Welcome to CENFACS’ Online Diary!

30 October 2024

Post No. 376

The Week’s Contents

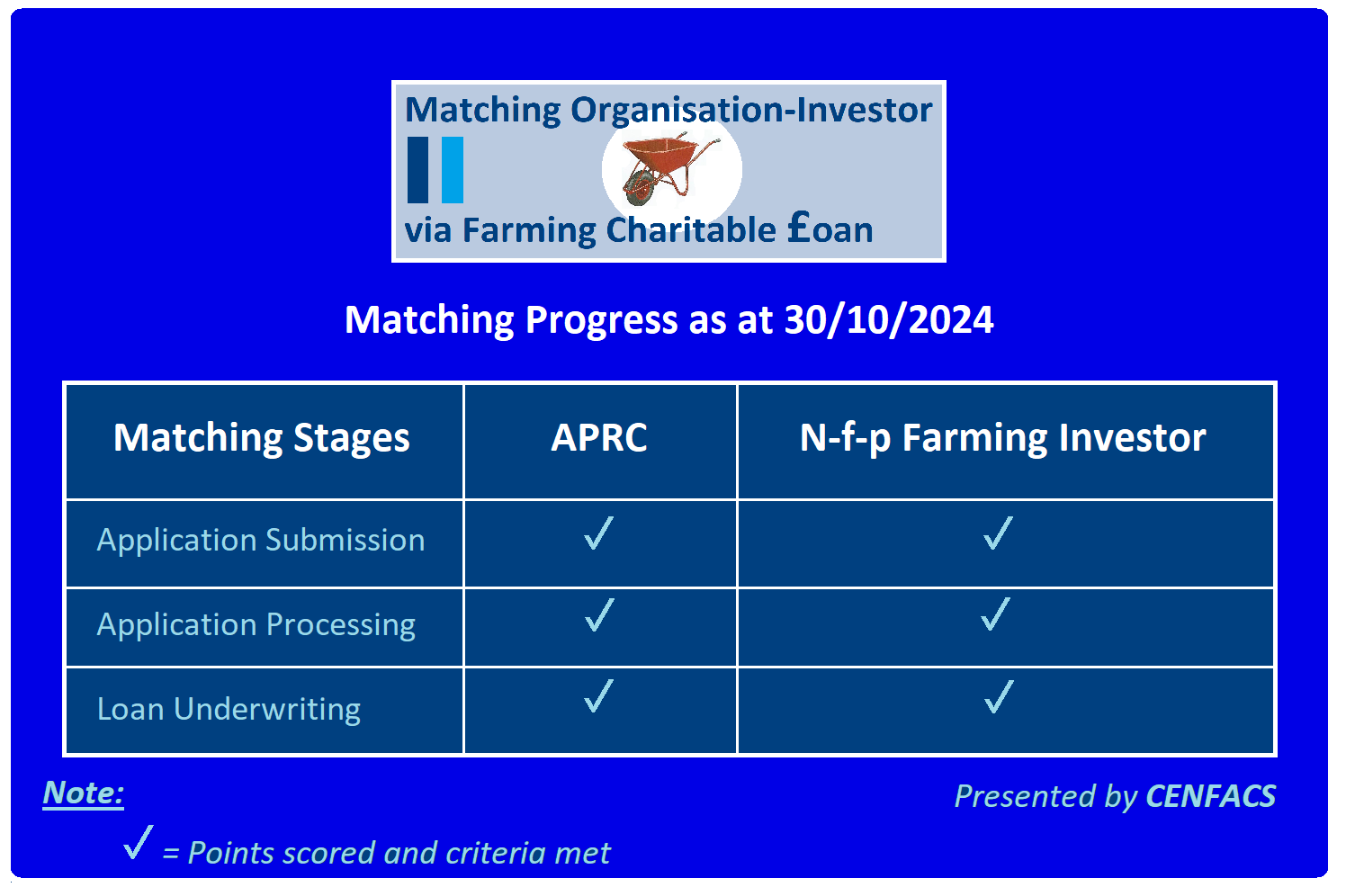

• Autumn Matching Organisation-Investor via Farming Charitable Loan – Match Period 30/10/2024 to 05/11/2024: Matching Organisation-Investor via Loan Disbursement (Stage 4)

• African Pension Fund Manager Project

• Rescuing Children’s Education in Africa

… And much more!

Key Messages

• Autumn Matching Organisation-Investor via Farming Charitable Loan – Match Period 30/10/2024 to 05/11/2024: Matching Organisation-Investor via Loan Disbursement (Stage 4)

Both African Poverty Relief Charity (APRC) and Not-for-profit (n-f-p) Farming Investor (FI) agreed on APRC’s loan approval steps. In other words, they agreed on how APRC will review the borrower’s application, credit history, income, and other loan determining factors. This agreement means that they can move to the next stage, which is Stage 4.

Stage 4, which is the last one, is Farming Charitable Loan Disbursement. Perhaps, the best way of introducing this last Stage of our Autumn Matching Organisation-Investor via Farming Charitable Loan is to explain loan disbursement.

Loan disbursement is simply, according to the website ‘financefuturists.com’ (1),

“When you receive the approved loan amount from your lender, allowing you to access the funds you need”.

In the context of our matching programme, the lender is APRC and money receivers or borrowers are those members of APRC who will apply for a loan to APRC.

Knowing what business loan disbursement is, both parties (i.e., APRC and n-f-p FI) are expected to well perform during this last opportunity of the matching talks. Before entering the negotiations, let us restate the aim of this project and recall the key matching points.

• • The Aim of Matching Organisation-Investor via Farming Charitable Loan

The main aim of this project is to reduce poverty (among local poor farmers, businesses and people) through the provision of small charitable loans to small to medium-sized farming activities or businesses in Africa.

There are guiding or matching principles to achieve the above stated aim.

• • Key Matching Points

The two parties (i.e., APRC and N-f-p FI) need to remember the following key matching points:

σ The loan, that APRC will provide, will be a flexible farming finance in the form of cash injection to small and medium-sized farming activities or businesses for equipment growth, expansion and cash flow

σ APRC’s loans will be flexible ones at concessional/social rates (that is, short-term loans with less interest to pay)

σ Loans, which could be between £100 and £2,000, will help to buy agricultural equipment or investment in a new farming initiative/venture

σ The loan will be made with the view that there will be financial benefit and charitable benefit for APRC while charitable benefit superseding financial benefit

σ The borrower will use the funds for their intended purpose only

σ N-f-p FI would like to see the farming business or activity is a profitable one so that it can achieve its goal of reducing poverty by raising money for it through farming trading.

After recalling the main aim of this project and its essential matching points, APRC and N-f-p FI can start the fourth round of negotiations.

To reach an agreement at the end of this Stage 4, there should not be any stumbling blocks or sticking points. If there is, then there must be resolved. Where the two (i.e., investee and investor) need support, CENFACS will work with each party to fill the gap.

More details about Stage 4 can be found under the Main Development section of this post.

• African Pension Fund Manager Project

To explain this project, let us first define it.

• • What Is African Pension Fund Manager (APFM)?

The starting point in this definition is to explain ‘pension fund manager’. The website ‘lawinsider.com’ (2) explains it by arguing that

“Pension fund manager means the person(s) appointed by the Directors to invest the whole or part of the assets of the scheme in accordance with such terms and conditions of service as may be specified in the instrument of appointment”.

This definition can apply to APFM with similarities and difference. The difference is that APFM will work with African charities based in Africa.

• • What Is African Pension Fund Manager (APFM) Project?

As a project, APFM is an initiative that consists of investing the contributions received, accumulating them, administrating the funds, developing pension policies and pension and benefits packages, reviewing, discussing and agreeing fund strategy and structure with African Charities.

To understand this project, let us briefly present its aim, the role of African Pension Fund Manager (APFM), APFMP outcomes and APFMP funding needs.

• • • The aim of APFMP

The real aim of this project is to reduce and possibly end pension poverty or old age poverty amongst African charities’ employees in Africa. To achieve this aim, someone has to carry out the function of African pension fund management.

• • • The role of APFM

APFM will be mainly responsible for managing and investing African charities’ funds in securities and investment policies. He/she will collect money from African charities and their employees to fund employee retirement obligations. He/she will keep an eye on long-term growth of capital to support the needs of future retirees as the cost of living increases over their working lives.

APFM will work across African charities to support them meet and implement their pension fund management strategy and aim, while contributing to their goal of reducing pension poverty or old age poverty among their users and workers. In its role, he/she will undertake some duties such as

σ help increase assets in African charity pension funds which are smaller compared to those of the rest of the world

σ encourage long-term (retirement) savings

σ create facilitative policies to support appropriate deployment and investment of the pension assets into the charity pensions sector

σ work with pension sectors across Africa to resolve common problems in Africa’s charity pension sector

σ run a programme, fund or scheme which will provide retirement income for African charities involved in

σ oversee day-to-day pension fund management and administration of the funds

σ develop pensions policies and pensions and benefits packages

σ review, discuss and agree fund strategy and structure with the boards of African charities, investment and fund managers within the African charity pension sector

etc.

Because there are some aspects of investment and assets management in the definition of pension fund management, our APFM will deal with these aspects in his/her role; aspects like overseeing and making decisions about investments in a charity portfolio or fund.

• • • APFMP outcomes

As a result of the implementation of APFMP, the following changes and effects may happen:

√ An increase in pensions coverage and assets under management of the charity sector in Africa

√ Reduction of pension poverty and old-age poverty amongst African charities employees

√ Better support to pension regulatory and statutory frameworks in Africa

√ Promotion of best-practice pensions and best asset allocation across the charity pension sector

etc.

• • • APFMP funding needs

According to ‘glassdor.co.uk’ (3),

“The estimated total pay for a Pension Fund Manager is £179,264 per year, with an average salary of £109,857 per year. The estimated additional pay is £69,407 per year. Additional pay could include cash bonus, commission, tips, and profit sharing”.

The above pay package relates to the situation in the for-profit sector. Because we are in the charity sector, the above pay and benefits can be lower. Also, the pay and benefits can be different for those working with African charities.

Nevertheless, this pay package expressed in terms funding needs for APFM is what is required to be raised in order to deliver this project as it is unfunded.

For those who would like to fund this project or to help CENFACS hire a Pension Fund Manager to work with African charities, they can fund it in the region of stated amount or contribute to it. They can also have in their mind the recruitment costs which are part the fundraising of this project.

To support or contribute to APFMP, please contact CENFACS.

For further details including the implementation plan of the APFMP, please also contact CENFACS.

• Rescuing Children’s Education in Africa

The United Nations Children’s Fund (4) notes that

“Millions of children across Africa still lack access to schooling due to ongoing conflicts across the continent… In West and Central Africa alone, more than 14,000 schools are closed mainly due to conflict, affecting 2.8 million children”.

As a way of keeping education alive for these unfortunate children living in those parts of Africa in conflict or crisis (like in the Democratic Republic of Congo, Central African Republic, Burkina Faso, Mali, Niger, etc.), many types of initiatives have been so far taken to support these children.

These initiatives have been carried out by organisations (such as the United Nations Children’s Fund) and people like you to help. Initiatives such as education by radio programme, back-to-school advocacy, delivery of school kits, etc. have been taken.

However, due to the immense educational challenge posed by the legacies of conflict, insecurity and violence; there is still a deep, intense and urgent educational need in many of these areas/parts of Africa.

This appeal, which is worded as or used the slogan ‘EVERY CHILD HAS RIGHT TO EDUCATION in Conflict Zones in Africa’ (in short: EVERY CHILD HAS RIGHT TO EDUCATION), has already started and will make CENFACS‘ fundraising campaign for Giving Tuesday on 03 December 2024.

We would like people who may be interested in our philanthropic mission to join us in this campaign to Rescue Children’s Education in Africa.

We are asking to those who can to support these Educationally Needy Children via this campaign not to wait the Giving Tuesday on 03 December 2024.

They can donate now since the needs are urgent and pressing.

To donate, please get in touch with CENFACS.

Extra Messages

• “A la une” (Autumn Leaves of Action for the Upkeep of the Nature in Existence) Campaign and Themed Activities – In Focus for Week Beginning 28/10/2024: Preserving Haplochromis Granti

• Nature Projects, Nature-based Solutions to Poverty and the 16th Meeting of the Parties to the United Nations Convention on Biological Diversity

• Guidance Service about the Reduction of Pension/Old Age Poverty via Pension Fund Management

• “A la une” (Autumn Leaves of Action for the Upkeep of the Nature in Existence) Campaign and Themed Activities – In Focus for Week Beginning 28/10/2024: Preserving Haplochromis Granti

To help Preserve Haplochromis Granti, we have composed our note around the following headings:

σ What is Haplochromis Granti?

σ The conservation status of Haplochromis Granti

σ What can be done to Preserve Haplochromis Granti.

In addition, we shall provide the themed activity we have planned for this week. This themed activity is a case study on Sustainable Fishing.

Let us look at each of the headings making this note.

• • What Is Haplochromis Granti?

There is more that can be said about Haplochromis Granti. Let us simply refer to what ‘ptes.org’ (5) states about it, which is

“Haplochromis Granti is cichlid fish only only found in Lake Victoria”.

Like other species, Haplochromis Granti is experiencing life-saving conservation issues as its status indicates.

• • The Conservation Status of Haplochromis Granti

According to the same ‘ptes.org’, urgent conservation is needed to save Haplochromis Granti, which is critically endangered species. One of threats to Haplochromis Granti is Nile perch – a piscivorous (fish-eating) fish introduced to Lake Victoria in the 1960s.

There is a need to conserve or preserve Haplochromis Granti.

• • What Can Be Done to Preserve Haplochromis Granti

To preserve Haplochromis Granti, one may need to know what is to preserve a species. To preserve a species is to keep or maintain it in an unaltered condition, according to Chris Park (6)

For example, ‘ptes.org’ (op. cit.) runs a conservation project which includes the following activities:

σ establishment of fish conservation zones

σ keeping genetic diversity of the captive fish population varied

σ increase in the species resilience against the Nile perch

etc.

This project and other ones try to conserve Haplochromis Granti.

Other initiatives could include:

σ Engaging stakeholders on the conversation and preservation matters relating to Haplochromis Granti

σ Designing conservation strategy to protect it

σ Raising awareness or educating people around the issue that Haplochromis Granti faces

σ Promoting better human-fish relationships through sustainable fishing, which could be benefitial for Haplochromis Granti

σ Prevention of water pollution

σ Getting involved in Haplochromis Granti cause or fish causes

etc.

Besides that, one can donate to causes relating to the preservation of Haplochromis Granti.

The above actions are the few ones. There is more that can be done to preserve Haplochromis Granti. To stay within the scope of this note, we can limit ourselves to the above-mentioned actions or steps to Preserve Haplochromis Granti.

• • Add-on Activity of the Week’s Campaign: A Case Study on Sustainable Fishing

The fish themed activity of this week is to provide a case study about Sustainable Fishing or Sustainable Management of Fishes. To introduce this case study, let us briefly explain sustainable fishing.

• • • What is sustainable fishing?

Amongst the explanations of sustainable fishing is the one provided by ‘msc.org’ (7), which states that

“Fishing is sustainable if it leaves enough fish in the oceans and minimises impacts on habitats and ecosystems”.

From this definition, one can check from their own experience what kinds of fishing practices that are unsustainable and what can be done to stop them. Kinds of unsustainable fishing practices could include overfishing, unregulated fishing activities, etc.

This understanding of sustainable fishing can help build a compelling case study.

• • • What is a case study on sustainable fishing?

The case study will be a detailed study on sustainable fishing or any aspects of sustainable fishing.

For example, one could follow the development of sustainable fishing and build their case study. The case study evaluation will help to know what has worked so far with sustainable fishing and what can be changed or improved in the conservation of fishes.

The case study on sustainable fishing will include the following elements:

the synopsis about sustainable fishing, summary of your task, findings about sustainable fishing, the summary of the main issue, conclusion and recommendations to preserve fishes.

Briefly, your case study will be a research project to generate in-depth understanding of the issue of sustainable fishing. This type of case study will help increase understanding not only on sustainable fishing, but in fish conservation.

Do you have a case study on sustainable fishing?

If you do, please do not hesitate to share the story about it.

To find out more about the entire “A la une” Campaign and Themed Activities, please communicate with CENFACS.

• Nature Projects, Nature-based Solutions to Poverty and the 16th Meeting of the Parties to the United Nations Convention on Biological Diversity

This week, we are following the work of the United Nations Biodiversity COP16 (8), which is the 16th meeting of the parties to the United Nations Convention on Biological Diversity. The meeting aims to implement the Kunming-Montreal Global Biodiversity Framework (KMGBF).

This year’s theme of COP16, which is held from 21 October to 01 November in Cali, Colombia, is “Peace with Nature”. The goal of COP16 is to develop an implementation plan for the KMGBF.

We are following COP16 since the new/last version of CENFACS’ Nature Projects derived from the KMGBF. COP16 is important for the next development of CENFACS’ Nature Projects. We are wondering how the plans of action from the delegates (to commit themselves to 30% of land and sea to be safely protected, usage to be reduced and harmful environmental subsidies to be changed) will impact CENFACS’ Nature Projects.

These nature pledges from the delegates can affect CENFACS’ Nature Projects. They can affect our projects on matters such as indigenous communities, biodiversity aid, biodiversity protection, etc.

Additionally, CENFACS “A la une” ((Autumn Leaves of Action for the Upkeep of the Nature in Existence) Campaign and Themed Activities are linked with many of the goals of KMGBF.

Furthermore, following COP16 is not only about Nature Projects or “A la une” Campaign we run. It is also and foremost about its impact on humans. As the ‘globalmanprize.org’ (9) puts it,

“COP16 is about our interconnected relationship with nature. It is about protecting endangered species. Consider the fisheries sector where 60 million jobs globally are tied to fishing and fish farming”.

For those who would like to know more about the relationship between COP16 and CENFACS‘ Nature Projects (and Nature-based Solutions to Poverty), they can contact CENFACS.

For those who are interested in working with CENFACS on this relationship, they can also communicate with CENFACS.

• Guidance Service on the Reduction of Pension/Old Age Poverty via Pension Fund Management

As an extension from the contents of the last Issue (Issue No. 85) of FACS, CENFACS‘ bilingual newsletter, which was titled as ‘Pension Fund Management and Poverty Reduction in Africa by African Charities‘, we are organising a Guidance Service on the Reduction of Pension/Old Age Poverty. The service is for Africa-based Sister Organisations and their representatives looking for guidance to develop and implement poverty reduction strategies relating to the reduction of pension poverty and/or old-age poverty.

Indeed, pension fund management can help generate additional income and profit by investing in financial securities, government fixed-interest bonds, stocks, shares and property bonds. This income generation can help narrow the wealth gap and build generational wealth to escape from intergenerational pension/old age poverty.

For those Africa-based Sister Organisations that would like to find out how they can align their pension fund management goals with their goals of pension/old age poverty reduction, they can contact CENFACS.

CENFACS can work with them to explore ways of aligning the two goals with their mission.

We can work with them under our International Advice-, Guidance- and Information-giving Service.

Under our International Advice-, Guidance- and Information-giving Service, we can advise them on the following matters:

√ Capacity building and development

√ Project planning and development

√ Poverty reduction within the context of Africa Continental Free Trade Area

√ Not-for-profit investment and development

√ Absorption capacity development

√ Fundraising and grant-seeking leads

√ Income generation and streams

√ Sustainable development

√ Not-for-profit investment and impact investing

√ Monitoring and evaluation

Etc.

Where our capacity to advise is limited, we can refer and or signpost them to relevant international services and organisations. We can as well signpost them to organisations working on charity pension fund management and pension/old age poverty.

This advisory support for Africa-based Sister Organisations is throughout the year and constituent part of our work with them.

To access advice services, please contact CENFACS. To register for or enquire about advice services, go to www.cenfacs.org.uk/services-activities.

Message in French (Message en français)

• Le Service d’Orientation sur la Réduction de la Pauvreté des Pensions et des Personnes Âgées par la Gestion des Fonds de Pension

Dans le prolongement du contenu du dernier numéro (numéro 85) de FACS, le bulletin d’information bilingue du CENFACS, qui s’intitulait «Gestion des Fonds de Pension et Réduction de la Pauvreté en Afrique par les Organisations Caritatives Africaines», nous organisons un service d’orientation sur la réduction de la pauvreté des pensions et des personnes âgées. Le service s’adresse aux Organisations Sœurs Basées en Afrique et à leurs représentant(e)s à la recherche de conseils pour élaborer et mettre en œuvre des stratégies de réduction de la pauvreté liées à la réduction de la pauvreté des pensions et/ou de la pauvreté des personnes âgées.

En effet, la gestion des fonds de pension peut contribuer à générer des revenus et des bénéfices supplémentaires en investissant dans des titres financiers, des obligations d’État à taux fixe, des actions, des actions et des obligations immobilières. Cette génération de revenus peut aider à réduire l’écart de richesse et à créer une richesse générationnelle pour échapper à la pauvreté intergénérationnelle en matière de retraite et de vieillesse.

Les Organisations Sœurs Basées en Afrique qui souhaitent savoir comment elles peuvent aligner leurs objectifs de gestion de fonds de pension sur leurs objectifs de réduction de la pauvreté des pensions et celle des personnes âgées peuvent contacter le CENFACS.

Le CENFACS peut travailler avec elles pour explorer des moyens d’aligner les deux objectifs avec leur mission.

Nous pouvons travailler avec elles dans le cadre de notre service international de conseils, d’orientations et d’informations.

Dans le cadre de notre service international de conseil, d’orientation et d’information, nous pouvons les conseiller sur les questions suivantes:

√ Renforcement et développement des capacités

√ Planification et développement de projets

√ Réduction de la pauvreté dans le cadre de la Zone de libre-échange continentale africaine

√ Investissement et développement à but non lucratif

√ Développement de la capacité d’absorption

√ Collecte de fonds et recherche de subventions

√ Génération de revenus et flux de revenus

√ Développement durable

√ Investissement à but non lucratif et investissement à impact

√ Suivi et évaluation

Etc.

Lorsque notre capacité de conseil est limitée, nous pouvons les orienter vers les services et organisations internationaux concernés. Nous pouvons également les orienter vers des organisations travaillant dans la gestion de fonds de pension caritatifs et la pauvreté des pensions/des personnes âgées.

Ce soutien consultatif aux Organisations Sœurs Basées en Afrique est présent tout au long de l’année et fait partie intégrante de notre travail avec elles.

Pour accéder aux services de conseil, d’orientation et d’information; veuillez contacter le CENFACS. Pour vous inscrire ou vous renseigner sur les services de conseil, d’orientation et d’information; vous pouvez vous rendre sur www.cenfacs.org.uk/services-activities.

Main Development

• Autumn Matching Organisation-Investor via Farming Charitable Loan – Match Period 30/10/2024 to 05/11/2024: Matching Organisation-Investor via Loan Disbursement (Stage 4)

As said in the Key Messages, both APRC and N-f-p FI agreed on how APRC will review the borrower’s application, credit history, income, and other loan determining factors. We have started to look at the Farming Charitable Loan Disbursement process, as part of Stage 4.

To explain how both APRC and N-f-p FI are going to proceed and what is going to happen in this Stage 4, we have organised our notes around the following headings:

∝ What Is a Business Loan Disbursement?

∝ What Is APRC’s Plan for Business Loan Disbursement?

∝ Key Areas of the Business Loan Disbursement Process to Be Clarified by APRC

∝ Reaching an Agreement on the Key Areas of the Business Loan Disbursement Process

∝ The Match or Fit Test

∝ Concluding Note on Autumn Matching Organisation-Investor via Farming Charitable Loan

Let us look at each of these headings.

• • What Is a Business Loan Disbursement?

There are many ways of defining business loan disbursement. The definition we are going to use here comes from Faster Capital (10) which argues that

“Loan disbursement refers to the process of releasing funds from a lender to a borrower after the loan has been approved”.

In the context of our matching programme, the loan disbursement in which we are interested is a business one, not a personal or other ones.

Both parties (i.e., APRC and N-f-p FI) may understand what business loan disbursement means. But, they may have different ways of interpreting or applying it. This is why APRC needs to explain to the N-f-p FI its own plan for loan disbursement.

• • What Is APRC’s Plan for Business Loan Disbursement?

According to Faster Capital (11),

“It [loan disbursement plan or process] involves a series of steps that ensure the funds are transferred securely and efficiently from the lender to the borrower, and it is essential for loan servicers to understand these steps to manage them effectively”.

In its business loan disbursement plan, APRC will ensure that borrowers are given details outlining how the loan will be disbursed and disbursement stages. It will also make sure that the funds will be used as intended. As a result, it will monitor and track the loan disbursement progress.

As a matter of fact, APRC has planned the following:

√ to provide borrowers with loan disbursement documentation for disbursement tracking and documentation

√ to record disbursement dates and amounts for transparency and financial planning

√ to explain loan methods (e.g., direct deposit, business bank account, cheque issuance or electronic transfer) and triggers

√ to specify disbursement terms (i.e., full or partial or direct payment loan disbursement) including the time for disbursement

√ to organize communication channels (such as email, automated SMS notifications, letters by post, etc.)

√ to make provision for risk assessment measures (e.g., identity verification systems and fraud detection tools)

etc.

However, business loan disbursal is a process which involves many steps and elements. These steps or elements must be clarified by APRC in order for N-f-p FI can invest in the APRC’s Farming Charitable Loan project.

• • Key Areas of the Business Loan Disbursement Process to Be Clarified by APRC

These are areas of the business loan disbursement process that APRC will need to clarify in order to get a good match with N-f-p FI’s view on loan disbursal.

From these areas, N-f-p FI would like some clarity about the following points or questions:

σ The efficiency and effectiveness of APRC’s loan disbursement

(e.g., APRC needs to explain the extent to which its loan disbursement will be producing satisfactory results with an economy of effort and a minimum waste, while generating a powerful desired outcomes for borrowers)

σ Enhancement of borrowers’ seamless experience

(that is, Will the loan enhance borrowers’ experience that shows no signs of having been pieced together?)

σ Minimized operational costs

(for example, Whether or not APRC will use digital disbursement methods such as electronic fund transfers)

σ Optimization of operational efficiency and loan disbursement processes

(e.g., Organising direct payment to the supplier of farming equipment on behalf of borrowers)

σ Risk mitigation

(e.g., How APRC will reduce the risk of fraud during disbursement)

σ Borrowers’ complaints

(for example, How APRC will resolve disputes and discrepancies over the loan terms)

σ APRC’s competitive advantage

(for instance, What advantage that APRC will have over rivals running similar projects or services)

σ The impact of loan project on APRC’s cash flow

(that is, Will the loan project improve APRC’s cash flow management?)

σ Streamline and automate disbursement processes

(i.e., Will APRC uses loan disbursement processes that will employ automatic machinery in data-processing and be extremely efficient, with little or no waste of resources, excess staff and unnecessary steps to reduce the time for the disbursement?)

σ Loan approval criteria

(e.g., Will the loan amount for APRC’s members get approved depending on their membership status or their credit score or income?

σ Disbursement options

(for instance, Will APRC offer flexible disbursement options like mobile money wallet, direct deposit, electronic funds transfer and physical check?)

σ Monitoring tools and metrics

(in other words, What are the details for disbursement monitoring tools and metrics?)

etc.

Without undermining the other areas of the business loan disbursement process, let us look at disbursement monitoring tools and metrics.

• • • Disbursement performance monitoring tools, metrics and indicators

APRC will provide useful disbursement monitoring tools or calculations to show that the project will be monitored and its performance will be financially tracked. It can explain the financial ratios or metrics or key performance indicators below.

APRC can, for example, use the following key indicators linked to the performance; indicators which we have selected from the top 10 Key Performance Indicators to measure the efficiency of loan origination process provided by ‘cloudbankin.com’ (12):

a) Pull-Through Rate =

Number of Loans Disbursed / Number of Loan Applications Submitted during the Same Period

b) Cost Per Unit Originated =

Total Expenses Incurred / Number of Loans Disbursed during the Same Period

c) Application Approval Rate =

Number of Approved Applications / Number of Valid Applications Submitted in that Same Period

d) Abandoned Loan Rate =

Number of Approved Loans Not Disbursed / Number of Applications Approved in that Same Period

e) Profit Per Loan =

(Total Revenue – Total Expense) / Number of Loans Disbursed in that Same Period

We can as well add the Key Metrics for Loan Performance Analysis given by Faster Capital (13), metrics which are below.

i) Delinquency Rate

It measures the percentage of loans that are past due.

ii) Default Rate

It represents the proportion of loans that have defaulted.

iii) Recover Rate

It explains how much of the outstanding balance is recovered through asset sales or other means.

iv) Repayment Rate

It is when borrowers pay off their loans early.

To the above suite of metrics and indicators, we can also include customer feedback, risk assessment and data security measures, etc.

To get to the next level of the matching game, APRC needs to demonstrate to N-f-p FI that it has the above mentioned tools to track its performance and will take action to make the business loan disbursement process a success story.

• • Reaching an Agreement on the the Key Areas of the Business Loan Disbursement Process

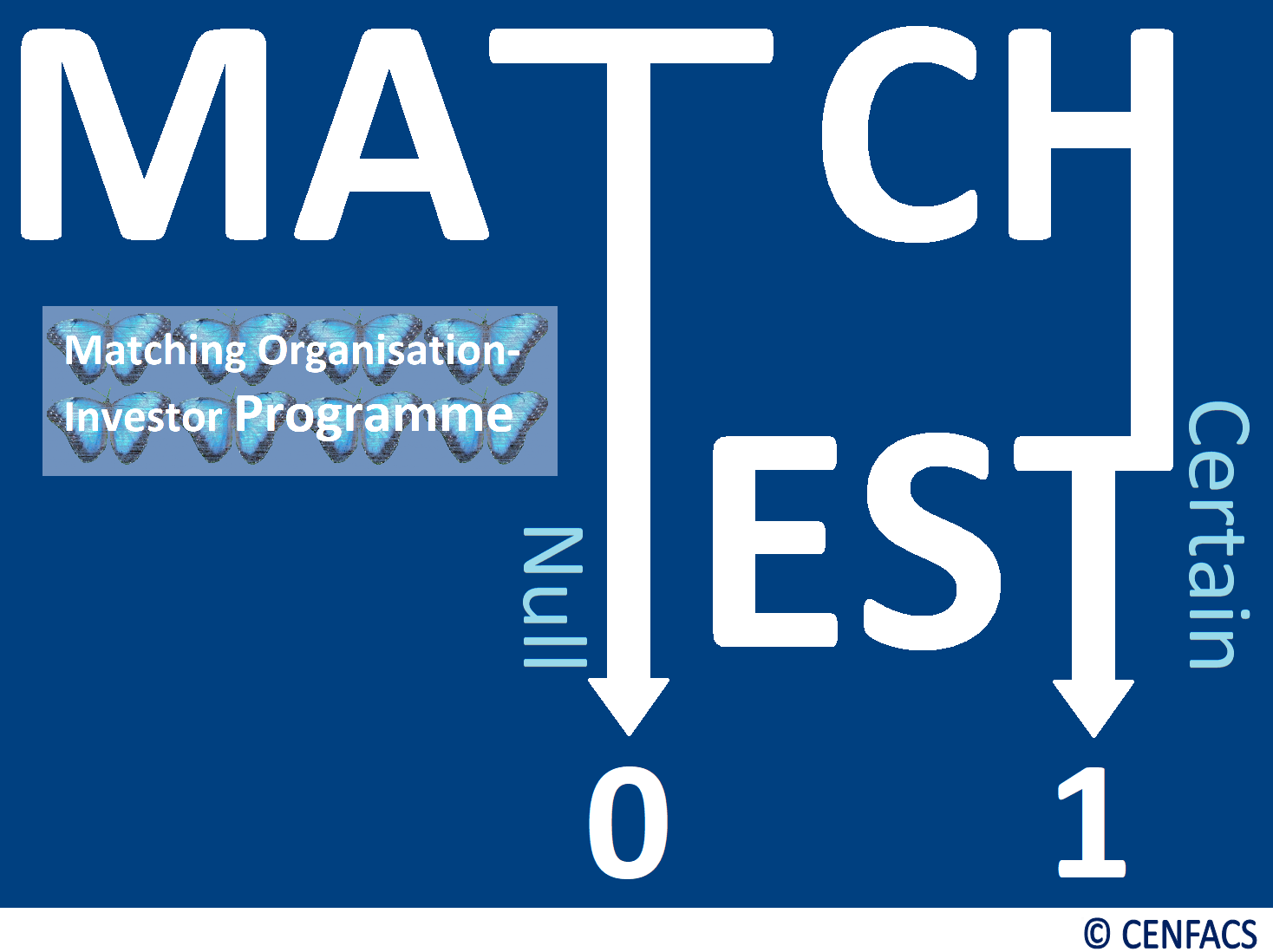

The two sides (APRC and the n-f-p farming investor) need to reach an agreement on the terms and conditions outlined in the loan disbursement process. If there is a disagreement between APRC and n-f-p farming investor, this could open up the possibility for a match/fit test. The match/fit test can be carried out to try to help the two sides. The match/fit test can also be undertaken if there is a disagreement on any of aspects of the farming charitable loan project.

• • The Match or Fit Test

As part of the match or fit test, n-f-p FI’s view on APRCs loan disbursement process must be matched with the information coming out of APRC’s business loan disbursement process.

The match can be perfect or close in order to reach an agreement. If there is a huge or glaring difference between the two (i.e., between what the investor wants and what APRC is saying about its loan disbursement process or loan origination system, between what the investor would like the loan disbursement process to indicate and what APRC’s loan disbursement process is really saying), the probability or chance of having an agreement at this fourth round of negotiations could be null or uncertain.

• • • Impact Advice to APRC and Guidance to n-f-p Farming Investor

CENFACS can impact advise APRC to improve the presentation of their loan disbursement process or loan origination system. CENFACS can as well guide n-f-p farming investors with impact to work out their expectations in terms of loan disbursement process to a format that can be agreeable by potential APRCs. CENFACS’ impact advice for APRCs and guidance on impact investing for n-f-p farming investor, which are impartial, will help each of them (i.e., investee and investor) to make informed decisions and to reduce or avoid the likelihood of any significant losses or misunderstandings or mismatches.

• • • The Rule of the Matching Game

The rule of the game is the more farming investors are attracted by APRCs’ loan disbursement process the better for APRCs. Likewise, the more APRCs can successfully respond to farming investors’ level of enquiries and queries about the loan disbursement process the better for investors. In this respect, the matching game needs to be a win-win one to benefit both players (i.e., investee and investor).

The above is the fourth stage of the Autumn Matching Organisation-Investor via Farming Charitable Loan.

Those potential organisations seeking investment to set up a lending scheme/project and n-f-p farming investors looking for organisations that are interested in their giving, they can contact CENFACS to arrange the match or fit test for them. They can have their fit test carried out by CENFACS’ Hub for Testing Hypotheses.

• • • CENFACS’ Hub for Testing Hypotheses

The Hub can help to use analysis tools to test assumptions and determine how likely something is within a given standard of accuracy. The Hub can assist to

√ clean, merge and prepare micro-data sources for testing, modelling and analysis

√ conduct data management and administration

√ carry out regression analysis, estimate and test hypotheses

√ interpret and analyse patterns or trends in data or results.

For any queries and/or enquiries about this fourth stage of Autumn Matching Organisation-Investor via Farming Charitable Loan and/or the programme itself, please do not hesitate to contact CENFACS.

• • Concluding Note on Autumn Matching Organisation-Investor via Farming Charitable Loan

African charities like other for-profit organisations can set up a lending scheme/project or loan origination system (LOS) to enable them to back up their charitable mission and vision, provided this scheme or project is within the regulatory frameworks of the countries in which they operate and within their constitutional rules. In other words, they can do it within the powers they have been given by their legislators and their governing rules (e.g., articles of association). However, they need to make sure that the newly formed lending scheme/project or LOS can generate enough income so that the more the difference between the sales revenue and the costs of those sales is, the better they can find the financial resources they need to allocate to their worthy causes. They are also required to guarantee that the loan that will be made from the LOS will generate both financial benefit and charitable benefit for them while charitable benefit superseding financial benefit.

There are not-for-profit impact investors who can help them to either to start or develop their idea of having a money lending scheme or project to reduce poverty. Where African charities, we mean CENFACS‘ Africa-based Sister Charitable Organisations (ASCOs) or African Poverty Relief Organisations (APRCs) like in this matching exercise, experience some difficulties in finding these types of investors, CENFACS can work with ASCOs/APRCs to source them.

Equally, for n-f-p impact investors who are looking for Africa-based organisations to invest in but they are not sure which organisation that can be their investee, CENFACS can as well work with these investors so that their investment is channelled to the right organisation, at the right moment and to the right cause. CENFACS can match ASCOs’/APRCs’ need to find an investor and n-f-p impact investor’s desire to get an investee.

The match probability can be high or average or low depending on how much ASCOs’/APRCs’ needs meet investors’ interests. CENFACS will make sure that this match is the strongest possible one.

CENFACS is available to work with ASCOs/APRCs that are looking for Impact Advice and Not-for-profit Investors who need Guidance with Impact so that the former can find the investment they are looking for and the latter the organisation to invest in, and both of them can realise their respective Autumn dreams.

To work together to make your matching dream come true by finding your ideal investee or investor, please contact CENFACS.

_________

• References

(1) https://financefuturists.com/loan-disbursement-meaning/ (accessed in October 2024)

(2) https://www.lawinsider.com/dictionary/pension-fund-manager# (accessed in October 2024)

(3) https://www.glassdor.co.uk/Salaries/pension-fund-manager-salary-SRCH_KO0,20.html (accessed in October 2024)

(4) https://www.unicef.org/esa/press-releases/unicef-alarmed-continued-attacks-education-conflict-zones-africa (accessed in October 2024)

(5) https://ptes.org/grants/worldwide-projects/restoring-the-critically-endangered-haplochromis-granti-fish-in-lake-victoria/# (accessed in October 2024)

(6) Park, C., (2011), Oxford Dictionary of Environment and Conservation, Oxford University Press, Oxford & New York

(7) https://msc.org/what-we-are-doing/our-approach/what-is-sustainable-fishing (accessed in October 2024)

(8) https://www.cbd.int/conferences/2024 (accessed in October 2024)

(9) https://www.globalmanprize.org/blog/cop16-what-to-know-about-the-2024-un-biodiversity-conference/ (accessed in October 2024)

(10) https://fastercapital.com/content/Loan-Disbursement-Optimizing-Loan-Disbursement-Strategies-for-Success.html (accessed in October 2024)

(11) https://fastercapital.com/content/Loan-Disbursement–The-Loan-Disbursement-Process-What-Servicers-Need-to-Know.html

(12) https://cloudbankin.com/blog/loan-origination/top-10-kpis-to-measure-the-efficiency-of-loan-origination-process/ (accessed in October 2024)

(13) https://fastercapital.com/content/Loan-Performance-Analysis-How-to-Perform-and-Interpret-Loan-Performance-Data-and-Metrics.html (accessed in October 2024)

_________

• Help CENFACS Keep the Poverty Relief Work Going This Year

We do our work on a very small budget and on a voluntary basis. Making a donation will show us you value our work and support CENFACS’ work, which is currently offered as a free service.

One could also consider a recurring donation to CENFACS in the future.

Additionally, we would like to inform you that planned gifting is always an option for giving at CENFACS. Likewise, CENFACS accepts matching gifts from companies running a gift-matching programme.

Donate to support CENFACS!

FOR ONLY £1, YOU CAN SUPPORT CENFACS AND CENFACS’ NOBLE AND BEAUTIFUL CAUSES OF POVERTY REDUCTION.

JUST GO TO: Support Causes – (cenfacs.org.uk)

Thank you for visiting CENFACS website and reading this post.

Thank you as well to those who made or make comments about our weekly posts.

We look forward to receiving your regular visits and continuing support throughout 2024 and beyond.

With many thanks.