the view of ‘scribd.com’ (7),

“Financial communication is a process whereby financial information is enclosed in a package and is channelled and imparted by a sender to a receiver via some medium. All forms of financial communication require a sender, a message, and an intended recipient, however the receiver need not be present or aware of the sender’s intent to communicate at the time of communication in order for the act of financial communication to occur. Financial communication requires that all parties have an area of communicative commonality. There are verbal means, such as speech, song, and tone of voice, and there are non verbal means through media, i.e., pictures, graphics and sound, and writing”.

Although this definition is long, it nevertheless provides a thorough understanding of financial communication. To this definition, we can add what ‘communication.iresearchnet.com’ says about financial communication in terms of its implications. The website ‘communication.iresearchnet.com’ (8) mentions that

“Financial communication entails all of the strategies, tactics, and tools used to share financial data and recommendations with investors and other interested parties”.

As one can notice, the three key concepts (i.e., financial education, financial information and financial communication) have some links or can be linked when it comes to dealing with poverty and poor people.

• • • Links between Financial Education, Financial Information and Financial Communication (Page 3)

Financial education, financial information and financial communication are the three factors or elements that can predict financial behaviour of people, and amongst these people are the poor. There could be relationship between these three factors and financial behaviour. But, reliability and validity testing needs to prove this relationship. In other words, the extent that a measurement tool measures what anyone who wants to use to measure this relationship needs to prove it.

As part of research sample on this relationship, we shall develop a questionnaire to check it amongst our community members. The evaluation of content of this questionnaire will help to prove or disprove it within our community. Perhaps, the month of creation and innovation (June 2023) will be the right one to ask our members to participate in this research.

Those members of our community who will be interested in taking part in this research and development work, they can let CENFACS know.

• • • Potential Beneficiaries of Financial Education, Information and Communication Making the 79th Issue (Page 3)

Amongst the types of people in need who could benefit from financial education, information and communication as defined above are:

√ The unbanked and those relying on cash economy

√ Those with inadequate personal finance education

√ The financially uneducated to control their finances

√ Those who cannot manage their income and expenses

√ People who need increased awareness of financial communication

√ The financially excluded

√ Those with little money which is unstable, unpredictable and hard to manage

Etc.

In short, most of the types of people mentioned above will need some form of capacity building or support to improve either their financial education or financial information or financial communication.

• • • Making Financial Information Reach the Poor in Africa (Page 3)

Making Financial Information Reach the Poor is about expanding the means to carry financial information to the poor in Africa.

One the means is mobile phone. Expanding the mobile phone usage is a way to reach them with financial information. Indeed, mobile phones can help to reduce poverty linked to the lack of financial communication means.

Another means is working with the poor to move away from cash economy to embrace digital economy. For example, at the moment many people in Africa are using account-based digital payments.

Briefly, there are sorts of initiatives that can help to carry financial information to the poor in Africa or anywhere else as well as to offer them uplifting opportunities.

• • • How Poor People Consume Financial Information in Africa (Page 4)

Like any consumer, poor people would like credible source of financial information and having clear level of assurance. For a good consumption of this financial information, it is better to have a standard, context, boundary and credibility about financial information to be consumed by them. For example, any financial reports or bills or statements need to have those features. Where there is a problem to understand the message sent, it could be a good idea to explain to the receiver the encrypted or encoded financial message.

• • • What Handicaps or Prevents Poor People in Africa from Having Financial Access (Page 4)

Financial education, information and communication play a vital role in most people’s lives. Lacking a bank account, financial services, financial products (like insurance, savings products and pensions) can result in financial exclusion. Therefore, working with the poor so that they can have financial education, information and communication will enhance their financial access. As Julie Birkenmaier et al. (9) put it in the Encyclopaedia of Social Work,

“Financial inclusion, the goal of financial access, broadly refers to the ability of all people in a society to access and be empowered to use safe, affordable, relevant, and convenient financial products and services for achieving their goals”.

The types of beneficiaries of the 79th Issue of FACS may not have this access or power. That is why some efforts can be done to remove barriers to financial access.

• • • Financial Education for Female-owned Micro-enterprises in Africa (Page 4)

As part of gender equality and women’s empowerment in Africa, promoting financial education, information and communication for women who are engaged in income-generating activities to reduce poverty can be a positive drive. In this respect, improving the attainment in financial education for those women entrepreneurs would not only help them but also their family and community. This type of financial inclusion of women can have other positive effects such as improvement of productivity for their micro-enterprises and the economy in which they are working.

• • • Les organisations sœurs basées en Afrique et leur travail pour combler les lacunes en matière d’éducation, d’information et de communication financières (Page 5)

Depuis le début des années 1990, lorsque l’éducation financière (en particulier la littératie financière) a fait ses débuts dans les politiques de développement, nous voyons de plus en plus d’organisations en Afrique travailler pour aider leurs membres et les populations locales à acquérir des connaissances dans ce domaine. Les organisations sœurs basées en Afrique qui travaillent avec le CENFACS ont également emboîté le pas.

Nos organisations sœurs encouragent les peuples autochtones à acquérir des connaissances financières non seulement pour gérer leur vie respective, mais aussi pour comprendre le cadre financier dans lequel ils vivent et opèrent quotidiennement ainsi que l’avalanche d’informations financières qui abondent dans les nouvelles. Ces connaissances leur permettent de tenir un compte familial, de comprendre les changements financiers tels que le taux de change, les fluctuations de la monnaie locale, le taux d’intérêt, le taux d’épargne, etc., et comment ces facteurs ou variables économiques et financiers affectent leur vie.

Cependant, ces organisations ont des limites de capacité. Cela étant dit, elles ont besoin de soutien pour poursuivre leur mission d’éducation, d’information et de communication financière auprès des populations locales.

• • • Expériences africaines en éducation financière : les cas congolais en République démocratique du Congo (Page 5)

Il existe plusieurs cas ou expériences relatifs à l’éducation financière en Afrique. Ce sont des cas ou des expériences de croissance inclusive, équitable et durable en Afrique.

Dans le cadre de ce 79ème numéro de FACS, nous voulons évoquer les trois cas congolais suivants:

σ Le Fonds pour l’inclusion financière en République Démocratique du Congo (FPM)

σ Le Programme d’Education Financière et Numérique (PEFD)

σ Le Programme National d’Education Financière (PNEF) qui a été mis en place en 2016 par la Banque Centrale du Congo.

Comme le montrent les documents publiés par ces programmes et fonds, ces initiatives ont des objectifs communs qui incluent de doter les populations congolaises locales des connaissances, des compétences et de la confiance nécessaires à une gestion optimale de leurs finances; de soutenir le taux d’inclusion financière; de promouvoir l’adoption des moyens de paiement existants sur le marché, etc. Ces initiatives permettent non seulement de sensibiliser et de former les populations à la gestion de leurs finances, mais aussi de soutenir ces mêmes populations avec des outils pour réduire la pauvreté et la précarité.

Pour plus d’informations sur ces initiatives, il serait préférable de les consulter.

• • • Organisations sœurs basées en Afrique et la réduction de la pauvreté liée au manque d’éducation, d’information et de communication financière (Page 6)

Travailler avec les populations locales pour acquérir des compétences, de l’information et des communications; c’est une chose. Aider ces mêmes populations à sortir de la pauvreté, c’est autre chose.

Nos organisations sœurs basées en Afrique travaillent avec leurs adhérents pour que ceux-ci deviennent capables de lire et de comprendre l’information financière. Ce travail permet à leurs adhérents ou bénéficiaires de réduire une partie de leurs problèmes. Être capable de lire, de comprendre et de communiquer des informations financières apporte plus à ces personnes. Néanmoins, cela peut ou ne pas suffire à réduire réellement la pauvreté.

C’est pourquoi nos organisations sœurs tentent d’aller au-delà en travaillant davantage avec leurs bénéficiaires afin de trouver de vraies solutions contre la pauvreté. Pour y parvenir, elles ont besoin de soutien car elles fonctionnent avec des moyens très limités; les moyens qui ont été parfois détruits par les polycrises (c’est-à-dire la crise du coût de la vie, la pandémie de coronavirus, la crise climatique et d’autres crises en Afrique). Les aider financièrement à continuer leur travail sera un grand salut.

• • • Les marchés de l’information financière et les pauvres en Afrique (Page 6)

Comme tout marché, les marchés de l’information financière répondent à la loi de l’offre et de la demande. Et ceux ou celles qui ont les moyens de payer les prix du marché ont plus de facilités pour accéder à l’information qu’ils/elles veulent. Ceux ou celles qui n’ont pas de moyens comme les pauvres ne peuvent pas s’attendre au même type et à la même qualité d’information que les autres.

L’information financière ne fait pas exception à cette règle du jeu économique. L’information financière circule souvent entre ceux/celles qui la fournissent et ceux/celles qui la consomment. Ceux/celles qui produisent ou fournissent l’information sont, par exemple, les banques, les gestionnaires, les institutions financières, les compagnies d’assurance, les caisses d’épargne, la presse, etc. Ces acteurs/actrices transmettent ou font circuler des informations financières.

En raison de très faibles moyens, les ménages pauvres n’ont souvent pas la possibilité de consommer un certain type d’informations qui peuvent être vitales pour peser sur la balance. Ce manque de consommation d’information peut perpétuer la pauvreté dans la mesure où ils ont l’objet de ce manque. Et pourtant, en veillant à ce que les pauvres fassent partie intégrante des marchés de l’information, cela peut avoir des effets bénéfiques sur eux et améliorer leurs conditions de vie.

En gros, si l’on veut réduire la pauvreté liée au manque d’information, il y a lieu de faire en sorte pour les pauvres ne soient pas marginalisés dans les marchés de cette information.

• • • Survey, Testing Hypotheses, E-questionnaire and E-discussion on Financial Education, Information and Communication (Page 7)

• • • • Survey on the impact of geographical factors and cultural barriers to financial education, information and communication

The purpose of this survey is to collect information from a sample of our user households regarding the impact of geographical factors and cultural barriers to financial education, information and communication.

Participation to this survey is voluntary.

As part of the survey, we are running a questionnaire which contains some questions. Three of these questions are:

√ How can geographical factors (like living in remote areas) and cultural barriers (such as family customs) contribute to the lack of or less financial education?

√ How can geographical factors (like living in remote areas) and cultural barriers (such as tribe customs) contribute to the lack of or less financial information?

√ How can geographical factors (like living in remote areas) and cultural barriers (such as ethnic group customs) contribute to the lack or less financial communication?

You can respond and directly send your answer to CENFACS.

• • • • Testing Hypotheses about causal relationships between the access to and use of financial education, information and communication on one hand; and poverty reduction on the other hand

For those of our members who would like to dive deep into the impact of financial education, information and communication on poverty reduction, we have some educational activities for them. They can test the inference of the following hypotheses:

a.1) Null hypothesis (Ho): There is a relationship between financial education and poverty reduction

a.2) Alternative hypothesis (H1): There is not a relationship between financial education and poverty reduction

b.1) Null hypothesis (Ho): There is a positive relationship between financial information and poverty reduction

b.2) Alternative hypothesis (H1): There is not positive relationship between financial information and poverty reduction

c.1) Null hypothesis (Ho): There is a positive relationship between financial communication and poverty reduction

c.2) Alternative hypothesis (H1): There is not a positive relationship between financial communication and poverty reduction.

In order to conduct these tests, one needs data on financial education, information and communication about a particular population or community.

• • • • E-question about experience sharing on financial education

Does financial education improve your ability to apply financial skills (like financial literacy and numeracy skills) in real life? Please tick (√) as appropriate.

YES [ ]

NO [ ]

If your answer is YES, please share your experience with CENFACS and others within the community.

If your answer is NO, CENFACS can work with you via its Advice-giving Service (service which we offer to the community for free) to find way forward to apply your financial education or skills in real life.

• • • • E-discussion on the effects of financial education, information and communication on financial wellbeing

Some of the people making our community are or get financially educated. Others are financially informed. Others more are equipped with financial communication. Does being financially educated or being financially informed or being equipped with means of financial communication grow financial wellbeing?

For those who may have any views or thoughts or even experience to share with regard this matter, they can join our e-discussion to exchange their views or thoughts or experience with others.

To e-discuss with us and others, please contact CENFACS.

• • • Support, Top Tool, Information and Guidance on on Financial Education, Information and Communication for the Poor (Page 8)

• • • • Ask CENFACS for Support regarding financial education, information and communication

For those members of our community who would like to improve their financial education or financial information or financial communication but they do not know how to improve them, CENFACS can work with them to explore ways of doing it.

We can work with them under our Advice-, Guidance- and Information-giving Service as well as through various financial campaigns we run (like Zero Income Deficit, Financial Controls, etc.) and our tools box of poverty reduction. Our support will help them to make good financial decisions such as investment decision, credit decision, saving decision, tax decision, etc.

If you are a member of our community, you can ask us for basic support regarding the problems you have to improve your financial education, information and communication.

• • • • Top Tool of the 79th Issue of FACS: Young Persons’ Money Index

One of the tools we find that could be useful for our community members is Young Persons’ Money Index. What is it?

The London Institute of Banking and Finance (10) states that

“Young Persons’ Money Index is an annual survey that tracks the take-up of financial education in UK schools”.

In other words, this index examines the delivery of financial education in schools and the financial capability of young people in the UK. This tool can help find the experiences of surveyed people regarding financial education matters such as feeling about money, learning about money, access to financial education, receiving financial information, etc.

For example, research found that 68% of young people surveyed said their financial understanding and knowledge mainly come from their parents, according to March 2023 news from the London Institute of Banking and Finance (11).

Those of members of our community who would like to gain more insight into about the index, they can find a lot of information online about it. Those who would like to discuss the relevancy of this tool and its application, they can feel free to contact CENFACS.

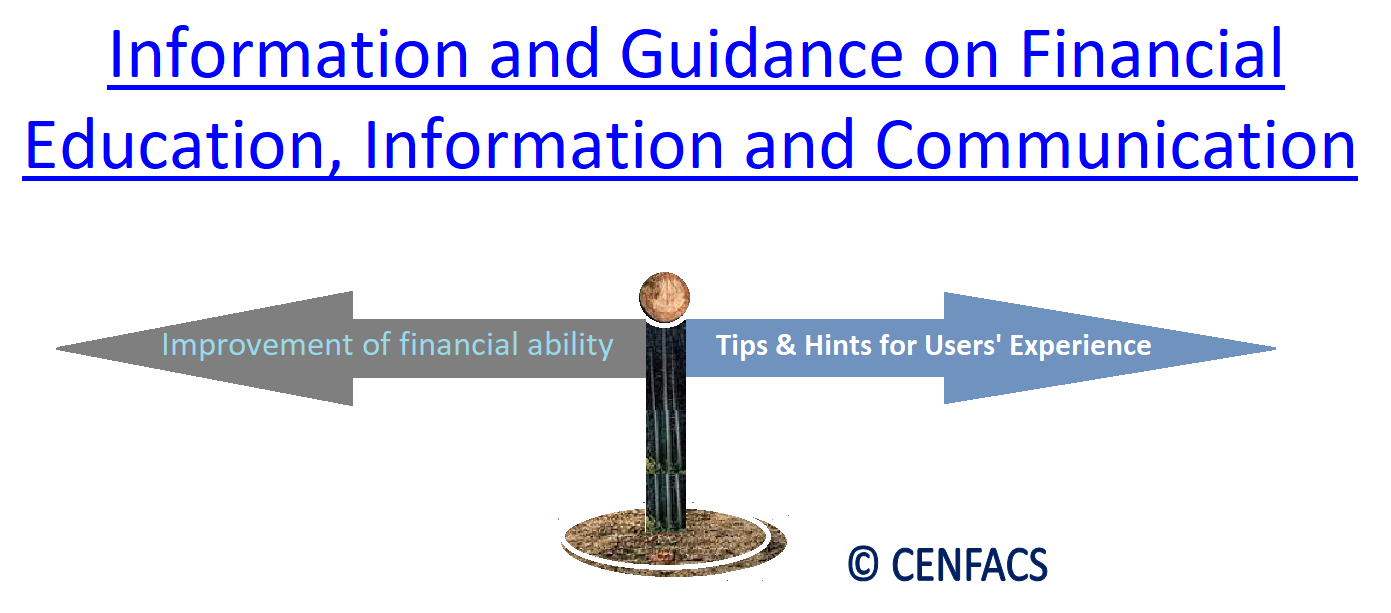

• • • • Information and Guidance on Financial Education, Information and Communication for the Poor

Information and Guidance include two types areas of support via CENFACS, which are:

a) Information and Guidance on financial education and training

b) Tips and hints to improve users’ experience about financial information and communication

• • • • • Information and Guidance on ways of improving and developing via financial training and education

Financial Training and education can enhance beneficiaries’ financial skills (like financial numeracy and literacy skills).

Those members of community who are looking for financial training and education and who do not know what to do, CENFACS can work with them (via needs assessment) or provide them with leads about organisations that can help them.

• • • • • Tips and hints to improve users’ experience about financial information and communication

For those who need some tips and hints to improve their experience about financial information and communication, we can provide this support via a number of services and activities we run. Our financial campaigns (like Financial Controls) and resources (such as Summer Financial Updates) will help them.

More tips and hints relating to the matter can be obtained from CENFACS‘ Advice-giving Service.

Additionally, you can request from CENFACS a list of organisations and services providing help and support in the area of financial information and communication for the poor, although this Issue does not list them. Before making any request, one needs to specify the kind of organisations they are looking for.

To make your request, just contact CENFACS with your name and contact details.

• • • Workshop, Focus Group and Enhancement Activity about Financial Education (Page 9)

• • • • Mini Themed Workshop

Boost your knowledge and skills about financial education via CENFACS. The workshop aims at supporting those without or with less financial education gain the skills make responsible financial decisions and own financial choices, to improve their ability to manage money and assets.

To enquire about the boost, please contact CENFACS.

• • • • Focus Group on the Promotion of Financial Education within the Community

You can take part in our focus group on ways of encouraging needy people to learn and know about financial products available for them and adopt them as their way of living.

To take part in the focus group, please contact CENFACS.

• • • • Spring Financial Confidence Building Activity

This user involvement activity revolves around the answers to the following questions:

σ How confident are you with the financial educational skills you possess, financial information you receive and financial communication you have to deal with any economic hardship issues?

σ How do many of you feel confident in their financial knowledge?

σ How do many of you turn to financial professionals for financial guidance?

σ How do many of you understand the basic financial principles?

Those who would like to answer these questions and participate to our Spring Financial Confidence Building Activity, they are welcome.

To take part in this activity, please contact CENFACS.

• • • Giving and Project (Page 10)

• • • • Readers’ Giving

You can support FACS, CENFACS bilingual newsletter, which explains what is happening within and around CENFACS.

FACS also provides a wealth of information, tips, tricks and hacks on how to reduce poverty and enhance sustainable development.

You can help to continue its publication and to reward efforts made in producing it.

To support, just contact CENFACS on this site.

• • • • Financial Education, Information and Communication Project (FEICP)

FEICP, which is a basic financial capacity building initiative, aims at reducing poverty linked to the lack of financial education, information and communication in Africa. FEICP will help to reach those who are financially uneducated or less educated, uninformed or less informed and lacking financial communication or with less financial communication.

Through this project, it is hoped that beneficiaries will improve their financial skills, knowledge and wellbeing. They will also enhance their means of living and enterprise so that they can increase the way contribute in their community or society.

To support or contribute to FEICP, please contact CENFACS.

For further details including the implementation plan of the FEICP, please contact CENFACS.

The full copy of the 79th Issue of FACS is available on request.

For any queries and comments about this Issue, please do not hesitate to contact CENFACS.

_________

• References

(1) www.taskmanagementguide.com/glossary/what-is-project-termination-.php (Accessed in April 2023)

(2) https://www.pmi.org/learning/library/project-termination-delay-1931 (Accessed in April 2023 )

(3) https://wealthdiagram.com/finance/whats-the-difference-between-financial-education-and-financial-literacy# (Accessed in April 2023)

(4) https://sciencemystic.com/what-is-financial-education/ (Accessed in April 2023)

(5) Messy, F. and Monticone, C. (2012), The Status of Financial Education in Africa, OECD Working Papers on Finance, Insurance and Private Pensions, No. 25, OECD Publishing

(6) https://www.wallstreetmojo.com/financial-information/ (Accessed in April 2023)

(7) https://www.scribd.com/document/2922625433/What-is-Financial-Communication# (Accessed in April 2023)

(8) communication.iresearchnet.com/strategic-communication/financial-communication/ (Accessed in April 2023)

(9) https://oxfordre.com/socialwork/display/… (https://doi.org/10.1093/acrefore/9780199975839.013.1331 (Accessed in April 2023)

(10) https://libf.ac.uk/study/financial-education/young-persons-money-index (Accessed in April 2023)

(11) https://www.libf.ac.uk/news-and-insights/news/detail/2023/03/10/demand-for-financial-education-in-schools-jumbs-by-10 (Accessed in April 2023)

_________

• Help CENFACS keep the Poverty Relief work going this year

We do our work on a very small budget and on a voluntary basis. Making a donation will show us you value our work and support CENFACS’ work, which is currently offered as a free service.

One could also consider a recurring donation to CENFACS in the future.

Additionally, we would like to inform you that planned gifting is always an option for giving at CENFACS. Likewise, CENFACS accepts matching gifts from companies running a gift-matching programme.

Donate to support CENFACS!

FOR ONLY £1, YOU CAN SUPPORT CENFACS AND CENFACS’ NOBLE CAUSES OF POVERTY REDUCTION.

JUST GO TO: Support Causes – (cenfacs.org.uk)

Thank you for visiting CENFACS website and reading this post.

Thank you as well to those who made or make comments about our weekly posts.

We look forward to receiving your regular visits and continuing support throughout 2023 and beyond.

With many thanks.